by confoundedinterest17

This would be the final time (Fed charge hikes) because the US financial system is forecast to both go right into a recession in 2023 or decelerate to an anemic 1.20% Actual GDP YoY. Even the Fed is forecasting 3.10% core inflation in 2023, nonetheless increased than their goal charge of two%.

One of many sectors that’s struggling is industrial actual property.

Industrial mortgage bonds may get clobbered within the coming months, and traders are backing away from the securities.

Some $34 billion of the bonds come due in 2023, and refinancing property loans is tough now. Property costs may fall 10% to fifteen% subsequent yr, in line with JPMorgan Chase & Co. strategists. And a few varieties of properties appear significantly weak as, for instance, metropolis employees are gradual to return again to their places of work full time.

Which may be why spreads on BBB industrial mortgage bonds have widened by about 2.7 proportion factors this yr via Thursday to round 6.6%, for the securities with out authorities backing. They’re now at their widest since January 2021. They’ve been getting hit significantly laborious in the previous few months, whilst threat premiums on investment-grade and high-yield corporates have been shrinking on hopes the Federal Reserve will cut back its tightening marketing campaign.

“For CMBS traders, there’s a number of uncertainty, particularly round whether or not maturing loans are going to get refinanced or not, and if not, what the decision can be,” stated David Goodson, head of securitized credit score at Voya Funding Administration, in an interview. “Layering in threat from decrease workplace utilization makes the evaluation even harder.”

The difficulty that the bonds face received’t essentially translate to a surge in defaults within the close to time period, which is a part of why betting in opposition to them is so tough. When property house owners can’t refinance mortgages which were bundled into bonds, noteholders have a tough option to make. They will seize the buildings and liquidate them, or they will prolong the debt and settle for compensation later. They normally go for the second choice.

Extending maturities permits bondholders to kick the can down the street and doubtlessly get well extra later, stated Stav Gaon, head of securitized merchandise analysis at Academy Securities. The query is whether or not properties have completely misplaced worth as, for instance, folks reorder their lives after the pandemic, or whether or not declines could also be extra momentary due to increased charges.

“Foreclosing on a mortgage, moderately than granting an extension, will be actually messy — that’s a lesson that was realized throughout the nice monetary disaster,” stated Gaon. “The lenders additionally acknowledge that at present’s increased rates of interest are a really sudden improvement that many high-quality debtors want time to regulate to.”

Some traders which can be nonetheless shopping for are specializing in higher-quality debtors and properties, which can be likelier to face up to any downturn in actual property costs with out having to hunt extensions on loans.

“We predict trophy properties will fare higher resulting from higher entry to the debt markets, decrease potential property declines, and a continued tenant flight to high quality,” stated Zach Winters, senior credit score analyst at USAA Investments.

He acknowledges that this technique isn’t at all times fashionable now, even when it seems to make sense.

“After we exit and bid on a bond tied to a trophy workplace constructing now, normally the variety of patrons is considerably lower than earlier than,” Winters stated.

After the Pandemic

The marketplace for industrial mortgage bonds with out authorities backing was about $670 billion as of the top of 2021, and though the securities soared within the second half of 2020 because the Fed opened the cash spigots, they’re going through extra problem now. With workplace occupancy nonetheless under 50% in lots of cities as extra folks earn a living from home, company buildings might even see their values drop. Retail area is equally beneath strain as customers have grown used to purchasing extra on-line. And whereas journey quantity is rising, many accommodations are struggling to achieve 2019 ranges for room prices.

A survey of institutional actual property market professionals in November discovered that companies anticipate workplace values to fall about 10% subsequent yr, and total industrial property declines of 5%, in line with the Pension Actual Property Affiliation.

The $34 billion of bonds due subsequent yr consists of largely fixed-rate CMBS bonds bought with out authorities backing. It’s a steep improve from the $24.4 billion of such bonds maturing this yr, in line with Academy Securities.

There’s one other $103 billion of a sort of CMBS referred to as single-asset single-borrower bonds maturing subsequent yr, in line with Academy — though most of that debt pile has a built-in contractual potential to increase loans, which means they’ll have the ability to search extensions extra simply.

Subsequent yr received’t be the primary time that CMBS bondholders and servicers have confronted robust decisions about whether or not to permit en masse extensions to the underlying debtors. After the 2008 monetary disaster, industrial property values plummeted and lots of lenders selected to provide house owners of these properties extra time to pay again their loans. In consequence they ended up getting extra money again than in the event that they’d instantly foreclosed on the loans and liquidated the properties, stated Jeff Berenbaum, head of CMBS and company CMBS technique at Citigroup.

By way of watchlisted CMBS loans, at the moment many of the USA is within the inexperienced (good) aside from San Francisco, New Orleans, Memphis and Chicago all have elevated industrial loans on the watchlist (loans being watched for going late and into default). Puerto Rico can also be within the crimson (>25%) watchlisted industrial loans, so I anticipate AOC to be asking for a bailout.

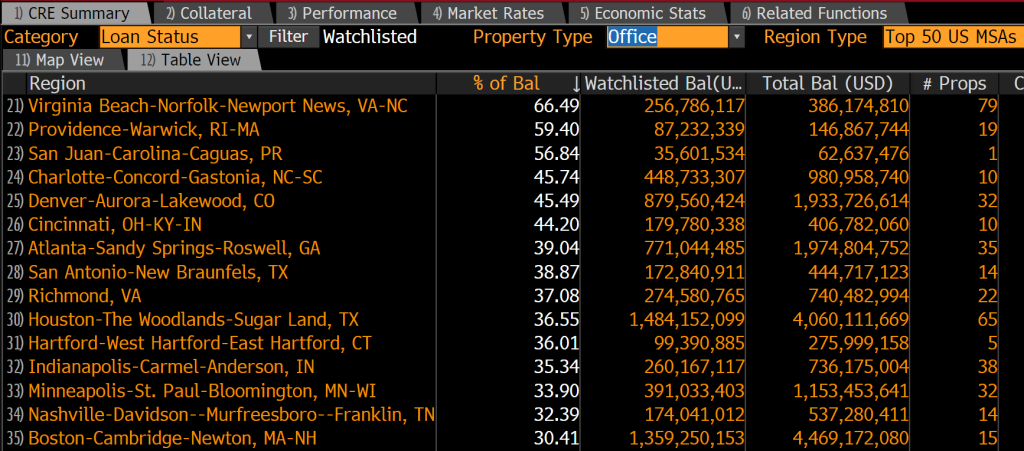

On the workplace property entrance, we are able to see crimson (>25% of economic loans watchlisted) just about throughout the board.

The main metro space by way of watchlisted workplace property loans is … Virginia Seaside-Norfolk-Newport Information VA-NC at 66.49% (that’s fairly unhealthy). Windfall RI is second and San Juan Puerto Rico is third adopted by Charlotte NC in fourth place. The one Ohio metropolis in prime 15 is Cincinnati, residence of Skyline Chili and Montgomery Inn.

Whereas most are calling for extra charge hikes in 2023, I predicted that December’s doubtless 50 foundation level hike with be the final one for some time because the US financial system grinds to a halt. Or it’s throughout now for Fed charge hikes.

Whereas The Fed predicts gradual progress, markets are pointing to recession. The Fed is out of contact with actuality. As is the US Secretarty of Treasury, “Too low for too lengthy” Janet Yellen.

{kind=link}