gsheldon

The Hershey Firm (NYSE:HSY), along with its subsidiaries, engages within the manufacture and sale of confectionery merchandise and pantry objects in the USA and internationally.

We’ve began protection on the agency in mid-2022, with a purchase ranking, and we have maintained our bullish view up until now. As our final writing in regards to the firm has been a few 12 months in the past, we determined to revisit the agency to evaluate whether or not our beforehand established arguments for a purchase ranking are nonetheless legitimate.

Our main causes for the purchase ranking have been:

1.) Robust monetary efficiency in 2022, comparatively unaffected by poor client sentiment.

2.) Engaging valuation and dividends.

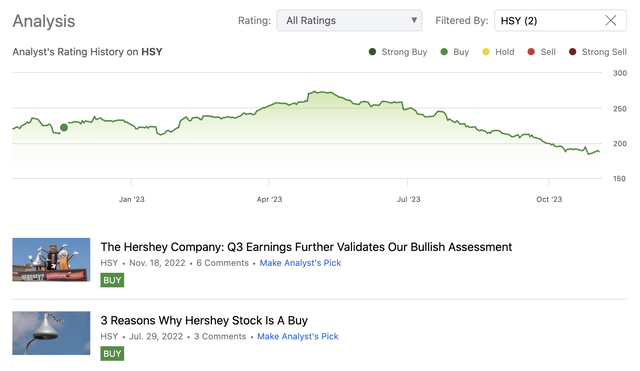

Evaluation historical past (Creator)

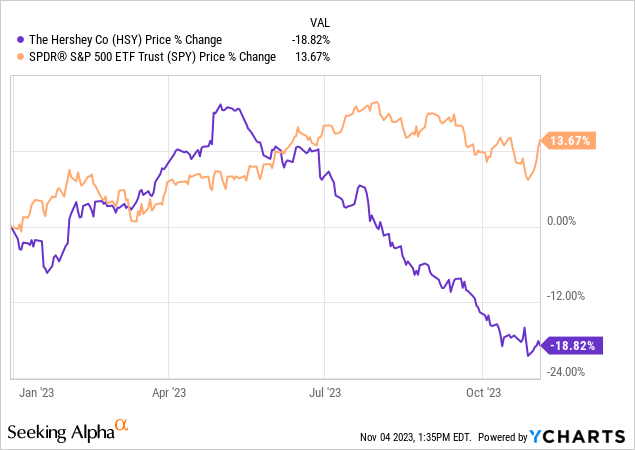

Additionally, because the agency’s market worth has declined considerably 12 months up to now, we’re going to focus on whether or not this might be a pretty alternative to purchase the dip.

To start out off our dialogue, we’ll first take a look at HSY’s newest earnings report.

Earnings

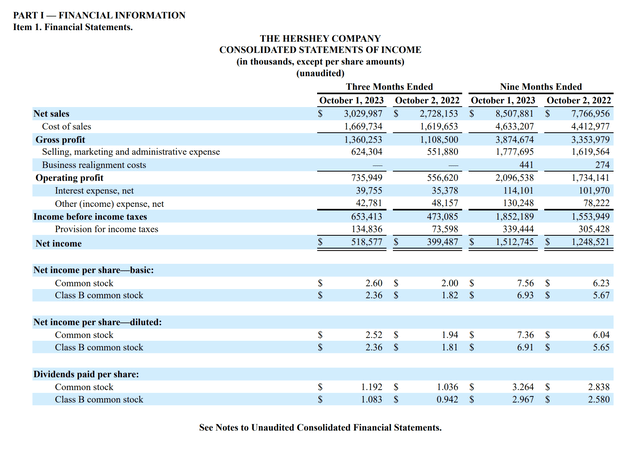

Within the third quarter of 2023, HSY has reported web gross sales of greater than $3 billion, representing a greater than 11% enhance in comparison with the identical interval within the prior 12 months. Natural gross sales development on a relentless foreign money foundation got here in at 10.7%. Reported web revenue has elevated by nearly 30% year-over-year, reaching as a lot as $518.6 million.

Income

Revenue assertion (HSY)

The rise in gross sales has been pushed primarily by worth will increase, nevertheless quantity has additionally contributed.

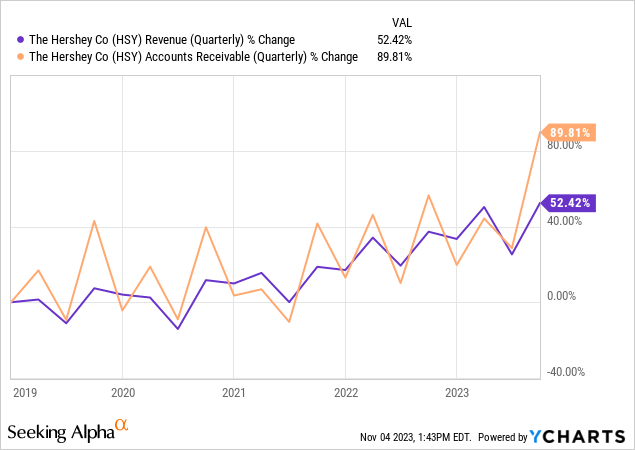

The next chart exhibits how HSY’s income development has developed over the previous 5 years. We will see that regardless of the pandemic and the difficult macroeconomic and geopolitical atmosphere, the corporate has managed to maintain the demand excessive for its merchandise and constantly enhance its gross sales.

We wish to spotlight right here that though accounts receivable have been traditionally fluctuating across the income determine, within the earlier quarter accounts receivable have grown at a a lot quicker than income. We expect it may be a sign that HSY is doubtlessly inflating its gross sales figures by pulling demand ahead from future durations. It’s positively essential to control this growth within the coming quarters. Ideally, we wish to see income development catching up with accounts receivable development.

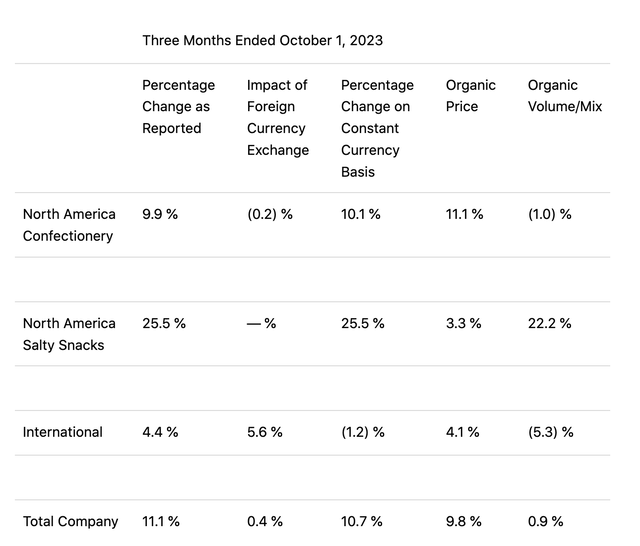

Moreover, we have to spotlight that gross sales haven’t solely elevated in North America, but additionally internationally. Specific consideration must be paid to the salty snacks phase, which has had by far the quickest development.

Gross sales by phase (HSY)

Wanting ahead, we consider that the strong income development is essential indication that HSY’s buyer base exhibits a excessive diploma of loyalty that allows the agency to efficiently broaden. This can be an essential aggressive benefit.

Profitability

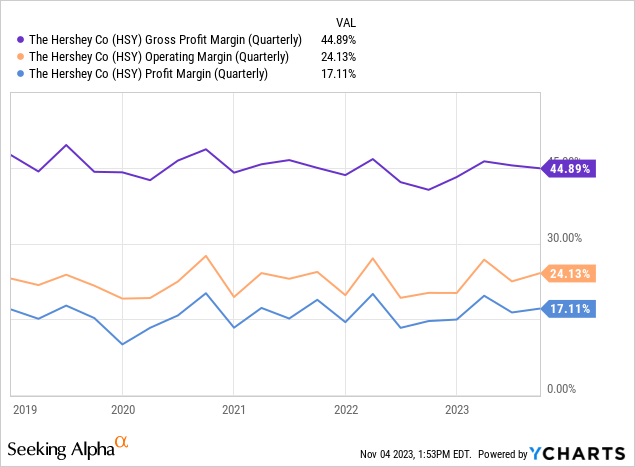

Not solely the income development has been spectacular, but additionally the event of the profitability measures year-over-year. The reported development margin has reached nearly 45%, representing a 4.3% growth in comparison with the prior 12 months. Value realization and productiveness have been the principle causes for the margin growth, nevertheless their constructive impacts have been dampened by the elevated commodity, overhead and manufacturing associated bills.

The next chart exhibits HSY’s revenue margins over the previous 5 years. Simply as income development has been strong, the profitability of the agency has remained pretty secure, contemplating the headwinds created by the comparatively poor client sentiment over the previous years.

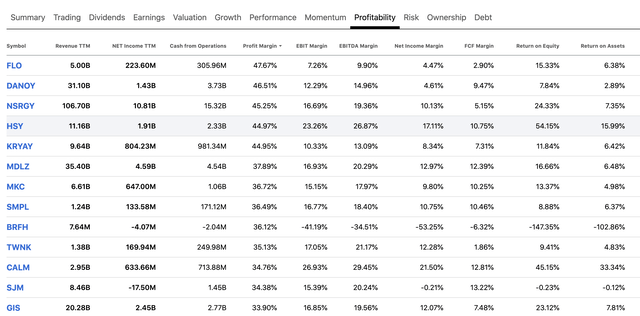

To place these figures into perspective, the next desk compares a set of profitability metrics throughout companies within the Packaged Meals and Meats business. We will clearly see that throughout most metrics, HSY ranks very excessive on the checklist.

Comparability (In search of Alpha)

This excellent profitability mixed with stability makes HSY a pretty enterprise, in our opinion.

Outlook

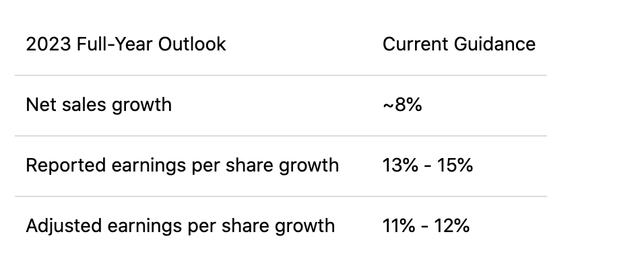

The agency has reiterated its full 12 months outlook for 2023, anticipating excessive single-digit income development and EPS development within the mid teenagers.

Steerage (HSY)

All in all, we consider that HSY has as soon as once more delivered sturdy quarterly outcomes, which show the robustness of the enterprise and the persevering with excellent demand for the agency’s merchandise. Wanting ahead, regardless of the difficult macroeconomic atmosphere, we don’t see vital headwinds for the corporate within the close to time period.

Return to shareholders

Hershey additionally stays enticing for dividend and dividend development traders. The agency has remained dedicated to paying quarterly dividends, which is presently $1.19 per share, equal to an annual yield of roughly 2.5%.

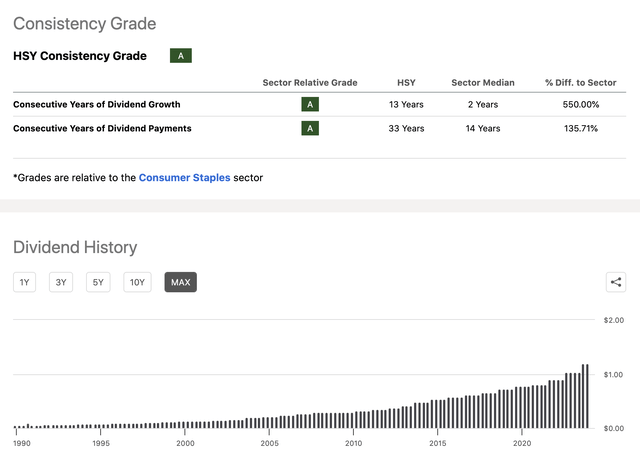

Dividend historical past (In search of Alpha)

Notice that the agency has been paying dividends in annually of the previous 33 years, and so they have managed to extend the funds in every of the previous 13 years.

The dividends additionally seem like protected and sustainable because the money movement from operations within the earlier quarter got here in at $516 million, CAPEX was $218 million, so the agency has greater than sufficient to left to spend on dividends, which finally accounted for $238 million.

HSY has additionally spend $1.1 million to repurchase shares, nevertheless this quantity was comparatively negligible in comparison with the quantity of buybacks within the prior quarters.

Valuation

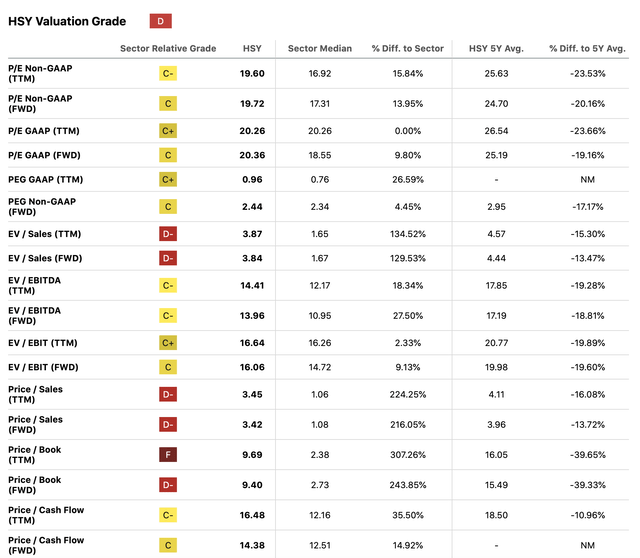

To evaluate, whether or not it’s value investing in HSY’s inventory now, we now have to debate its valuation. To take action, we shall be utilizing a set of conventional multiples to see how the agency’s relative worth is in comparison with its sector, business and its personal 5YR historic averages.

The next desk exhibits the comparability between HSY’s present metrics, the patron discretionary sector median and the agency’s personal historic averages.

Multiples (In search of Alpha)

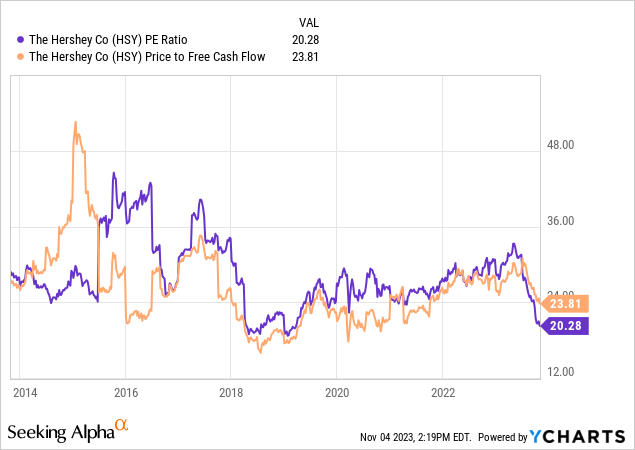

Whereas HSY seems to be buying and selling at a premium in comparison with the sector median, it’s buying and selling at a big low cost in comparison with its personal historic valuation, throughout all metrics. Usually, HSY has been additionally buying and selling at a premium in comparison with the sector median. And if we have a look again on the historic valuation of the agency, we will clearly see that the present drop in share worth could present an ideal alternative to accumulate HSY’s shares at a comparatively enticing worth degree.

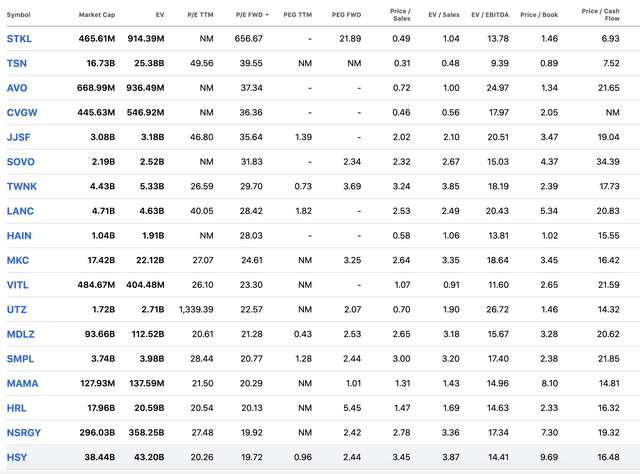

Once we slim the peer group to companies within the Packaged Meals and Meats business, we will see that HSY’s inventory isn’t priced at a premium in any respect, in line with most metrics.

Comparability (In search of Alpha)

To sum up

HSY has delivered sturdy quarterly outcomes with vital enhance in gross sales and EPS. On the similar time the agency has managed to enhance its profitability in comparison with the prior quarter.

The agency has remained dedicated to returning worth to its shareholders within the type of dividend funds. These dividends seem like protected and sustainable, as they’re well-covered by the free money movement.

Whereas the inventory nonetheless trades at a premium in comparison with the patron discretionary sector median, we consider that in comparison with its business friends and its personal 5YR averages, it’s truly attractively priced.

For these causes, we reiterate our earlier bullish ranking.

{kind=link}