S&P 500, Dow, Volatility, Greenback, Yields, Inflation and Recession Speaking Factors:

- The Market Perspective: S&P 500 Bearish Beneath 3,800; USDCNH Bearish Beneath 7.0000

- The primary week of the yr registered a 1.5 p.c achieve for the S&P 500 and -3.0 p.c drop from the VIX, lining as much as seasonal norms

- Whereas the market’s sidled increased with a backdrop of tempered fee expectations, there’s important distinction in recession dangers and danger from extraordinarily complacent circumstances

Really useful by John Kicklighter

Get Your Free High Buying and selling Alternatives Forecast

Seasonal norms received out this previous week, which is unimaginable contemplating the specter of an impending recession grew significantly extra tangible and market complacency has pushed to blatantly excessive ranges. Trying again on the efficiency of the varied benchmark danger belongings that I monitor for a worldwide perspective, it was clear that the bid wasn’t siloed to particular asset or areas. International indices, rising markets, excessive yield fastened earnings, carry commerce and a few speculative-oriented commodities posted notable good points. In some instances, the bullish curiosity comes with the technical context of a restoration from considerably depressed ranges – just like the Nasdaq 100 which is just 5 p.c away from tipping into new multi-year lows. For such markets, nuanced adjustments in key themes can foster a rebound that may subsist as a counter-trend ‘bounce’ with out spurring the dedication needed for a long-term bull development. Then again, we now have sure measures that flagrantly defy conventional fundamentals and can draw a lot better scrutiny – as with the UK’s FTSE 100 at multi-year highs and inside simple attain of information.

Focusing in on my most popular ‘imperfect’ benchmark for danger, the S&P 500, there was a nascent cost that doesn’t elevate the specter of a definitive development. The index lastly managed to filter an exceptionally slim 13-day buying and selling vary that was the maintain over of vacation circumstances. The break might also be at the very least be a partial by-product of these seasonal circumstances as nicely. Breaking down the S&P 500’s common weekly efficiency over the calendar yr, the primary week has averaged the strongest general achieve of all the 52-week interval again to 1900. A 1.0 p.c averaged achieve isn’t far off the 1.5 p.c advance that was largely earned on Friday’s session. Whether or not this was extra a real break (one I’d contemplate backed by ‘conviction’) or capital flows related to reinvesting capital to start out the yr might be put to the take a look at within the week forward. We broke the slim, close to three week vary, however the midpoint of the August – October vary and vary low from November eleventh to December 14th at 3,910 remains to be overhead.

| Change in | Longs | Shorts | OI |

| Day by day | -14% | 15% | -3% |

| Weekly | -8% | 7% | -1% |

Chart of the S&P 500 with Quantity and 100-Day SMA (Day by day)

Chart Created on Tradingview Platform

The market’s subsequent leg – in sentiment as a lot because the US indices – will draw more and more in the marketplace’s elementary convictions because the tide in liquidity ranges out. The tempo for which we anchor again into predictable themes relies on circumstances, however I wish to additionally consider markets in accordance with potential. There’s a risk that speculative markets resolve to the bulls to proceed the restoration from 2022’s broader losses as a lot as there’s a likelihood that the bears regain management over the yoke because the systemic themes proceed to color a unfavorable image. The end result relies on the trail of key occasions in addition to the prioritization of the lots. That mentioned, I imagine there to be a skew within the ‘potential’ of the completely different outcomes. Ought to bullish pursuits (say within the S&P 500) win out, it’s extra prone to be primarily based in nuance similar to a ‘gentle recession’ or ‘barely decrease oppressive rates of interest’. That might doubtless result in slower and choppier good points, particularly with the market’s sense of implied danger so low. Conversely, an eruption of concern may amplify a market that’s poorly positioned to soak up the bears. Think about the VVIX ‘Volatility of Volatility’ Index. It dove to its lowest degree since March 2017. I’d say that’s remarkably complacent.

Chart of the VVIX Volatility of Volatility Index Overlaid with the VIX (Weekly)

Chart Created on Tradingview Platform

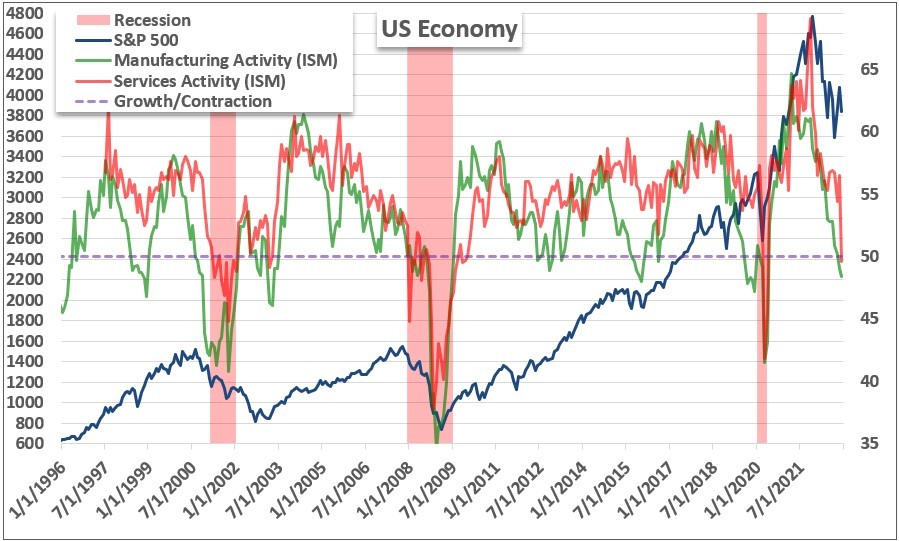

A giant consideration for what form the markets take within the week and weeks forward is what the highest elementary focus shakes out to be. This previous week, we had been offered the distinctive alternative to check two of the main issues on the macro spectrum: fee hypothesis versus development forecasting. The Friday morning US nonfarm payrolls appeared to provide a light-weight push in favor of Fed prognostication when the 226,000 web improve modestly beat expectations, dampening financial considerations; whereas the common hourly earnings development decelerated to 4.6 p.c year-over-year to modestly ease terminal fee projections. Maybe if it weren’t for the NFPs, the response to the ISM service sector exercise report may have been very completely different. Representing a well timed have a look at the most important element of financial exercise and employment within the US, the ISM studying dropped 6.9 factors and into ‘contractionary’ territory. Such an occasion strains up very nicely to previous recessions, however that didn’t appear to hit the market’s radar. With a perspective that Fed expectations had been already easing, this might amplify the transfer. However are barely decrease Fed charges actually a better boon for markets than a recession is a risk?

Chart of ISM Service and Manufacturing Surveys, S&P 500 and US Recessions (Month-to-month)

Chart Created by John Kicklighter

For one thing just like the US Greenback, the push and pull of an rates of interest versus development query isn’t as urgent. It could actually reply to each themes in its function because the world’s most liquid forex – and the various guises it dons provided that place. Contemplating the Fed Fund futures implied June dropped to 4.95 p.c with US 2-year yields posting their greatest single-day slide since November tenth’s CPI launch, the implications for the Dollar as a latest carry benefactor had been simple. This forex is extra delicate to the particulars of Fed yield curve forecasting as long as the extra systemic issues of worldwide sentiment don’t crowd out our senses. Ought to danger aversion sit back in, the bid for a secure haven just like the Greenback will begin to battle with a probable additional slide in fee projections. The extra intense a sentiment swoon, the scales will tip for the USD to behave as a liquidity supplier of final resort. It could take fairly the dive to escalate our fears to that scale, however it’s actually throughout the eventualities we may face forward as liquidity is topped off.

Chart of the DXY Greenback Index with 200-Day SMA Overlaid with US 2-Yr Yield (Day by day)

Chart Created on Tradingview Platform

Finally, the US doesn’t have the lock up on dictating international sentiment. Then once more, its scale does give it better sway when its personal circumstances are creating considerably. What’s extra, the financial calendar for the approaching week appears to be disproportionately weighted in the direction of US affect. For rate of interest hypothesis, we now have the market’s favourite inflation indicator, the CPI, due for launch on Thursday. Fed Chairman Powell may also be talking on Tuesday, however his feedback may simply as readily spill into an financial evaluation contemplating how often he has talked about that facet of the coin of late. Friday’s financial institution earnings and College of Michigan client sentiment report, although, are more likely to start out with a development perspective.

High Macro Financial Occasion Danger Subsequent Week

Calendar Created by John Kicklighter

Uncover what sort of foreign exchange dealer you’re

{kind=link}