porcorex

Selection is the spice of life, and the identical goes for investments, too. Whereas it might be laborious to go mistaken with so-called ‘sleep nicely at evening’ shares like Important Road Capital (MAIN) within the BDC house, some traders might discover it interesting to succeed in for greater yield whereas additionally getting the peace of thoughts of not having all their eggs in a single basket.

This brings me to Trinity Capital (NASDAQ:TRIN), which is a relative newcomer within the BDC house. Like lots of TRIN’s friends, it is seen first rate share worth efficiency over the previous 12 months, however the previous 30 days have proved difficult with the broader market downturn. On this piece, I focus on what makes now buy-the-dip alternative, so let’s get began!

TRIN Inventory (Looking for Alpha)

Why TRIN?

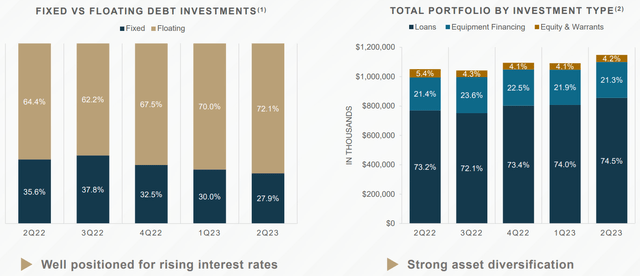

Trinity Capital is one in all a handful of internally managed BDCs and focuses on growth-stage corporations which might be usually backed by enterprise capital. At current, it carries a $1.15 billion portfolio that is composed primarily of secured loans (75% of the portfolio), adopted by gear financing (21%), and fairness and warrant investments (4%).

TRIN’s portfolio resembles that of growth-oriented peer, Hercules Capital (HTGC), with a tilt towards expertise and life science. It additionally has a little bit of bread and butter industries like that of Important Road Capital with client merchandise and finance, insurance coverage, and healthcare within the combine.

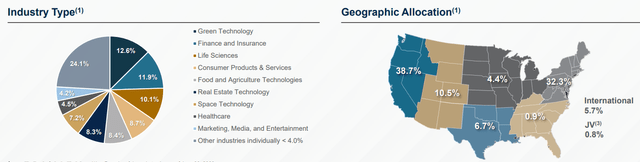

As proven under, Inexperienced Expertise, Finance & Insurance coverage, Life Science, Shopper Merchandise & Companies, and Meals Applied sciences make up TRIN’s 5 industries, comprising simply over half of its portfolio, and TRIN is diversified by geography with greater concentrations alongside the West Coast and Northeast, the place development industries are primarily positioned.

Investor Presentation

Like different BDCs, TRIN is benefitting from greater rates of interest, which has resulted in TRIN’s efficient yield on investments rising by 240 foundation factors over the previous 12 reported months to 16.2%. This has helped TRIN obtain a $0.61 NII per share through the second quarter, which is up $0.06 on a sequential foundation from the Q1 charge of $0.55. TRIN can also be well-positioned to learn from a ‘higher-for-longer’ charge setting that the market now extensively expects after the Federal Reserve’s assembly in September.

TRIN is well-positioned for one of these charge setting, because it has shifted the portfolio extra towards floating-rate loans. Administration estimates that annualized NII per share will increase by $0.15 for each 100 foundation level rise in rates of interest. As proven under, the share of floating-rate debt investments has risen materially by 7.7% over the previous 12 reported months, from 64.4% to 72.1%.

Investor Presentation

Dangers to TRIN embrace the cyclical nature of the tech trade and the headwinds they face from greater rates of interest. Which means that portfolio exits by way of IPO or M&A are much less commonplace given the upper price of capital that these corporations face, and as such, TRIN will not have the ability to develop its NAV/share by way of its fairness investments as a lot in comparison with a wholesome IPO setting.

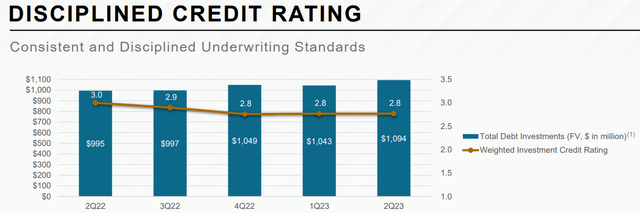

Additionally, decrease rates of interest would imply a decrease NII/share, however that situation doesn’t appear possible within the foreseeable future. As proven under, TRIN’s portfolio credit score rating barely declined final 12 months from 3.0 to 2.8 (on a scale from 1 to five, with 5 being the best performing), however has held regular to this point this 12 months.

Investor Presentation

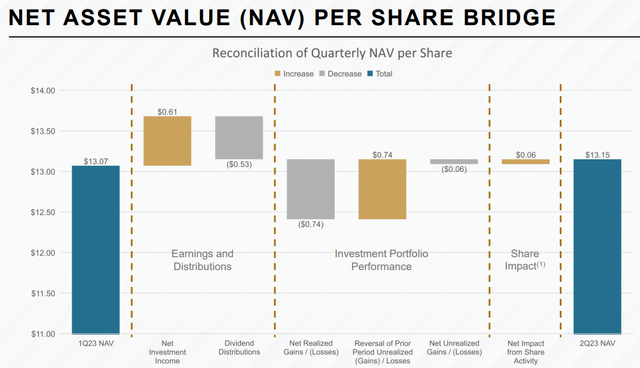

Nonetheless, TRIN’s investments in non-accrual declined since earlier this 12 months and sit at a modest 2% of portfolio worth. That is value monitoring, as I would prefer to see that decline all the way down to the 1-1.5% vary over time. As well as, TRIN has seen an enchancment in its NAV per share on a sequential foundation, pushed by greater web funding earnings, reversal of earlier mark to market (unrealized) loss, and accretive fairness issuances.

Investor Presentation

Importantly for earnings traders, TRIN presently yields a formidable 14.5% primarily based on the common dividend alone, with the potential for a better yield by way of particular dividends. The common dividend is well-protected by an 80% payout ratio. TRIN has lately been paying out about half of its NII to common dividend overage with $0.05 particular dividends, leaving loads of retained capital to fund development. TRIN additionally carries an affordable quantity of leverage with a 138% debt to fairness ratio, sitting under the 200% statutory restrict.

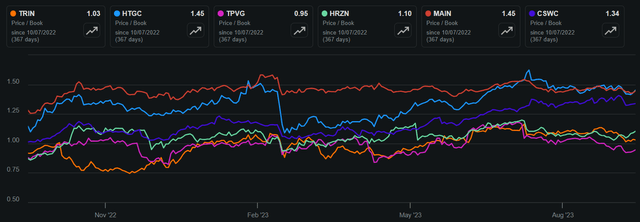

Lastly, I see worth in TRIN on the present worth of $13.54 with a worth to guide worth of 1.03x. As proven under, this sits simply above that of peer TriplePoint Enterprise Progress (TPVG), whereas sitting materially under that of Horizon Expertise Finance (HRZN) and internally managed friends Important Road Capital, Hercules Capital, and Capital Southwest (CSWC).

TRIN & Friends Value-to-Ebook (Looking for Alpha)

Utilizing the next NPV evaluation, I got here up with a good worth worth of $15.93, which sits barely above the analyst consensus common worth goal of $15.50. That is primarily based on the present 12 months’s EPS estimate of $2.23, a conservative 0% development charge, since TRIN pays out most of its earnings, and a ten% low cost charge to account for the upper threat nature of TRIN resulting from publicity to rising development industries. This truthful worth sits meaningfully above the $13.54 present share worth.

NPV Evaluation (Produced By Writer)

Investor Takeaway

All in all, Trinity Capital seems to be a well-managed internally managed BDC that gives publicity to engaging growth-stage corporations backed by enterprise capital. It is set to learn from a better for longer rate of interest setting.

With its diversified portfolio of industries and geography, give attention to floating charge loans, spectacular dividend yield, and potential for NAV/share development by way of fairness investments, I see worth in TRIN on the present worth. Lastly, TRIN seems to be undervalued primarily based on my valuation evaluation and trades at a reduction to most of its friends.

{kind=link}