Previous efficiency will not be a assure of future outcomes.

In fact it isn’t. Issues change. Particularly if we’re referring to the previous efficiency of a selected funding technique, portfolio supervisor, mutual fund or particular person inventory.

However previous efficiency of asset courses ought to be effectively understood. Particularly the form of previous efficiency that’s taken place over longer stretches of time.

Shares have been one of the best asset class when it comes to outperforming inflation over the past century. We all know this for sure. Over the past seventy years, shares are undefeated versus inflation, however solely over the longest time horizons. Shares have outperformed inflation 100% of the time over all twenty 12 months intervals.

(observe me on Mastodon right here, we’re constructing a brand new neighborhood free from the goblins and orcs who’ve polluted twitter to the purpose of dis-utility)

Can this previous efficiency fail to indicate up in any future twenty 12 months interval? In fact it could actually. By no means say by no means. Will shares at all times be one of the best asset class versus inflation? Possibly not. Possibly bonds find yourself working higher over the following 20 years. Possibly money. Possibly commodities or actual property or gold or CrackCoin or no matter else. We all know something is feasible, which is why investing includes danger.

However when one thing has persistently labored over seven many years, with out fail, no matter all different situations and variables, maybe it’s greatest to take that danger relatively than not. Even with the total acceptance of the Previous Efficiency caveat. You possibly can learn extra about inflation and discover the chart above right here at Goldman Sachs Asset Administration with all associated disclaimers.

How do shares beat inflation? Permit me to oversimplify the story for the good thing about individuals who aren’t searching for a grad school-level dissertation the morning after Thanksgiving…

The inventory market is valued on earnings (income) and these earnings are reported in nominal phrases. If Colgate sells you toothpaste for $2 in 2019 after which sells you that very same tube of toothpaste three years later in 2022 for $4, the nominal income progress they’re reporting to shareholders is 100%. Has Colgate’s value to make, ship, market and promote that toothpaste gone larger? Sure. Is that value larger by 100% thereby utterly offsetting the income progress achieve? Most likely not. So income progress results in earnings progress, even web of upper working prices in an inflationary setting. That is how inflation truly helps corporations develop their earnings up till a sure level the place prices rise an excessive amount of or demand destruction happens.

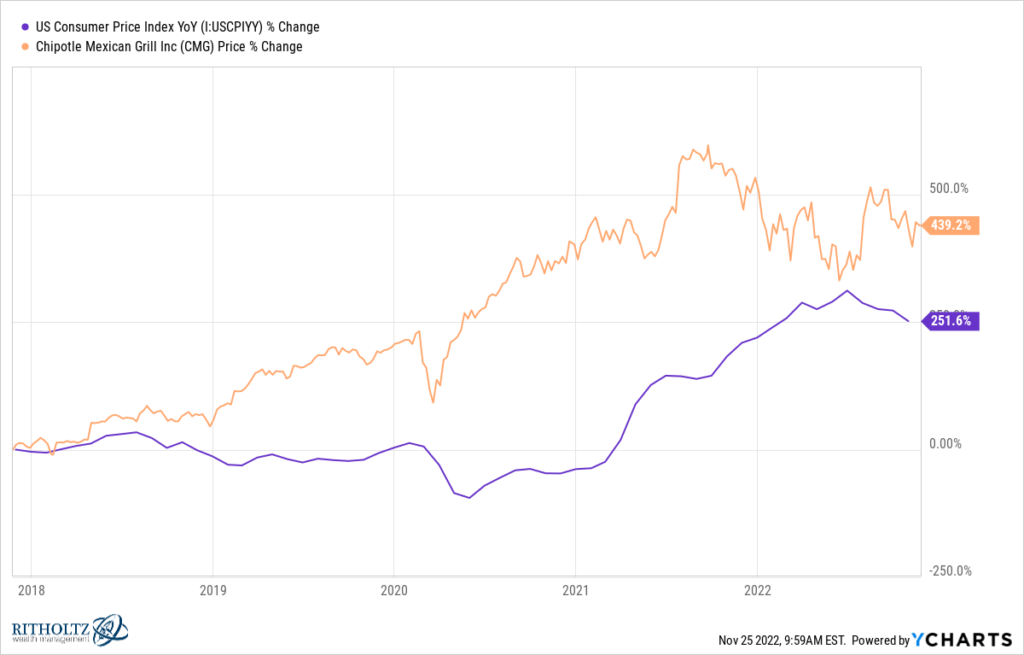

At Chipotle, the price of a barbacoa burrito was $7.50 in 2017 and as of the top of 2021 it was $9.10. That’s a value improve of 21.33%. If Chipotle’s value of constructing and promoting that burrito solely rose by 15% throughout that very same time frame (I’m making this up, however bear with me), then Chipotle’s shareholders have benefited by elevated earnings in each nominal and actual phrases. Chipotle’s web earnings was $176 million in 2017. It was $652 million final 12 months. Inflation has risen however Chipotle’s means to extend costs, open extra shops, promote extra burritos, and many others has far outpaced it. A bar of gold may maybe preserve tempo with inflation, however a burrito, correctly ready and marketed, can blow its doorways off. Even when the burrito prices extra to make every year.

I’m conceding that the beneath might represent one in all historical past’s biggest chart crimes however I’m posting it anyway – Chipotle’s inventory value return versus year-over-year CPI inflation, over 5 years, blame YCharts for permitting me to create this atrocity:

Within the present setting, corporations are complaining about rising prices (particularly labor) on each convention name, however they’re nonetheless getting by. These prices are being handed alongside to customers with out a lot demand destruction (thus far). For this reason predictions of an earnings per share collapse for the S&P 500 have been flawed. S&P 500 corporations are probably the most well-equipped corporations on the earth when it comes to weathering larger prices. They eat larger prices for breakfast. Larger prices drive will increase in innovation, which we’re actually f***ing good at in case you didn’t know.

In some unspecified time in the future, persistently excessive inflation will hit demand tougher than it already has. In some unspecified time in the future, income progress and earnings progress will likely be a lot tougher to return by as customers push again or retrench. Tightening monetary situations will contribute to this pulling again. It’s a certainty – the one query is when and the way excessive rates of interest need to go for this to occur. The inventory market is aware of this, therefore the document volatility seen through the first 9 months of this 12 months.

However all people is aware of this. The inventory market has shed trillions in market capitalization already. It’s not information.

In the meantime, there are inventory charts pointing larger in all places you look in at present’s market. My pal JC at All Star Charts is saying “Enjoyable Truth: The Dow Jones Industrial Common, after rallying over 5000 factors since final month is already up 19.3% from its lows.”

Right here’s his have a look at the S&P 500 and the proportion of S&P 500 shares which can be 20% up (or extra) from this 12 months’s lows.

The listing is large and rising. In case you can tear your eyes away from the profitless tech spectacle, you may see it in all places. A scorching CPI print in December may actually negate this progress, however what if it doesn’t?

So sure, inflation is a cause to be cautious of inventory market volatility within the close to time period. However it’s completely not a cause to not make investments, as long as the highway forward is lengthy and your timeframe is measured in many years relatively than weeks or months. In reality, inflation is all of the extra cause to proceed to take the suitable dangers, tuning out as a lot of the each day bullsh*t as you probably can.

Learn additionally:

IS 3% THE NEW 2%? SIZING UP A SCENARIO OF HIGHER INFLATION TARGETS (GSAM)

Shares in Bull Markets (All Star Charts)

Downtown Josh Brown (Mastodon)

{kind=link}