Kelly Sullivan

Contemplating Meta Platforms (NASDAQ:META) as soon as traded close to $400, the inventory rallying to $240 following higher than anticipated quarterly outcomes is only a continuation of the overdue rebound. The social media inventory ought to’ve by no means traded under $100 on the irrational concern of overspending on the Metaverse. My funding thesis stays Bullish on the inventory as the corporate nonetheless is not maximizing earnings whereas investing for the long run.

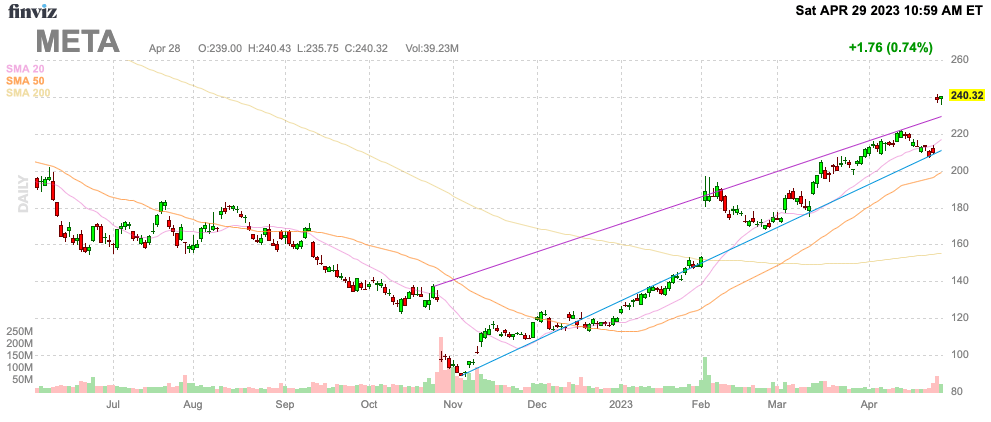

Supply: Finviz

Fixing Income Drawback

The entire focus during the last 12 months was the extreme spending from Actuality Labs and wild progress within the workforce. In actuality, the answer to the issue all alongside was the income facet of the equation.

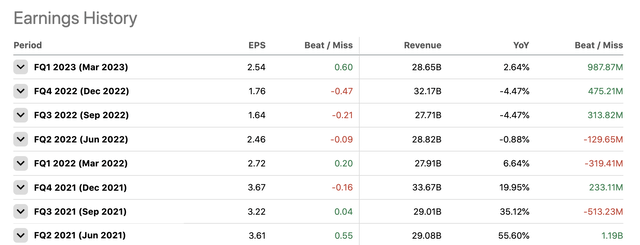

For Q1’23, Meta reported revenues of $289.7 billion, beating analyst estimates by a large $990 million. The Q2’23 steering was way more spectacular with a goal of $29.5 to $32.0 billion versus the $29.5 billion consensus estimates.

The social media large had reported a string of earnings experiences going again to Q2’21 the place Meta did not beat income estimates by this a lot. In reality, through the interval of 8 quarter, the tech large missed income estimates 3 instances.

Supply: Searching for Alpha

Whereas taking part in the expectations recreation could be deceptive, the large key to Q1 precise numbers was a return to progress after 3 quarters of YoY income declines. The typical analyst estimate for Q2 is for revenues to leap 6% YoY to $30.6 billion and a quarterly determine above $30 billion could be a report non-holiday quarter.

Meta can clear up plenty of the overspending points from the final 12 months by returning to gross sales progress. Contemplating the financial system hasn’t improved, the numbers recommend the social media large has solved a number of the IDFA points brought on by the privateness modifications at Apple (AAPL) and Reels is gaining momentum.

The corporate will clear up plenty of the illnesses by returning to double-digit progress making the spending challenge simpler to resolve. CEO Zuckerberg can acquire effectivity by sustaining prices as a lot as chopping prices.

A major instance of how the market received off heart on the Metaverse is that Meta is seeing substantial positive aspects from utilizing AI to spice up time on Instagram through Reels. On the Q1’23 earnings name, CEO Mark Zuckerberg reported the next spectacular metrics:

Since we launched Reels, AI suggestions have pushed a greater than 24% enhance in time spent on Instagram. Our AI work can also be enhancing monetization. Reels monetization effectivity is up over 30% on Instagram and over 40% on Fb quarter-over-quarter. Each day income from Benefit+ procuring campaigns is up 7x within the final six months.

These numbers assist Meta fixing the problems from IDFA to the market share shift to TikTok in prior quarters. On high of this, the corporate continues to cut back the workforce to supply a double enhance to the underside line whereas nonetheless investing aggressively sooner or later.

Actuality Labs Will Pay Off

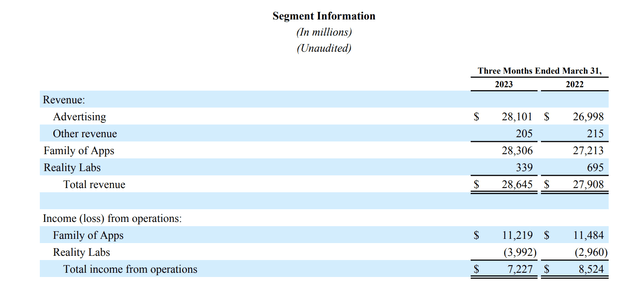

The superb half is that Meta made all of this progress to enhance earnings whereas nonetheless investing an insane quantity in Actuality Labs. The corporate spent over $4 billion on the phase throughout Q1’23 resulting in an annualized loss fee at a large $16 million.

Supply: Meta Platforms Q1’23 earnings launch

Contemplating the Metaverse has been sluggish to ramp, Meta has a protracted runway to cut back the losses on this space and enhance earnings going ahead. In reality, Actuality Labs revenues had been down practically 50% within the quarter due partially to weak point from the headsets.

The Meta Quest Professional launched final 12 months hasn’t had a formidable uptake whereas the Quest 2 has failed to keep up momentum because the machine ages. With the corporate fixing the advert income issues, Zuckerberg may have the money flows to proceed investing within the promise of the Metaverse together with AR/VR units.

Based on Verge, the corporate has the next schedule outlined for future AR/VR headsets:

- 2023: Quest 3 – 2x thinner, twice as highly effective

- 2023: Good glasses – 2nd era machine

- 2024: Quest 4 – photorealistic, codec avatars

- 2025: Good glasses – third era with a show and a neural interface

- 2027: AR glasses

An excessive amount of alternative exists on this space for Meta to reign in many of the funding on this class. Analysts have the corporate producing the next EPS targets over the following 3 years with the 2025 goal approaching $15 per share.

Traders can determine find out how to worth the enterprise primarily based on the extreme spending on the Metaverse. Meta is shedding $16 billion yearly, amounting to about ~$13 billion after taxes.

The corporate now has 2.6 billion shares excellent resulting in a few $5 EPS hit from the aggressive spending on Actuality Labs. At a 20x EPS goal, the evaluating is giving up a few $100 per share price of market cap from investing within the Metaverse.

Traders need to know Meta both turns this right into a future worthwhile progress driver or Zuckerberg will implement one other 12 months of effectivity for the Metaverse.

Takeaway

The important thing investor takeaway is that Meta is just too low cost buying and selling under 20x official 2024 EPS targets. In actuality although, buyers ought to slap a $20+ EPS goal on the 2025 earnings and examine the inventory buying and selling at 12x a extra normalized EPS goal as soon as the enterprise is absolutely again in progress mode (together with effectivity enhancements) and including again the non permanent Metaverse losses.

After this large rally, buyers ought to most likely anticipate a near-term pause, however finally the inventory nonetheless has legs.

{kind=link}