Effectively, after all somebody has observed: to start with, the debtors of variable-rate mortgages who’ve seen their repayments skyrocket, or those that wish to apply for a brand new one or refinance their outdated one. Within the US the official mortgage charge has reached 7.09%, within the UK the charges on 2-year and 5-year loans are each properly above 6%.

Even small and medium-sized firms – those that can not challenge debt – have seen their prices skyrocket and a few have merely been excluded from the opportunity of a financial institution mortgage (particularly in Europe because the ECB famous in its newest survey). However the SP500, the inventory indices, appear to not have observed.

The above chart reveals the Dividend Yield on US500: it’s the common yield that an investor can get from the dividend paid by the shares included on this index. It sits at 1.49% proper now, properly beneath the long-term common (2.88%); the chart reveals that it’s about 1 sigma, 1 commonplace deviation beneath the common. This can be a very low stage, just like what has been reached between the bursting of the tech bubble in the beginning of the millennium and the GFC. It has been reasonably low for some time now really; throughout the entire 10s decade, it hovered round 2%. However again then the rates of interest – the cash you would earn by shopping for the lower-risk debt securities (bonds, payments, notes) – had been 0% or damaging. In brief, a lot lower than now.

Take Warren Buffett: he’s identified to be a long-term investor, not all for even deep fluctuations within the share worth. What he’s in search of is a gentle and safe movement of earnings through the years from what the inventory pays – dividends.

The identical is true for a lot of institutional traders, particularly funds. For them, the selection is between completely different asset courses – in addition to between completely different firms: why accept a mean of 1.49% when shopping for one-year US debt can get you 5.4%? And if you’re based mostly in Europe, you should buy 1-year Italian BOT at 3.8%? The scenario was actually not the identical 3 years in the past. But, indices are nonetheless purchased strongly.

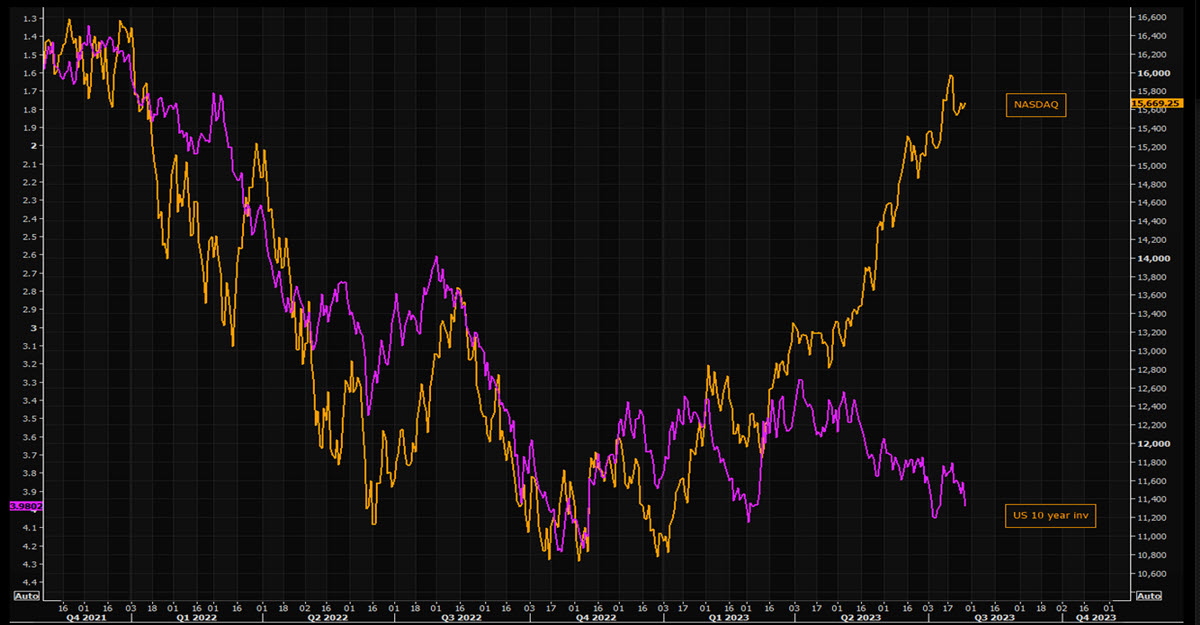

US100 vs. Inverted 10Y Yield

The above chart reveals the divergence between US100 costs and the (inverted) US 10y yields, typically properly correlated due to the dependency of many progress shares on future anticipated money flows: has this divergence damaged? Are we in a brand new regular? Or are we set for a classical imply reversal transfer in some unspecified time in the future?

Click on right here to entry our Financial Calendar

Marco Turatti

Market Analyst

Disclaimer: This materials is supplied as a common advertising communication for info functions solely and doesn’t represent an unbiased funding analysis. Nothing on this communication comprises, or needs to be thought of as containing, an funding recommendation or an funding suggestion or a solicitation for the aim of shopping for or promoting of any monetary instrument. All info supplied is gathered from respected sources and any info containing a sign of previous efficiency will not be a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature includes a excessive stage of threat for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made based mostly on the data supplied on this communication. This communication should not be reproduced or additional distributed with out our prior written permission.

{kind=link}