Petmal

The world is moving towards a more sustainable future, but the transition seems challenged by the pandemic and ongoing inflationary pressures. However, the recently enacted Inflation Reduction Act, which promotes investments in clean energy, provided a positive catalyst for the overall clean energy industry. In fact, analysts believe that the US will outpace its emission reduction target by 2030. Stem, Inc. (NYSE:STEM), as one of the leading companies that provides intelligent energy storage networks, is well positioned to benefit in this growing energy storage market.

In its Q2 2022, STEM showed a positive bottom line of $27.1 million, a better performance than its peers, but this is due to a non-recurring gain incurred in Q3 2021. I believe the company still has a few years to prove itself profitable. Although there is some improvement, especially looking at its gross margin, it is not enough to translate to positive operating income. Looking forward, its adjusted EBITDA outlook still remains on a declining trend, which makes this stock a bit risky with today’s uncertainties. Additionally, STEM is a bit pricey as of this writing with a P/S ratio of 12.71x compared to its peers’ average of 6.77x. I believe waiting for a possible correction will make the risk/reward better than entering at these levels.

Company Overview

The Inflation Reduction Act Law has been a good catalyst for STEM. Its TAM is forecasted to grow by between 20% to 300%, according to market research firms Wood Mackenzie and BNEF. Even though this is a third-party estimate, it would be nice to hear the management’s thoughts on the company’s financial outlook in the long run.

Going forward, STEM is enjoying a positive synergy with its AlsoEnergy acquisition. According to the management, they ranked number one for solar and storage monitoring and control and expect a significant boost on integration, which promotes cross-selling opportunities.

In fact, the company ended the quarter with $66.9 million, up from $41.1 million in Q1 2022 and $19.3 million recorded in Q2 2021. According to the management, it remains elevated on its Q4 2021 performance, as quoted below.

The quarterly revenue performance surpassed the Q4 2021 performance of $53 million or an increase of 26%. Most of the growth came from the storage hardware sales on FTM and BTM partner projects and about $14 million from the addition of AlsoEnergy. Source: Q2 2022 Earnings Call Transcript

This $14 million addition from AlsoEnergy is actually good; however, upon further investigation, this is quite short from its $15.6 million normalized quarterly level, where AlsoEnergy recorded an annual revenue of $62.56 million in December 2021. On the other hand, STEM has positive gross margins both on a GAAP and Non-GAAP basis of 12% and 17%, respectively, improving on a year over year basis. This may improve further, thanks again to its AlsoEnergy acquisition, where management expects continued efficiency with a 15% to 20% Non-GAAP gross margin in FY22, better than the 11% recorded in FY21 and the 10% recorded in FY20.

This snowballed into its improving total operating expense ratio, as shown in the image below.

STEM: Improving Total Operating Expense Ratio (Source: Data from Seeking Alpha. Prepared by InvestOhTrader)

With these improving metrics, I believe STEM has the ability to experience a positive turnaround in the next few years. However, upon crunching up the numbers further, we can see that there is some slowness on its R&D spending.

STEM: Declining R&D Expense Ratio (Source: Data from Seeking Alpha. Prepared by InvestOhTrader)

This may affect STEM’s ability to innovate, which is not good, due to this highly competitive industry. This is especially true when one of its peers, Fluence Energy (NASDAQ:FLNC), has an actually improving R&D expense ratio, as shown in the image below.

FLNC: Rising R&D Expense Ratio (Source: Data from Seeking Alpha. Prepared by InvestOhTrader)

Although it is not yet clear if STEM is being complacent, especially with its current leadership in solar and storage monitoring and control, I believe this uncertainty ignites its current profitability issue.

Positive Bottomline?

One of the most interesting catalysts for STEM this quarter is its positive trailing bottom line amounting to $27.1 million. However, looking at its Q2 2022 performance, although there is an improvement, it is still in negative territory, amounting to -$32 million, a bit better compared to its -$100.2 million recorded in the same quarter last year. This trailing figure accounted for a non-recurring figure in its Q3 2021, where the company reported a positive bottom line of $115.6 million. This positive bottom line is a fruit of their simplification of the capital structure, as quoted below.

On August 20th, we announced the redemption of all 12.8 million public warrants outstanding. Holders exercised 12.6 million warrants at a purchase price of $11.50, which generated gross proceeds of $145 million for the Company. The remaining 147,000 warrants were redeemed for 1 penny each. And as of September 21, there are no more trading warrants in the balance sheet. Source: Q3 2021 Earnings Call Transcript

I believe that with the current guidance of declining adjusted EBITDA, which is expected to be around -$60 and -$20 million this FY22, down compared to the -$30.3 million recorded in FY21 and -$25.44 million, it challenges the idea that STEM is near profitability. In fact, analysts projected an earnings per share of -$0.70 in FY22, -$0.37 in FY23, and -$0.22 in FY24 before it reached a positive $0.21 in FY25.

However, It Is Still Possible

STEM is currently making its move in the EV changing industry and actually closed a deal with a Fortune 50 customer, as quoted below.

We closed a multimillion-dollar EV charging deal with a Fortune 50 customer this quarter. This is our newest behind the meter offering. With strong margins, it is highly differentiated as we can provide our customer a single solution for solar monitoring, energy storage and our Athena platform to monetize all available value streams in their specific market. We are seeing solid momentum in this area and have multiple EV deals in the works. Source: Q2 2022 Earnings Call Transcript

On top of this, it has outstanding growth in its backlog of $726.6 million this quarter, up from $249.7 million recorded in Q1 2021, a 191% YoY growth, up from 156% in Q1 2022 and 144% in Q4 2021. This is quite impressive, especially considering today’s slowing market, but on top of this catalyst, looking at STEM’s pipeline, which is its total value of potential or uncontracted revenue, it has already reached $5.6 billion this quarter, up from $1.7 billion the same period last year. This makes this stock somehow attractive given its potential capabilities.

Still Overvalued Compared to Its Peers

Conservatively, I believe STEM is overvalued as I mentioned earlier and should be avoided for now.

STEM: Relative Valuation (Source: Data from Seeking Alpha. Prepared by InvestOhTrader)

Fluence Energy, Inc. (FLNC), Eos Energy Enterprises, Inc. (EOSE)

STEM is trading at a premium with its P/S ratio of 12.71x compared to its peers’ average of 6.77x. Looking at its forward P/S of 6.66x, which is way above its peer’s average of 2.50x, the same issue will arise when we compare its trailing EV/Sales and forward EV/Sales to the average of its competitors. Considering today’s macro headwinds and an unclear long-term outlook from the management, makes this stock unattractive.

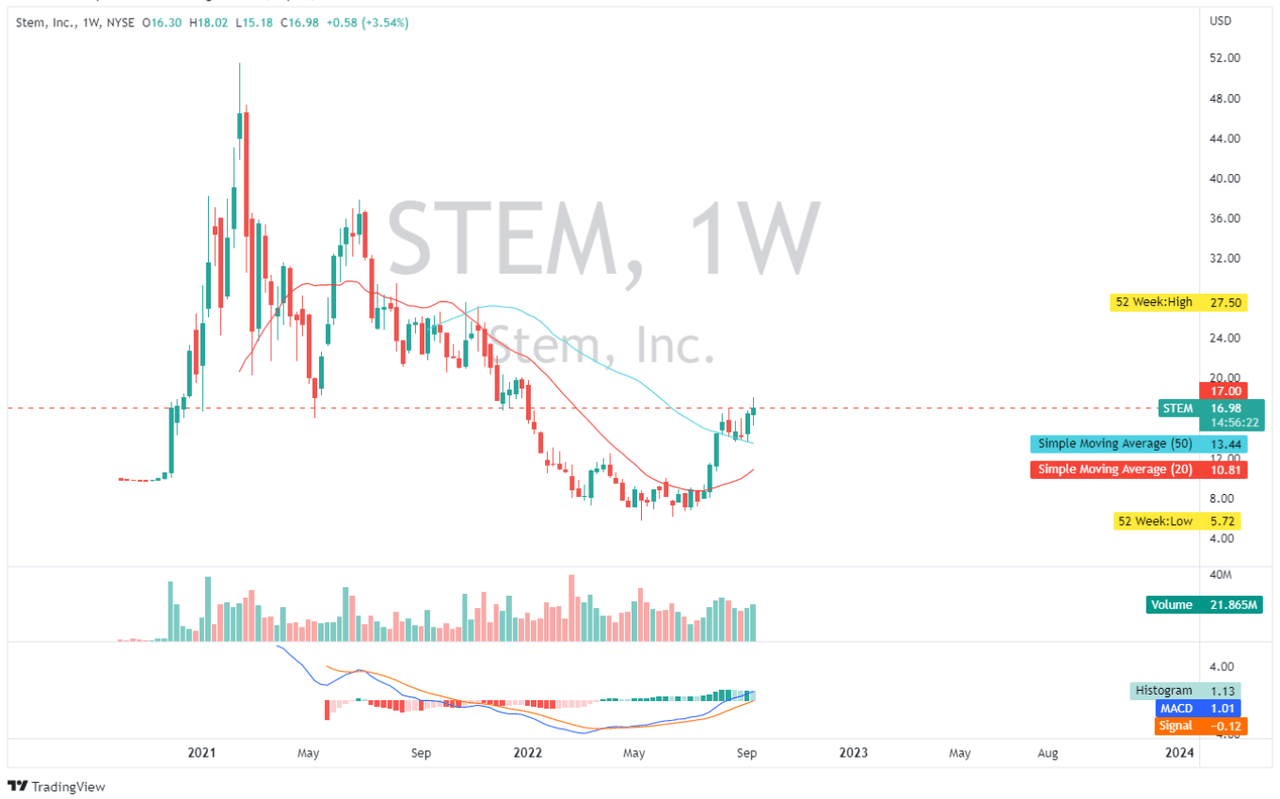

Trading Above Simple Moving Averages

STEM: Weekly Chart (Source: TradingView.com)

Looking at STEM’s weekly chart, the price seems to be struggling at $17, and I believe this is a strong resistance point to consider. However, looking at its simple moving averages indicator, the price pierced both its 20- and 50-day simple moving averages, implying some bullish momentum move. Looking at its MACD indicator, it is still above zero, indicating investor bullishness on the stock. If prices continue to go up, it is okay not to chase, especially if you do not have a base from the low of this year. There is a better option to bet on if you are aiming for a breakout play like FLNC, who is trading at a much lower multiple than STEM.

Conclusion

STEM has a lot of potential, especially with its growing pipeline and with its current leadership, as mentioned earlier. However, looking at the company’s short-term perspective, I believe there is still room for downside. For now, I will be happy to buy STEM at a better price.

Thank you for reading!