Michael M. Santiago

I first became a significant Spotify (NYSE:SPOT) bull when shares have been buying and selling <$100 and promoted a Purchase/ or Sturdy Purchase suggestion ever since (For context, since my final bullish replace in October 2023, shares are up near 58%).

Looking for Alpha

Additionally heading into 2024, and looking out past, I’m tremendous bullish on Spotify inventory. In actual fact, SPOT is my favourite lengthy thought for doubtlessly explosive upside: In my view, Spotify is poised for important progress and elevated profitability in 2024, constructing on sturdy product growth and a concentrate on monetization in addition to effectivity enchancment. My elementary projections recommend a 15-20% YoY improve in MAU, with gross sales progress mirroring this enlargement. Profitability goals embrace a 50 foundation level quarterly improve in gross margin, focusing on a year-end gross revenue margin of round 27%, bringing estimated annual working earnings to $550-600 million and free money circulate to $1.5-2.0 billion, doubtless sparking a doable buyback program as early as Q2 2024. On a extra structural word, the corporate’s potential for consumer base enlargement is appreciable, with alternatives in monetization and diversification into podcasts, audiobooks, and academic streaming. Spotify’s long-term market alternative might attain $170 billion by 2030, with $51 billion in gross sales for Spotify on a 30% market share assumption (Supply: HSBC, analysis word dated twenty seventh March: Spotify: Provoke at purchase: Hitting the fitting notes). Contemplating up to date valuation metrics, most notably a decrease threat requirement for the fairness, in addition to an accelerated EPS progress by way of 2028 on the backdrop of a stable progress outlook, I replace my valuation framework for Spotify; and I now calculate a good implied goal value of $368/share.

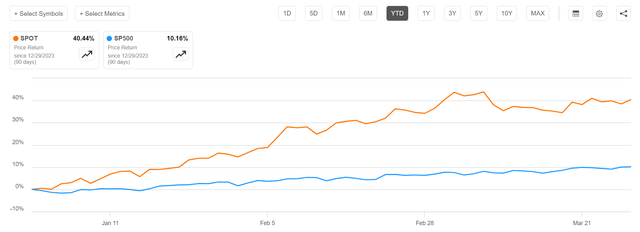

For context, SPOT shares have strongly outperformed the broader bull-market in U.S. shares YTD: Because the begin of the yr, Spotify inventory is up about 40%, in comparison with a acquire of 10% for the S&P 500 (SP500).

Looking for Alpha

FY 2023 Outcomes Level To Doubtlessly Explosive Progress With Engaging Unit Economics

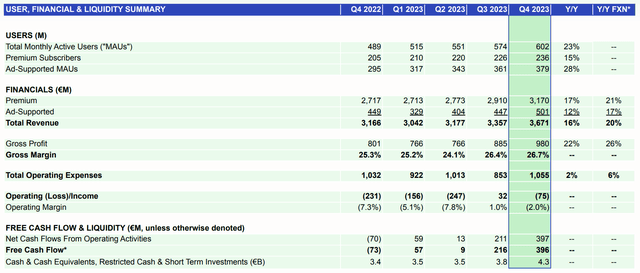

Spotify delivered an exceptionally sturdy This autumn and FY 2023, beating analyst consensus estimates on each topline and earnings: Through the interval from September by way of finish of December, the world’s most distinguished music streaming platform generated $3.67 billion in revenues, which represents a 16% YoY progress charge in comparison with the identical interval one yr earlier. Dissecting the topline by income driver, I level out that 86% was attributable to Premium subscription (up 37% YoY), whereas ad-based gross sales accounted for barely lower than 14% (up 12% YoY).

On profitability, it’s noteworthy to level out that Spotify’s gross revenue in This autumn grew by 22% YoY, to $980 million, outpacing topline enlargement by a powerful 600 foundation factors. In the meantime, working loss narrowed from 231 million in This autumn 2022, to solely $75 million in This autumn 2023. As the primary driver of this revenue inflection, administration cited working jaws and effectivity packages that assist the corporate do ship extra output with much less workers. In that context, the decreased headcount in 2023 vs. 2022 definitely helped scale back the price foundation, with administration having introduced 3 rounds of layoffs by way of 2023, reducing the variety of workers by 17%. On that word, a lot of the effectivity profit ought to be totally materialized solely in 2024, and be sustainable on a long run perspective. Spotify’s free money circulate surged from adverse $73 million in This autumn 2022, to optimistic $396 million in This autumn 2023.

Spotify This autumn 2023 outcomes

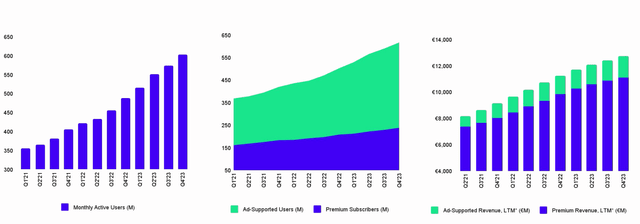

In This autumn, Spotify’s complete consumer base grew at a stable 23% YoY progress and 5% QoQ charge, bringing the full consumer depend to 602 million. Premium subscribers jumped from 205 million in This autumn 2022, to 236 million in This autumn 2023 (15% YoY).

Spotify This autumn 2023 outcomes

For the total yr 2023, Spotify’s topline got here in at $14.6 billion (up 15% YoY in comparison with $12.6 billion in 2022), whereas free working money circulate jumped to $751 million (up 1,500% YoY in comparison with $49 million in 2022). Lastly, I level out that Spotify closed the yr with a really comfy internet money place of $2.4 billion, up from $1.7 billion recorded in 2022.

In 2024, Anticipate Extra Progress, Larger Free Money Stream …

Heading into 2024, Spotify is about for an additional sturdy yr of progress and rising profitability, as CEO Daniel Ek commented within the name with analysts:

So wanting into 2024, you need to anticipate a continuation of what you noticed in 2023, sturdy product growth, which ends up in sturdy progress, however with an elevated concentrate on monetization and effectivity, which in flip drives profitability

In monetary phrases, this could doubtless recommend that Spotify’s MAU base enlargement ought to run at a 15-20% YoY charge, with doubtless an identical progress influence on gross sales. Referring to profitability, Spotify will doubtless purpose for a 50 foundation level uplift in gross margin per quarter, bringing gross revenue margin at yr finish 2024 to ~27%, in accordance with my estimates that are carefully in keeping with consensus as collected by Refinitiv. Additional, extrapolating that Spotify will doubtless run at a 0/+10% working expense base in comparison with FY 2023, I estimate that FY 2024 annual earnings might doubtless fall within the vary of $550-600 million, whereas I mannequin annual free money circulate at $1.5-2.0 billion.

Whereas we now not give full yr steering, we do anticipate wholesome full yr 2024 consumer progress that ought to be near the typical of the previous few years and we anticipate sturdy subscriber progress as properly. Gross Margin and Working Margin are each anticipated to enhance all year long to ship significant full yr enlargement, with podcasting anticipated to ship optimistic Gross Revenue for the yr. We additionally anticipate our Free Money Stream technology to meaningfully exceed what we generated in 2023.

And Doubtlessly Additionally Buybacks

With Spotify’s free money circulate anticipated comfortably above $1 billion in 2024, paired with a $2.4 billion internet money place, I argue the announcement of a buyback program as early as Q2 2024 may very well be doubtless. Buyers ought to think about that Spotify wants little or no money for progress, as evidenced by the corporate’s enormously engaging incremental free money circulate on incremental CAPEX metric. For context, Spotify’s CAPEX/Gross sales ratio is 0.0005, whereas the corporate’s YoY 2024 vs 2023 working expense investments of $50 million generated a gross revenue uplift of $800 million.

Spotify Nonetheless Has Tons Of Progress Forward

On a structural perspective, investor ought to word that there’s nonetheless numerous penetration upside for Spotify. In actual fact, I argue that the demand for music is common. And with Spotify clearly main the streaming commercialization of this common product, the corporate might even see a consumer depend much like different international platforms comparable to Instagram/ Fb, or YouTube, suggesting a MAU potential that might high 3 billion, in probably the most optimistic state of affairs.

Along with the consumer base progress potential, I additionally see an unlimited alternative in monetization: In actual fact, the vast majority of SPOT’s earnings, round 85%, are generated from its premium subscription choices, whereas premium subscribers account for lower than 40% of the corporate’s complete consumer base. The remainder of gross sales, about 15%, comes from promoting revenue by way of its free, limited-access streaming platform.

Lastly, Spotify’s progress is supported by alternatives rising from ventures into podcasting, audiobooks, academic streaming, and the Two-Sided Market. On that word, I spotlight work by HSBC, which estimated that Spotify’s 2030 market alternative might high $170 billion, with $51 billion of gross sales for Spotify on a 30% market share assumption (Supply: HSBC, analysis word dated twenty seventh March: Spotify: Provoke at purchase: Hitting the fitting notes).

HSBC Analysis

Replace Valuation: Elevate Goal Worth to $368/ share

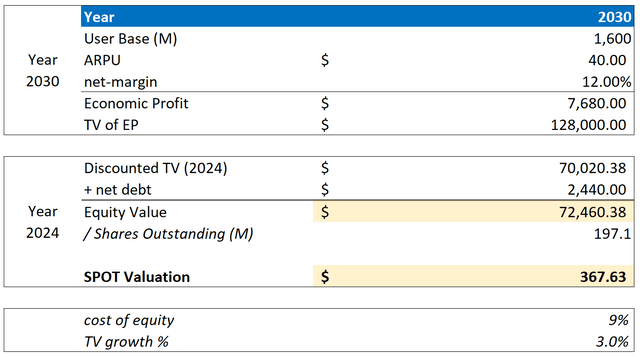

Given the accelerated progress of Spotify and the corporate’s earnings turning round sooner and extra robustly than initially anticipated, I am revising my projections for Spotify. For the yr 2030, I now predict that Spotify will attain a consumer base of 1.6 billion, which might replicate a compound annual progress charge of roughly 15% all through the forecast interval—a charge barely beneath the historic development. On monetization, I imagine a $45-45 ARPU is cheap, which might roughly be equal to the weighted ARPU that Netflix is seeing in its international subscriber base, as of 2024 (I argue Netflix in 2024 is way forward of the monetization vs. Spotify, as evidenced by the corporate’s value will increase, crackdowns on password sharing and class in subscription tier. In my base case thesis, Spotify’s monetization would catch as much as Netflix’ over the subsequent 7 years). Constructing on comparable working economics seen in Netflix, I am projecting a 12% internet revenue margin. Furthermore, whereas I preserve a terminal progress charge assumption at 3%, which is roughly 75-100 foundation factors forward of nominal GDP progress, decrease my value of fairness requirement by as a lot as 200 foundation factors, principally as a mirrored image of a extra accommodating rate of interest atmosphere on macro degree, but additionally as a mirrored image of a maturing, and thus much less dangerous, business outlook for Spotify particularly. Primarily based on these revised assumptions, I now calculate that Spotify will generate a $7.7 billion annuity by 2030, which has a gift worth value of $128 billion. When this determine is discounted again to early 2024 at a 9% charge and mixed with $2.4 billion in internet money, the calculation yields an fairness worth of $72.4 billion, or $368 per share.

Firm Financials; Creator’s EPS Estimates; Creator’s Calculation

Beneath additionally the up to date sensitivity desk (columns = MAU; rows = ARPU)

Firm Financials; Creator’s EPS Estimates; Creator’s Calculation

Dangers

Referring to threat, I wish to level out what I’ve beforehand written — in my opinion, no main threat occasion has been notable since (September 2023):

Competitors vs huge tech firms is the primary threat I see for Spotify: Notably, Apple (AAPL), Amazon (AMZN) and Google (GOOG) are competing for a share within the music streaming industries – and these gamers aren’t “good” opponents to have. Particularly, and along with the competitors for customers, competitors from pocket-rich gamers comparable to Apple and Google has the potential to drive elevated content material acquisition prices, as streaming distributors attempt to safe unique music rights to stay aggressive. Moreover, Spotify could face challenges in diversifying its income streams past subscriptions, as in comparison with Apple and YouTube, which produce other worthwhile companies supporting their music and video choices. Whereas Spotify appears just like the winner in music streaming at the moment (for me), traders ought to watch aggressive dynamics “like a hawk”.

Investor Takeaway

Heading into 2024, my outlook on Spotify is extraordinarily bullish, marking it as my high suggestion for doubtlessly explosive share value upside: In my opinion, Spotify’s optimistic progress trajectory is firmly anchored in strong product growth, enhanced monetization, and improved effectivity. On a extra structural word, I spotlight the potential for consumer progress and income diversification that might indicate $51 billion of gross sales by 2030. Contemplating up to date valuation metrics for Spotify, I now calculate a good implied goal value of $368/share.

{kind=link}