Klaus Vedfelt/DigitalVision through Getty Photos

In my writing, I are inclined to give attention to dividend-paying ETFs with robust yields, returns, and purchase scores. I typically write about weaker ETFs, to warn buyers about their shortcomings and supply appropriate alternate options. On this article, I’ll give a fast overview of three such ETFs.

HYG – Costly Excessive-Yield Bond ETF

The iShares iBoxx $ Excessive Yield Company Bond ETF (HYG) is the most important high-yield bond ETF out there, with $16.5B in property. HYG can also be one of the costly high-yield bond ETFs, with a 0.49% expense ratio. It’s round twice the business common, with a number of ETFs providing sub 0.10% bills. Of the highest ten ETFs on this sector, solely the First Belief Tactical Excessive Yield ETF (HYLS) is costlier, with a 1.02% expense ratio.

In search of Alpha – Desk by Writer

Bills straight scale back HYG’s dividend yield and returns, two vital, easy negatives for the fund and its shareholders.

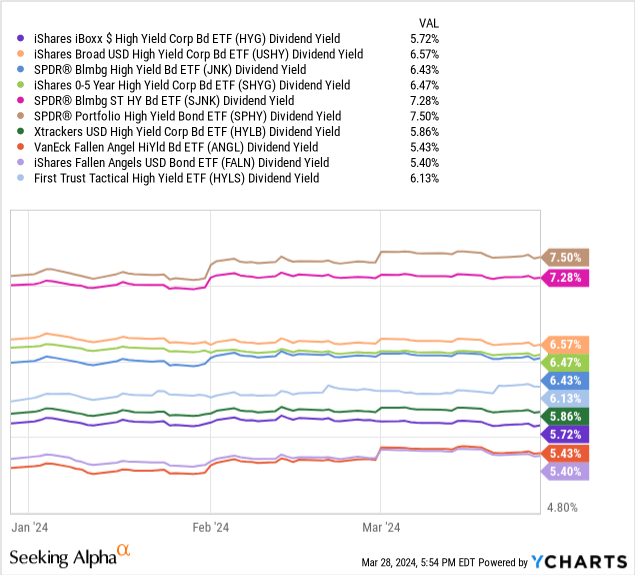

Particularly, HYG’s present 5.7% yield is kind of a bit decrease than common. Solely the iShares Fallen Angels USD Bond ETF (FALN) and the VanEck Fallen Angel Excessive Yield Bond ETF (ANGL) yield lower than HYG, however the methods employed by these funds, and their returns, are a lot stronger.

Information by YCharts

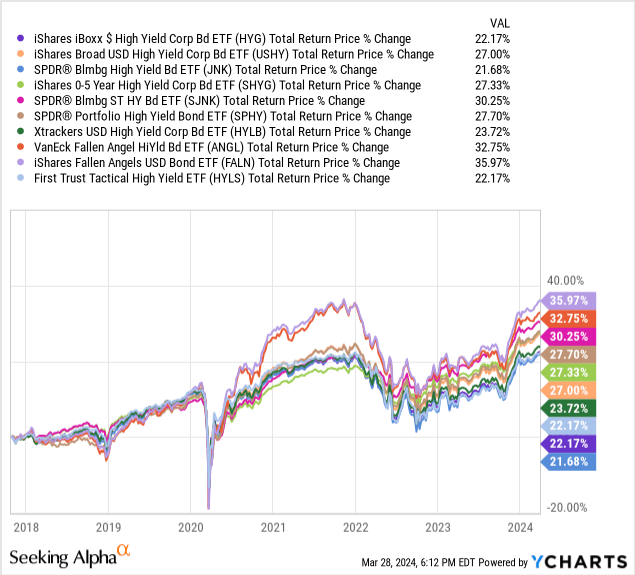

HYG’s complete returns are a lot weaker than common too, though a few different funds have broadly comparable efficiency. HYG’s excessive bills are liable for a good portion of the fund’s underperformance.

Information by YCharts

As HYG is a straightforward index ETF, it offers no different significant profit or benefit that might counteract its bills. Leveraged funds would possibly generate extra revenue, as an illustration, however HYG doesn’t. Actively-managed funds would possibly generate alpha or extra returns, however HYG can’t. Some extra focused index funds would possibly give attention to best-performing securities, reminiscent of ANGL and FALN, however HYG doesn’t.

Contemplating the above, I consider there may be mainly no motive to decide on the costly HYG over its cheaper friends. As an alternative of HYG, buyers may purchase the SPDR Portfolio Excessive Yield Bond ETF (SPHY), with a a lot decrease 0.05% expense ratio, and a a lot larger 7.5% dividend yield. Returns are stronger too, as anticipated. Buyers even have the selection of ANLG and FALN. Each are considerably cheaper, with 0.25% expense ratios. Each have barely decrease 5.4% dividend yields, however a lot stronger returns.

BIL – Easy T-Payments ETF

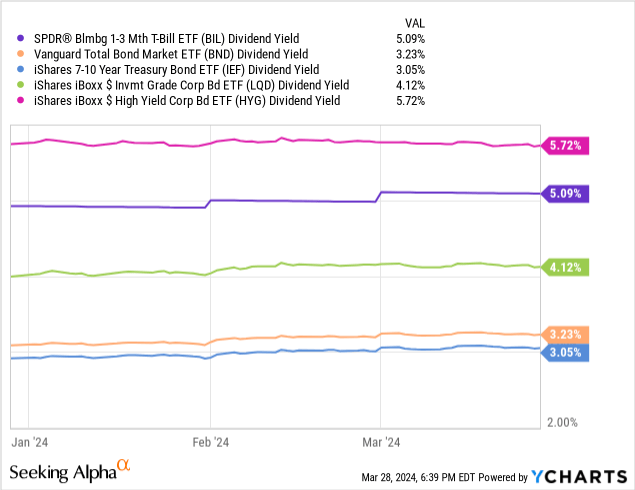

The SPDR Bloomberg 1-3 Month T-Invoice ETF (BIL) is a straightforward index ETF, with all of the traits and advantages that entails. Particularly, Fed hikes have prompted t-bill yields to spike, with the fund itself yielding 5.1%, greater than most different bonds apart from high-yield bonds.

Information by YCharts

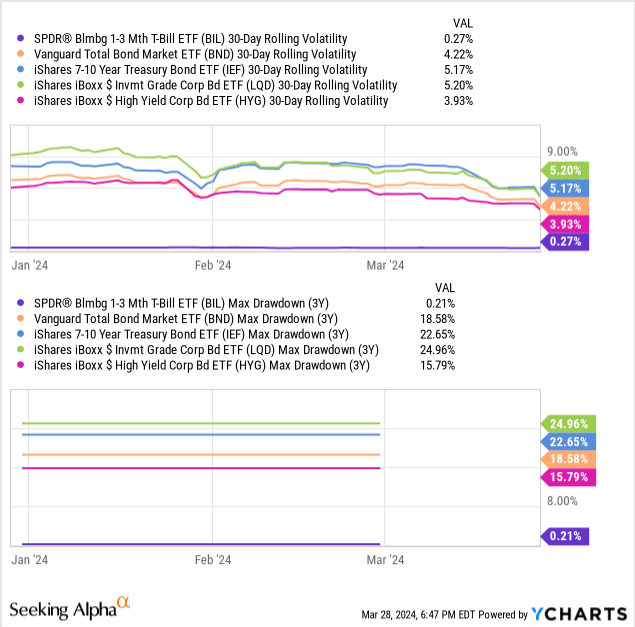

Threat, volatility, and drawdowns are fairly minimal too. In follow, many of the fund’s (tiny) volatility is because of briefly retaining revenue throughout the fund, after which distributing it to shareholders.

Information by YCharts

BIL’s 0.14% expense ratio is about common for a easy fixed-income ETF. Some buyers would possibly desire to construct their very own private t-bill portfolio to keep away from these bills, however these don’t appear terribly costly both manner.

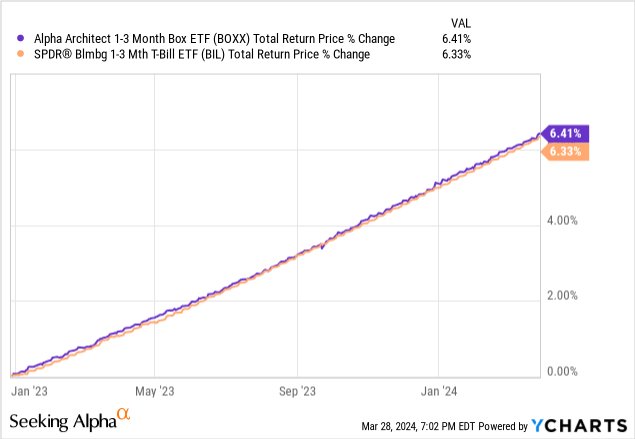

For my part, BIL has no vital dangers or negatives. I nonetheless suppose buyers ought to keep away from the fund for a easy motive: the Alpha Architect 1-3 Month Field ETF (BOXX) does every part BIL does, however higher.

BOXX achieves comparable returns to t-bills by way of fairness choices. An in-depth rationalization of those is exterior the scope of this text however see right here for one. BOXX’s returns have virtually similar to these of BIL since inception, as anticipated.

Information by YCharts

BOXX does have two benefits relative to BIL.

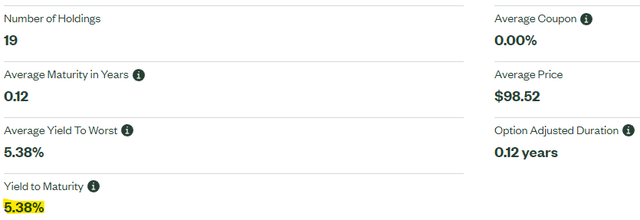

First, BOXX tends to have a touch larger yield and return. Proper now, the fund sports activities a yield to choice expiration of 5.8%, in comparison with BIL’s 5.4% yield to maturity. Spreads are usually tighter, however optimistic.

BOXX BIL

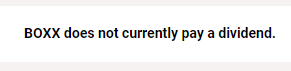

Second, the fund has some potential tax advantages. Particularly, technique mustn’t generate taxable occasions for both the fund or its shareholders, with the fund retaining any revenue and returns inside itself, and with no dividend funds.

In search of Alpha

Buyers in BOXX can select to carry the fund long-term, deferring taxes till a second of their selecting. Doing so may, doubtlessly, end in tax financial savings.

BOXX’s marginally larger, tax-deferred 5.8% yield appears strictly superior to BIL’s. As such, I might a lot sooner spend money on BOXX over BIL.

MORT – Dangerous mREIT ETF

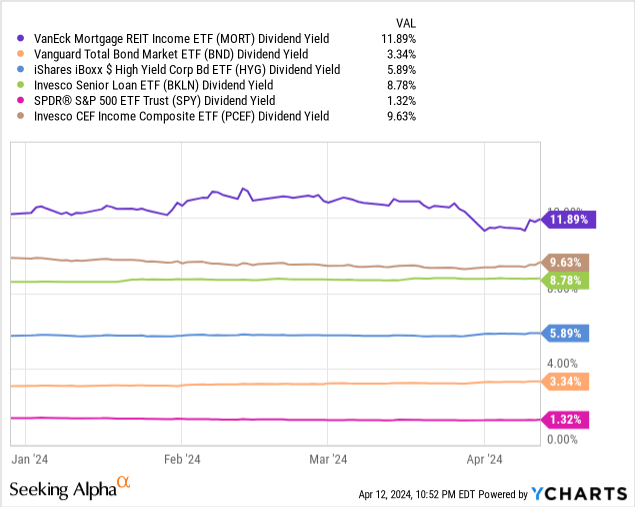

The VanEck Mortgage REIT Revenue ETF (MORT) invests in mREITs, monetary establishments specializing in leveraged mortgage investments. These establishments are inclined to sport robust dividend yields, with the fund itself yielding a whopping 11.9%. MORT yields greater than most bonds, high-yield bonds, senior loans, equities, even CEFs, and by very wholesome margins.

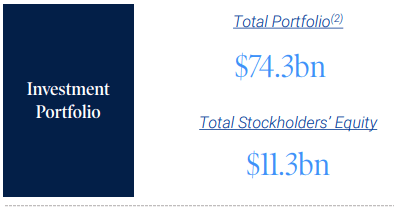

mREIT leverage ratios are additionally usually fairly excessive, with Annaly Capital Administration (NLY) managing a $74.3B portfolio with solely $11.3B in fairness. In different phrases, for each greenback of fairness, the corporate has six {dollars} of debt, a staggering quantity.

Annaly

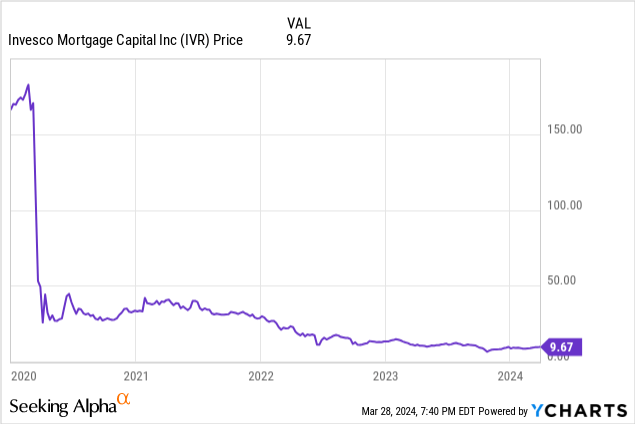

Annaly’s large debt load boosts the corporate’s dividends, but in addition its threat. Default charges of 10% would trigger vital points for the fund, default charges a bit larger would imply rapid insolvency, and certain chapter. These usually are not idle threats, with mREITs do often imploding, rather more so than common. For example, the Invesco Mortgage Capital (IVR) noticed large losses throughout early 2020. As a result of their magnitude, losses have been successfully irrecoverable, with share costs nonetheless massively down from pre-pandemic developments.

Information by YCharts

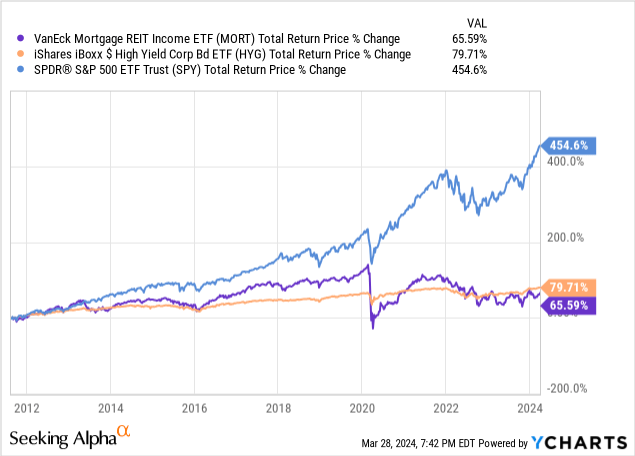

For my part, mREITs are typically excessively leveraged, so vital investments in these, particularly as an asset class, are unwise. Smaller, focused investments in the very best of those would possibly make extra sense. MORT focuses on the latter, making the fund a broadly sup-par funding. MORT has seen weaker returns than equities and high-yield company bonds since inception, and with considerably larger threat and volatility, in-line with expectations.

Information by YCharts

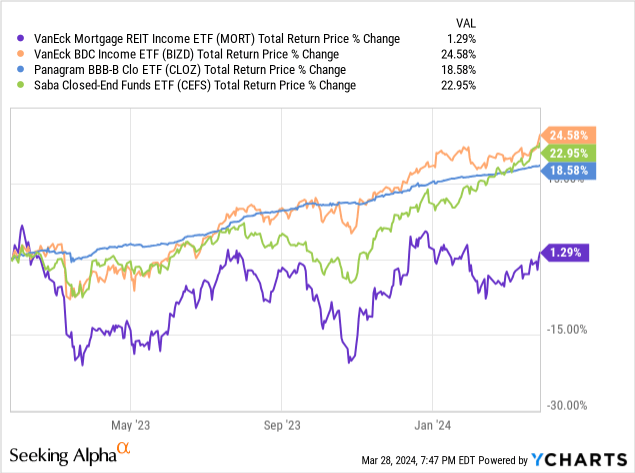

For my part, buyers on the lookout for notably robust yields have a lot better alternate options to MORT.

The VanEck BDC Revenue ETF (BIZD), specializing in BDCs, gives a rising 10.9% yield. Though it yields a bit lower than MORT, returns are a lot stronger.

The Panagram BBB-B Clo ETF (CLOZ), specializing in BBB-BB CLO tranches, gives a decrease 9.4% yield. Returns are larger, too.

Lastly, the Saba Closed-Finish Funds ETF (CEFS), holding a diversified portfolio of CEFs, has a considerably decrease 8.3% yield, but in addition larger returns.

The funds above have decrease yields, however a lot stronger efficiency and dividend progress track-records.

Information by YCharts

Conclusion

HYG, BIL, and MORT are three dividend-paying ETFs. Though every fund has its benefits, every has stronger alternate options, and so I might not be investing in any of those funds.

{kind=link}