After a barrage of US information harm the greenback this week, with buyers having second ideas as as to if one other Fed hike could also be wanted, the US agenda will develop into lighter subsequent week with the highlight turning to the ISM non-manufacturing PMI. Elsewhere, the RBA and the BoC are holding their rate of interest selections, kick-starting a spherical of pivotal conferences by main central banks, which may effectively affect forthcoming instructions of main forex pairs.

Mild US agenda, concentrate on ISM non-mfg PMI

The US greenback pulled again this week as a number of US information compelled buyers to rethink the chance of one other hike by the Fed earlier than the tip credit of this tightening campaign roll, and so as to add extra foundation factors price of price cuts for subsequent yr.

Simply after Fed Chair Powell saved the prospect of extra price will increase alive at Jackson Gap, buyers lifted barely their implied path, however on Tuesday, job openings for July hit their lowest since March 2021 and client sentiment for August deteriorated, whereas on Wednesday, the ADP employment report revealed that the US personal sector added much less jobs than anticipated throughout August.

Buyers had second ideas after the information and at present, they’re evenly break up on whether or not one other hike by November is warranted. The US agenda can be gentle within the coming week, with Monday being a vacation as a consequence of Labor Day, however there’s a information level that might effectively affect expectations relating to the Fed’s plans, and that is the ISM non-manufacturing PMI on Wednesday.

The preliminary manufacturing and providers PMIs from S&P World each confounded market expectations of largely unchanged factors and as an alternative declined in August. With that in thoughts, the dangers surrounding the ISM index could also be tilted to the draw back. That stated, whether or not the chance of one other Fed hike will additional decline may additionally depend upon the brand new orders and costs subindices. If there are declines there as effectively, the greenback and Treasury yields may keep beneath stress and equities could proceed drifting larger as expectations of decrease rates of interest may preserve the web current worth (NPV) of high-growth companies elevated.

Aussie awaits RBA and Chinese language information

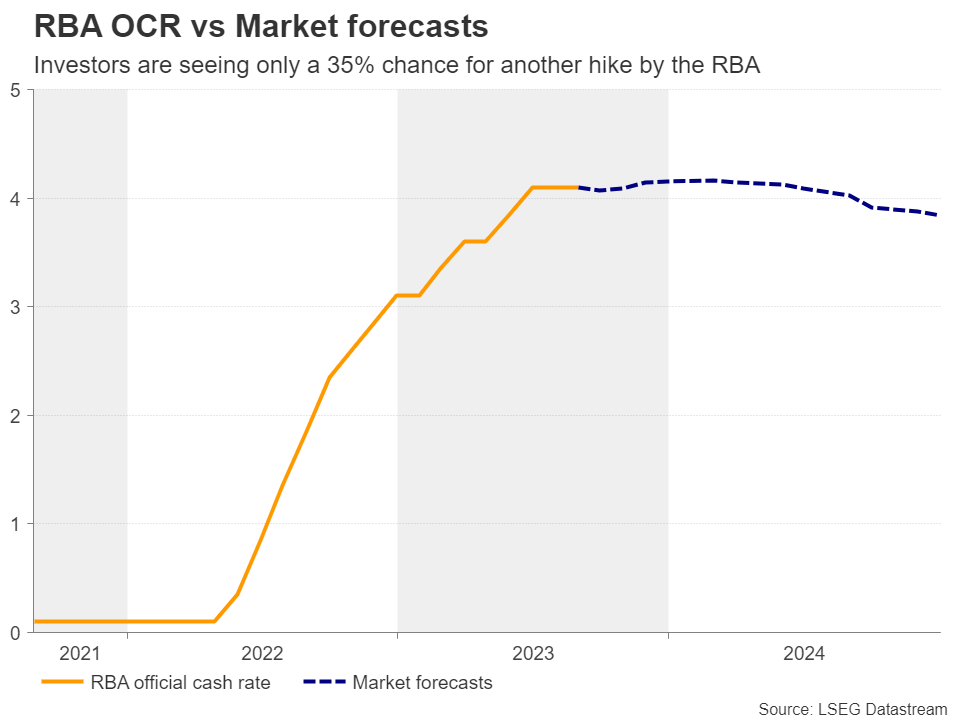

On Tuesday, the Reserve Financial institution of Australia begins a collection of central financial institution conferences that might show crucial in guiding market expectations relating to the way forward for financial coverage within the main economies. At their final assembly, officers stood pat, disappointing expectations of a price hike, however leaving the door open to extra motion by saying that some additional tightening of financial coverage could also be required, but additionally that this can depend on the information and the evolving evaluation of threat.

Since then, the employment information for July revealed that the financial system has misplaced jobs as an alternative of gaining, with the unemployment price rising to three.7% from 3.5%. On high of that, CPI numbers for the month of July confirmed that headline inflation in Australia dropped to 4.9% y/y from 5.4%, which eradicated any hypothesis almost about a possible hike at this gathering.

At present, buyers are almost sure that policymakers will preserve their arms off the hike button at this assembly, whereas they’re assigning round solely a 35% chance for one more quarter-point improve to be delivered by the tip of the yr.

Having stated that although, with the core month-to-month CPI price sliding solely to five.8% y/y from 6.1%, nonetheless effectively above the Financial institution’s inflation goal vary of 2-3%, closing the door to extra hikes could also be an unwise selection. Subsequently, if policymakers reiterate the steerage that some additional tightening could also be required, even when they stand pat at this assembly, the chance for one more hike earlier than the tip of this yr may rise, serving to the prolong its newest restoration.

That stated, financial coverage developments on their very own will not be sufficient to avoid wasting the risk-linked forex, which has been delicate additionally to developments and expectations surrounding China, Australia’s primary buying and selling accomplice.

China has been within the highlight currently, with information pointing to deepening financial wounds and responses by authorities not convincing market members that they may have the specified impact. With that in thoughts, China’s commerce information on Thursday, in addition to the CPI and PPI numbers on Friday, may appeal to particular consideration. Additional weak point in Chinese language exports and imports, in addition to one other month of deflation may immediate merchants to promote the aussie, which may erase any RBA decision-related features.

Australia’s personal commerce information are additionally as a consequence of be launched on Thursday, whereas the day earlier than, the nation releases its GDP numbers for Q2.

BoC seen holding fireplace, steerage and jobs information in focus

Moreover the aussie, one other risk-linked forex will enter the limelight subsequent week and that’s the , with the Financial institution of Canada holding its personal rate of interest determination on Wednesday.

On the July gathering, this Financial institution determined to push the hike button, lifting rates of interest by 25bps, however shunned clearly telegraphing future strikes. Officers simply famous that they’ll proceed to evaluate the dynamics and the outlook for inflation and that they continue to be dedicated to restoring worth stability.

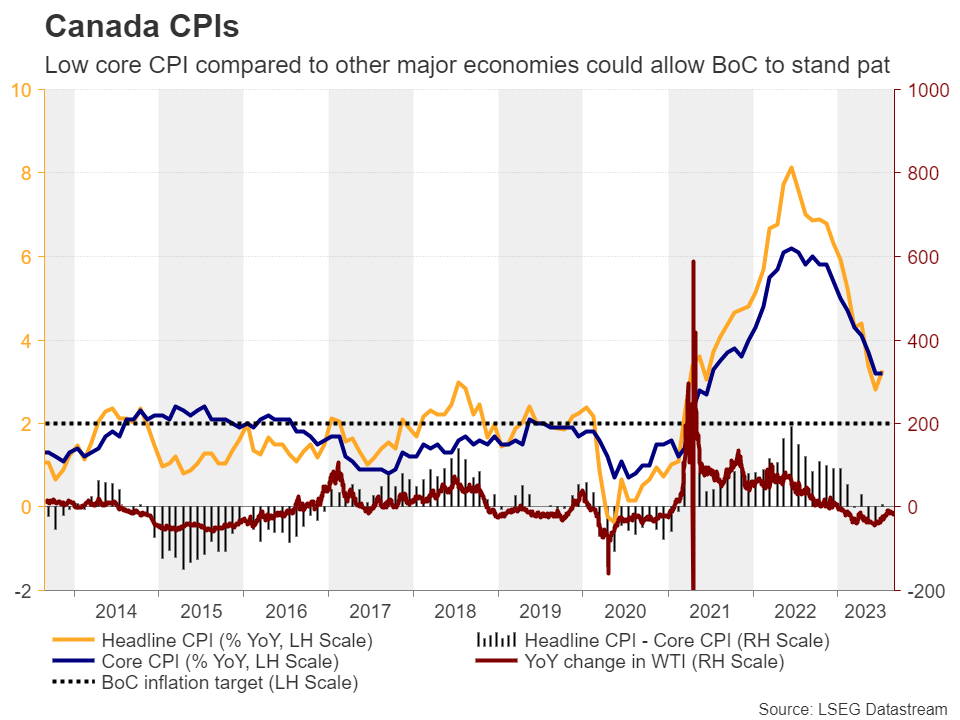

Inflation information for June revealed a notable slowdown in each headline and core phrases, however the July numbers pointed to some stickiness, with the headline price rebounding to three.3% y/y from 2.8%, and the core one holding regular at 3.2%.

This will likely have prompted market members to maintain the choice of one other hike by the tip of the yr firmly on the desk. Though they see solely a 20% probability for motion subsequent week, they’re assigning round a 50% chance for one more 25bps hike by December.

Sure, inflation is above the Financial institution’s 2% goal, however with Canada’s core price being nearer to that quantity than underlying inflation charges in different main economies, and with the BoC sustaining a flexibility vary round that focus on between 1-3%, officers could have the posh to remain sidelined now and wait to see whether or not previous hikes are nonetheless exerting draw back stress on costs.

That stated, equally to the RBA, closing the door to future hikes earlier than the target is met could also be a untimely selection. Thus, even when they stand pat, Canadian policymakers may preserve alive the opportunity of extra motion if deemed essential. This can verify the view of these assigning respectable probabilities for one more transfer within the coming months and thus, it could permit the loonie to achieve some floor.

Nonetheless, whether or not the forex may have a sustained and respectable post-meeting restoration could largely depend upon Friday’s employment report for August. The July numbers pointed to some weak point, with the financial system dropping some jobs and the unemployment price rising additional. Ought to subsequent week’s information reveal deeper wounds, these anticipating one other BoC price improve could begin having second ideas. For the chance of additional motion to maintain rising and take the loonie larger, enhancing labor-market situations could also be required.

{kind=link}