wildpixel

Introduction

On April 20, I wrote an article titled XLE: Be Protected The Subsequent Oil Bull Market Will Be Wild. In that article, I made the case to purchase power shares to be protected against what might turn into a raging bull market in power commodities.

This is part of my takeaway:

Investing within the power sector has turn into tougher on account of latest structural adjustments, which I view as a long-term optimistic for the business. There’s a excessive likelihood that oil costs could surge into the triple-digit territory as soon as demand hits its backside, due to the OPEC cuts and their expectations of stronger-than-anticipated long-term demand.

[…] Due to this fact, I strongly suggest holding power shares for each their potential capital beneficial properties and dividends, and I imagine that having some publicity to the power sector is essential within the present power and inflation surroundings, which was not vital earlier than the pandemic.

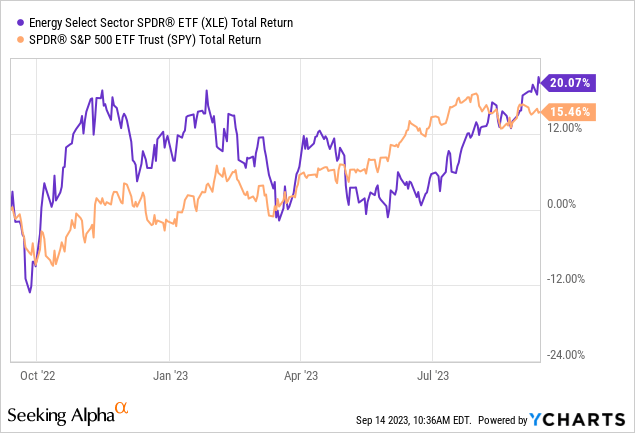

Since then, the Power ETF (NYSEARCA:XLE) has rallied roughly 11%, beating the S&P 500 by 300 foundation factors.

Now, it is time for an replace. Not solely have I written numerous articles on varied power shares, updating my bull case, however we have additionally seen a affirmation of my thesis.

After breaking out in July, crude oil futures are again at $90. That is regardless of poor client confidence and a normal downtrend in financial progress.

TradingView (NYMEX Crude Oil)

On this article, I am going to talk about the drivers of this bull case and clarify why I proceed to imagine that proudly owning power shares is so vital.

So, let’s get to it!

Provide – The Driver Of Greater Costs

Like each different commodity, oil is all about provide and demand.

The provision image is what worries me (that means, it might trigger excessive inflation for a few years to come back) as a result of main basins within the U.S. are operating out of steam.

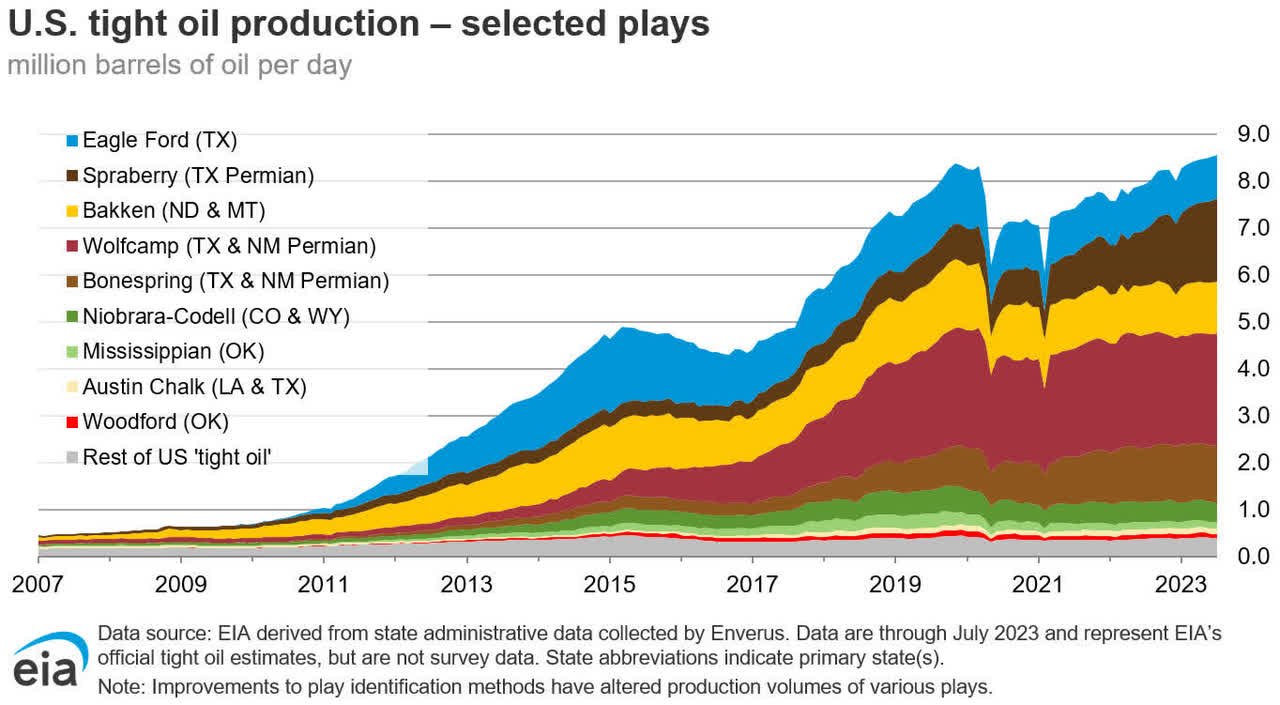

After the Nice Monetary Disaster, U.S. shale manufacturing was the rationale why world oil costs have been subdued more often than not (particularly after 2014). In 2007, the U.S. produced roughly 500 thousand barrels of oil per day utilizing unconventional measures (horizontal drilling). Now, that quantity is 8 million barrels per day greater!

Power Data Administration

This aggravated OPEC quite a bit. It even aggravated U.S. producers, as they have been producing a lot that each decline in demand brought on oil costs to crash.

So many smaller gamers went bust up to now few years.

Now, issues are altering. U.S. shale is operating out of stream. We’re not seeing peak oil however a big decline in provide progress. Producers are seeing quickly declining Tier 1 drilling reserves. They deal with free money circulation technology as a substitute of manufacturing progress and reward traders by dividends and buybacks.

They’ve discovered their lesson – particularly in an surroundings the place new local weather actions wish to put huge oil out of enterprise.

Because the chart above reveals, shale manufacturing is barely greater than it was previous to the pandemic. The one basin with progress left is the Permian (the large one).

Even that basin is predicted to succeed in peak manufacturing in 4Q24.

OPEC Is Again

With the U.S. shedding pricing energy, OPEC is witnessing an opportunity to turn into extra highly effective.

One of many explanation why oil is again at $90 is aggressive output cuts from OPEC (primarily Saudi Arabia). Saudi Arabia needs to guard $80 Brent in any respect prices. It additionally appears to be prepared to defend $90 Brent, on condition that they introduced an extension of the cuts.

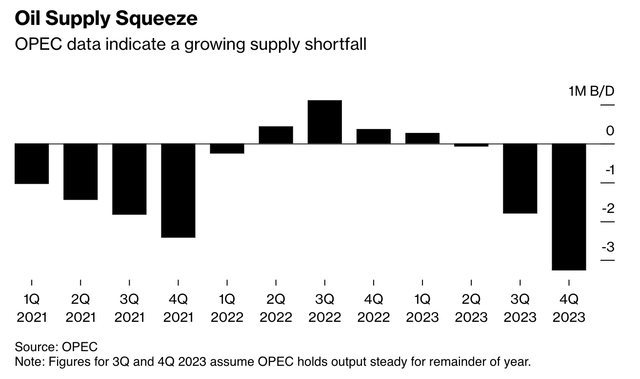

International oil markets face a deficit of 1.2 million barrels a day through the second half of 2023 following final week’s bulletins by the OPEC+ leaders that they will lengthen cutbacks to the tip of the yr, the company mentioned. It is smaller than projected final month, because of historic adjustments to demand estimates, however nonetheless poses dangers for customers. – Bloomberg

Due to the availability squeeze, we’re coping with an growing provide shortfall, pushing up costs.

Bloomberg

We will assume that OPEC is probably going enjoying a political recreation right here. Whereas I am clearly not a political insider who is aware of what, for instance, the Saudis are as much as, I can think about what they’re doing right here.

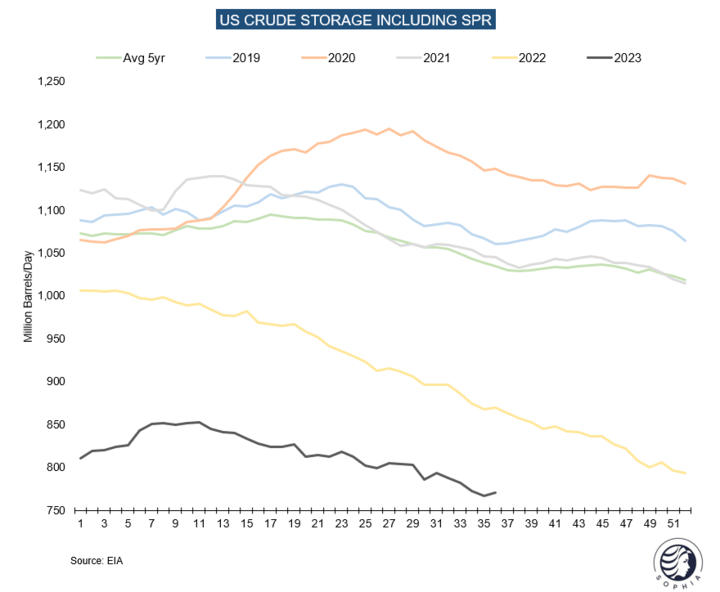

Wanting on the chart under, we see that crude oil storage ranges within the U.S. are method under something we have seen over the previous 5 years (and earlier than that).

Together with the strategic reserves, reserves are greater than 200 million barrels under their longer-term common. Additionally, we’re going into a significant election yr. I doubt Biden – or any Democrat – needs to purchase again oil on this surroundings.

Twitter/X (@SophiaKnowledge)

Having mentioned that, demand developments are additionally favorable.

No, Demand Is not Peaking

As reported by Bloomberg on September 14, forecasts from main power analysts counsel that world crude oil consumption is on an unstoppable ascent.

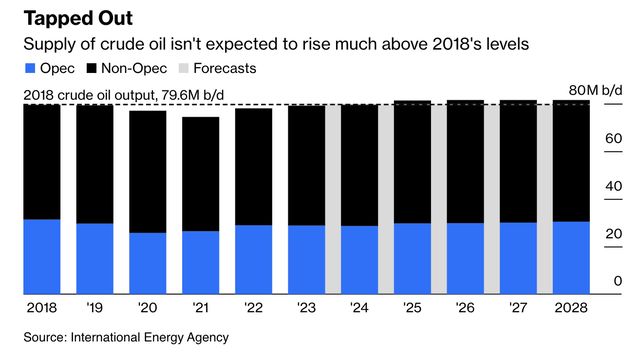

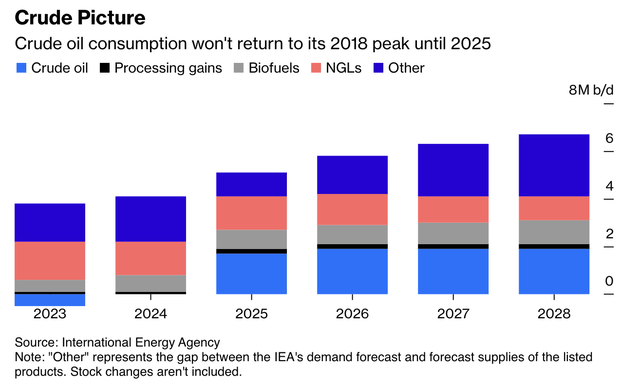

The Worldwide Power Company (“IEA”) tasks a record-breaking 102.2 million barrels per day for this yr, with a relentless climb to 105.7 mb/d by 2028.

Bloomberg

Exxon Mobil (XOM) additionally anticipates demand to surge by roughly 7.5 mb/d till it peaks in 2040.

What’s fascinating is that the IEA (don’t confuse this with the EIA) is not *that* bullish. Its outlook consists of barely any demand progress by 2028.

They don’t count on 2018 ranges to be reached earlier than 2025, as most consumption is predicted to come back from pure gasoline liquids and biofuels.

Bloomberg

In accordance with Bloomberg’s David Fickling, we may very well be taking a look at a peak demand situation for crude oil – regardless of the general optimistic demand image of fossil fuels.

Put all that collectively, and the trail for crude oil to rise above earlier peak ranges could also be far narrower than you’d assume from listening to bullish studies of refinery output. Final September, I predicted a world recession pushed by fast-rising rates of interest would forestall crude oil demand ever rising above its pre-pandemic document. The recession hasn’t materialized, however crude demand remains to be ready to get well. Ought to biofuels and NGLs proceed to outperform, we could come to look again on 2018 because the yr that 150 years of crude oil demand lastly peaked.

Having mentioned that, I agree with the outlook that fossil gasoline demand is not peaking. I don’t imagine that we’re anyplace near a peak, as we’re at the beginning of large progress within the middle-class inhabitants of India and varied African nations.

Whereas India will be sure that to construct a future with much less dependency on overseas power (studying from China’s errors), I don’t see a situation the place oil demand turns right into a headwind – ignoring cyclical recessions that occur often. I am speaking concerning the greater image.

OPEC additionally issued an announcement on September 14, reacting to the IEA’s outlook and feedback.

OPEC

Permit me to share a number of quotes from OPEC’s letter. I’ll add emphasis and my very own view on issues.

It’s a particularly dangerous and impractical narrative to dismiss fossil fuels, or to counsel that they’re at the start of their finish. In previous many years, there have been typically calls of peak provide, and in more moderen ones, peak demand, however evidently neither has materialized. The distinction at present, and what makes such predictions so harmful, is that they’re typically accompanied by calls to cease investing in new oil and gasoline tasks.

OPEC is 100% proper right here. Whereas suggesting that we might peak demand could very effectively be a incorrect thesis, actively pushing for fewer investments in oil and gasoline is a critical concern. We’re at present discovering out what occurs when rising demand meets slower provide progress. The center class (and everybody under) will get squeezed.

In recent times, we have now seen power points climb again to the highest of the agenda for populations as many glimpse how experimental internet zero insurance policies and targets impression their lives. They’ve official issues. How a lot will they price of their present type? What advantages will they carry? Will they work as hyped? Are there different choices to assist cut back emissions? And what’s going to occur if these forecasts, insurance policies and targets don’t materialize?

I typically make the case that I’m not rooting for top power inflation. Though I’ve shut to twenty% power publicity, my essential concern is the safety of my portfolio, as elevated inflation is mostly dangerous for the inventory market.

That is additionally why I am writing this text.

Wall Road Journal

Lastly, I agree with OPEC in relation to options.

[…] OPEC doesn’t dismiss any power sources or applied sciences, and believes that each one stakeholders ought to do the identical and acknowledge short- and long-term power realities,” says HE Al Ghais.

I have been a lot of instances on Dubai-based Asharq TV, the place I mentioned power insurance policies. My level has all the time been to make use of the proceeds from fossil fuels to construct options. We must always NOT lower dependable sources earlier than we have now good options.

That is the most important mistake we’re at present making.

My View & XLE

Placing all issues collectively, I am bullish on oil. Whereas I don’t rule out potential recession dangers that would push oil down $20 to $70, I am a purchaser on main weak point, defending my portfolio in opposition to what I imagine will likely be a long-term uptrend in crude oil. I imagine that triple-digit greenback costs are possible, which might include a second wave of inflation – particularly if the Fed is compelled to chop charges sooner or later.

Whereas I don’t personal XLE, I imagine that XLE is a good way to hedge in opposition to power inflation with out having to tackle elevated dangers.

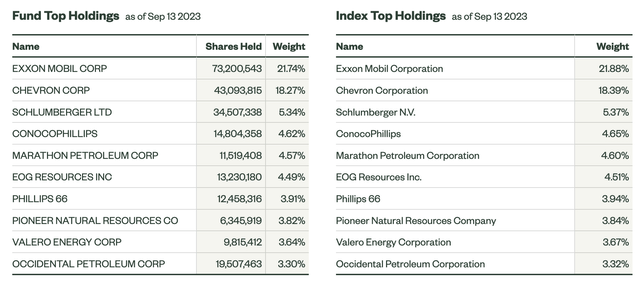

Incepted in 1998, XLE is without doubt one of the oldest ETFs available on the market. It has a 0.10% expense ratio and a quarterly dividend. The present yield is 3.6%, which is principally pushed by Exxon Mobil and Chevron (CVX), who account for roughly 40% of this ETF.

State Road (SPDR)

Moreover, because the overview above reveals, traders get entry to refiners as effectively. The ETF additionally consists of suppliers of power gear and companies.

This offers some diversification.

Regardless of not having the advantage of proudly owning tech shares, XLE has outperformed the S&P 500 by roughly 450 foundation factors over the previous 12 months. This consists of dividends.

Though XLE may very well be a bumpy journey if we enter a recession, I count on XLE to maintain outperforming the S&P 500 for a lot of extra years.

Takeaway

The power sector is experiencing a exceptional transformation, and the indicators level in the direction of a sustained bull market in oil. Latest developments, comparable to declining U.S. shale manufacturing progress and OPEC’s strategic output cuts, have set the stage for greater oil costs.

The provision-demand dynamics are shifting in favor of oil, with provide shortages pushing costs upward. Opposite to predictions of peak demand, world crude oil consumption continues to rise, pushed by elements like India’s rising center class.

Whereas there are differing opinions and biases within the power debate, one factor stays clear: power shares, like these within the XLE ETF, provide a stable hedge in opposition to inflation and a doubtlessly long-term uptrend in crude oil costs.

Contemplating XLE’s historical past, low expense ratio, and various holdings, it presents a compelling alternative for traders trying to profit from the power sector’s resurgence.

For my part, oil is poised for triple-digit costs, and XLE stands as a dependable automobile to navigate the power market’s alternatives and uncertainties.

{kind=link}