Trevor Williams/DigitalVision by way of Getty Photographs

Williams Firms (NYSE:WMB) is an American power firm headquartered in Oklahoma, with a greater than $35 billion market capitalization and a dividend of greater than 6%. The corporate’s spectacular asset portfolio of important pure fuel property will end in large FCF. We anticipate the corporate can flip that FCF to sturdy shareholder returns making it a robust funding.

Pure Fuel Energy Progress

The primary query for Williams Firms is what’s the long-term way forward for pure fuel.

Williams Firms Investor Presentation

Pure fuel not solely has monumental rising demand however it has distinctive advantages in ease of transport, storage, and energy supply. Extra so giant firms are supporting blue and inexperienced pure fuel as low-footprint sources of pure fuel, which is able to assist demand to stay sturdy for many years to return. In our view, pure fuel is simply in danger for these trying 50+ years sooner or later.

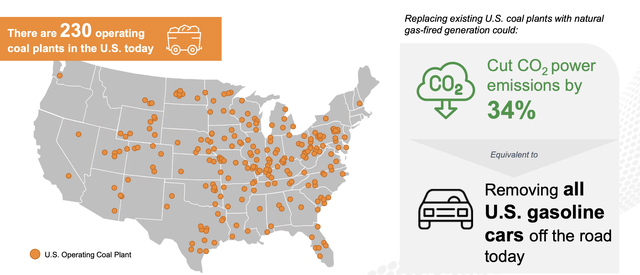

Extra so pure fuel has a novel skill within the energy infrastructure discipline. It is nearly plug-and-play in present coal plant areas, and changing it might lower CO2 energy emissions by a large 34%, equal to eradicating all gasoline automobiles in the present day. That is even higher if EVs are used with pure fuel and blue and inexperienced pure fuel grows.

That is evident, in our view, that pure fuel will proceed to develop for the long term.

Williams Firms System Power

Williams Firms has an extremely sturdy asset system that delivers pure fuel throughout the USA.

Williams Firms Investor Presentation

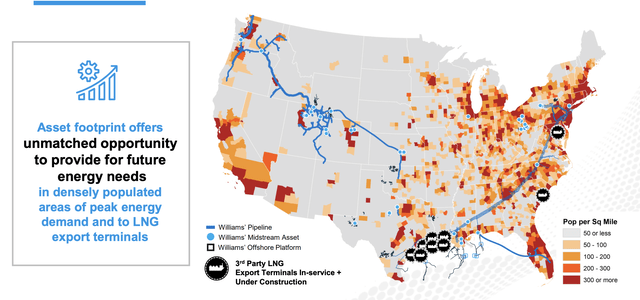

The corporate’s flagship pipeline is the Transco pipeline. It delivers 10s of billions of cubic ft / day of pure fuel throughout the USA. That features main inhabitants facilities. The corporate touches roughly 1/3 of the pure fuel in the USA and is in some main areas of development (comparable to new LNG terminals).

Extra so Appalachia is the most important supply of pure fuel reserves in the USA and notably develop to inhabitants facilities. The corporate’s system of property is properly positioned right here.

Williams Firms Monetary Efficiency

The corporate has continued to carry out properly financially, and it has a historical past of supporting shareholders.

Williams Firms Investor Presentation

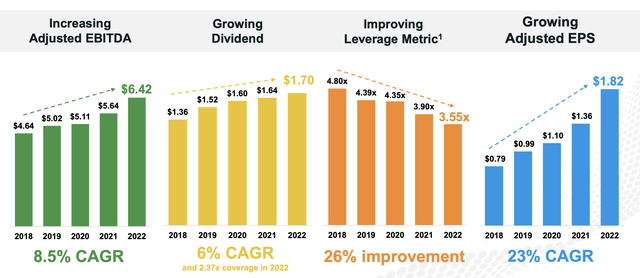

The corporate has continued to extend its adjusted EBITDA by 8.5% yearly and in line its leverage has continued to drop and its dividend has grown by 6% annualized. The corporate has a 6% dividend yield with a 2.37x protection ratio, highlighting its monetary power and double-digit yield. On the identical time, the corporate’s debt yield is manageable.

The corporate’s uncooked EPS quantity is much less essential right here. Nonetheless, the essential takeaway for buyers is that the corporate is constant to develop its dividend, one thing it may well comfortably afford, whereas persevering with to put money into its enterprise.

Williams Firms Progress Potential

The corporate has substantial development potential that it’s persevering with to put money into annually.

Williams Firms Investor Presentation

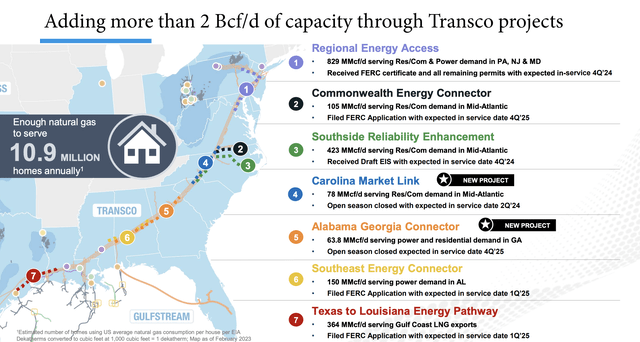

The corporate already has a robust core community of property and as we have mentioned the Transco venture is on the heart of this. Because of this, the corporate is working to incrementally enhance its asset base. The premise of that’s the skill so as to add greater than 2 Bcf/day of capability by means of Transco initiatives, sufficient to serve tens of millions of houses.

The property will enhance reliability and the corporate’s skill to generate money movement. Particularly within the north-east the corporate is working to construct out Appalachia shale and we really feel that is a market that the corporate can dominate and use to generate sturdy returns.

Our View

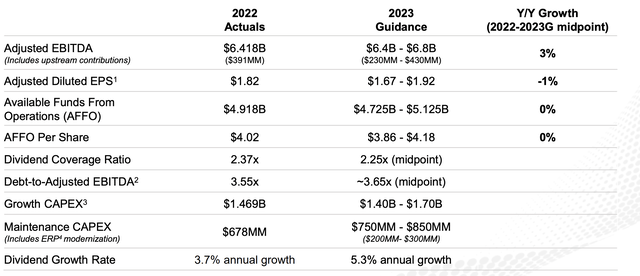

The corporate has launched its 2023 steering which might allow rising shareholder returns.

Williams Firms Investor Presentation

The corporate forecasts 3% development on the midpoint in adjusted EBITDA from $6.42 billion to $6.6 billion. Diluted EPS will lower barely whereas AFFO per share will stay roughly fixed. Nonetheless, there’s some extra essential facets to the breakdown of the corporate’s money movement and returns which can be value paying shut consideration to.

The corporate expects to generate 6% in dividends for the yr. On the identical time, the corporate is forecasting a greater than 5% dividend development fee. That is sturdy direct shareholder returns. The corporate can be guiding for greater than $1.5 billion in development capex, or a greater than 4% development capex yield, which means double-digit direct shareholder returns.

The corporate nonetheless has substantial debt, however it’s persevering with to maintain its debt manageable. The corporate expects a 3.65x debt to EBITDA ratio, or $24 billion in debt representing 40% of its enterprise worth. It is nonetheless spending >$1 billion in annual curiosity expenditures.

General, the corporate’s AFFO / share, represents a 13% yield that the corporate can comfortably afford and use to drive shareholder returns.

Thesis Threat

The dangers to our thesis are pretty minimal. In actual fact, in our view, the most important threat is that the corporate wants main revamps or replacements on its Transco pipeline and faces native opposition, much like what Enbridge has confronted with the Line 5 substitute. That would damage the corporate’s main asset and future returns.

Conclusion

Williams Firms tends to commerce at a barely larger valuation than its friends; nevertheless, we nonetheless view it as an affordable funding with sturdy potential. The corporate operates as a serious midstream pure fuel firm and pure fuel has monumental potential. That is each as a consequence of its benefits over coal together with the potential advantages of blue and inexperienced pure fuel.

Batteries, each in capability and price, are many years away from having the ability to compete with the power density of pure fuel. On the time, the expertise would not exist for the improved density. The corporate is constant to realize development with incremental additions to Transco and we anticipate that dividends and shareholder returns will develop.

General, because of the corporate’s total portfolio, we view Williams Firms as a priceless long-term funding. Tell us your ideas within the feedback under.

{kind=link}