Michael Vi

Funding thesis

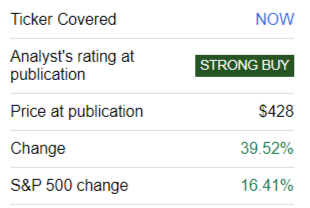

I lined ServiceNow (NYSE:NOW) for the primary time in early March, and my name aged properly. The inventory delivered a large, virtually 40% rally, considerably higher than the broad market’s efficiency.

In search of Alpha

In the present day I need to reiterate my “Sturdy Purchase” ranking. The corporate’s efficiency is stellar, particularly contemplating the present difficult setting. Income continues to develop at double digits, and profitability metrics are increasing. Each near-term and long-term consensus estimates are optimistic, and the inventory nonetheless seems undervalued even after a large rally. I like the corporate’s latest energetic initiatives together with promising partnerships with IT giants within the area of synthetic intelligence [AI]. Nevertheless, given a strong year-to-date rally, a near-term correction to the general inventory market is feasible. Due to this fact, traders contemplating investing in NOW needs to be able to tolerate short-term volatility.

Current developments

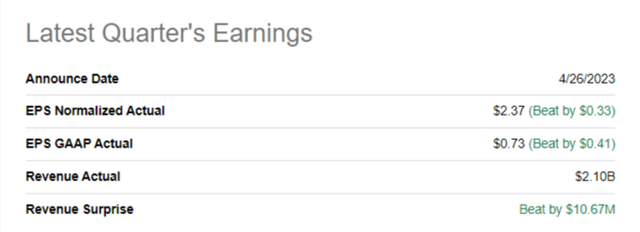

The corporate introduced its newest quarterly earnings on April 26, beating consensus estimates. Income demonstrated strong momentum with a 22% YoY progress and the adjusted EPS expanded considerably from $1.73 to $2.37.

In search of Alpha

The power in income momentum allowed NOW to broaden profitability metrics. There may be little room to enhance for the gross margin near 80%, however the firm did broaden the metric barely. What’s extra vital is that the working margin expanded from 5% to virtually 7%, with the SG&A to income ratio declining by virtually one proportion level. R&D investments are nonetheless substantial and near 25%. I like that the corporate continues to speculate closely in constructing sustainable aggressive benefits. Given the stellar monitor file of income progress and margin enlargement, I’ve excessive conviction that the administration and engineers will probably be environment friendly of their R&D actions.

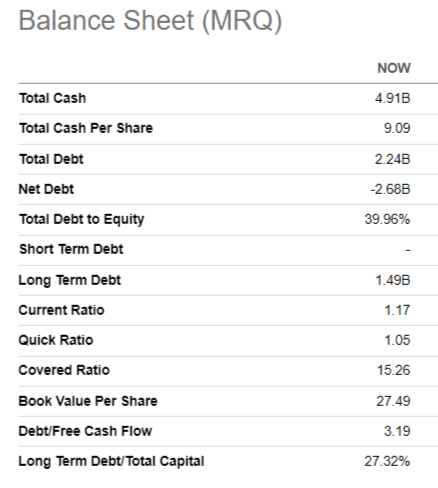

The stability sheet continues to be a fortress with virtually $5 billion in money, which is greater than twice increased than the excellent debt quantity. The lined ratio could be very comfy at about 15, and liquidity metrics are additionally in good condition.

In search of Alpha

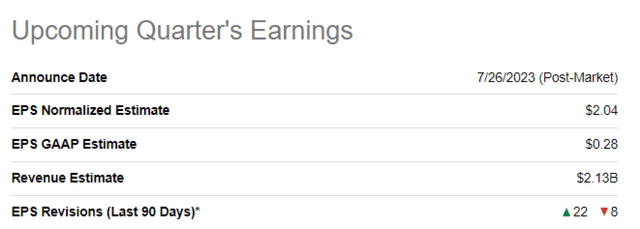

The upcoming quarter’s earnings launch is shut, scheduled on July 26. The general sentiment over the upcoming announcement is optimistic, with 22 upward revisions from Wall Avenue analysts over the past 90 days. Income is projected by consensus to stay above 20% YoY progress, which is spectacular. The adjusted EPS is anticipated to comply with the highest line by increasing from $1.62 to $2.04, which if achieved will probably outpace the income progress.

In search of Alpha

I believe that so long as the corporate continues to reinvest a considerable portion of its gross sales in innovation, NOW will be capable to maintain double-digit income progress. The corporate’s stellar income progress tempo didn’t deteriorate a lot amid the cruel macro setting, which has existed because the starting of 2022. That is so as a result of NOW’s choices are aimed toward making shoppers’ IT techniques extra streamlined and environment friendly, which reduces the overall price of possession. That stated, shoppers aiming for price optimizations are poised to implement options like NOW presents, particularly within the present risky setting. I count on the corporate to proceed to exhibit this resilience amid the unsure setting the place many enterprises are slicing again on prices, together with IT spending.

The evident secular power for ServiceNow is prone to come from the AI alternatives. The corporate is taking strong steps in including AI-related options to its merchandise. Final month, ServiceNow launched its Now Help digital agent, a chatbot with generative AI capabilities. I’m additionally very optimistic relating to the corporate’s actions in increasing its AI-related partnerships with giants like Microsoft (MSFT) and NVIDIA (NVDA) to enhance its product. In the mean time, it’s troublesome to evaluate the impact of those partnerships and new options on the corporate’s earnings. However I’ve excessive conviction that the impact on the corporate’s long-term earnings estimates will probably be notable. I imagine generative AI options will allow ServiceNow to considerably enhance the worth of its platforms for purchasers. It might be truthful for NOW to cost elevated charges or create new alternatives to cross-sell or upsell, in my opinion. I believe that throughout the upcoming earnings name, the administration is very prone to improve its steerage and share its imaginative and prescient of how new AI options will create extra worth for shareholders over the long run. That’s the reason I’m very optimistic concerning the upcoming earnings.

Valuation replace

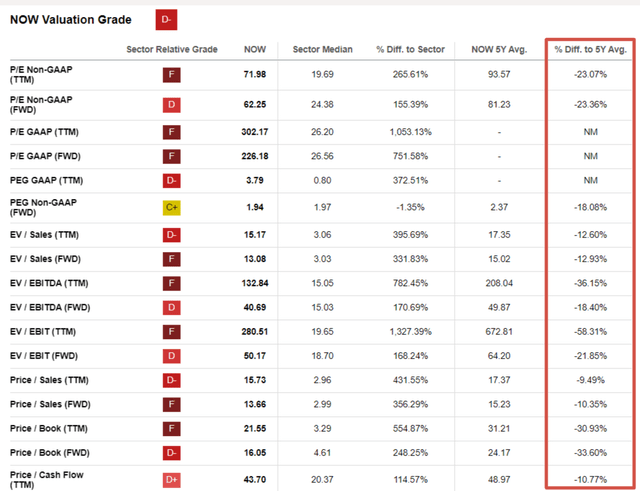

The inventory delivered a large 55% rally year-to-date, considerably outperforming the broad market. NOW has a poor “D-” ranking from In search of Alpha Quant on account of excessive valuation ratios in comparison with the sector median. Then again, the present multiples are nonetheless considerably decrease than historic averages. That stated, the inventory would possibly nonetheless be undervalued.

In search of Alpha

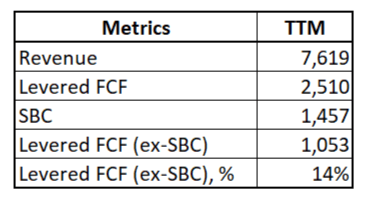

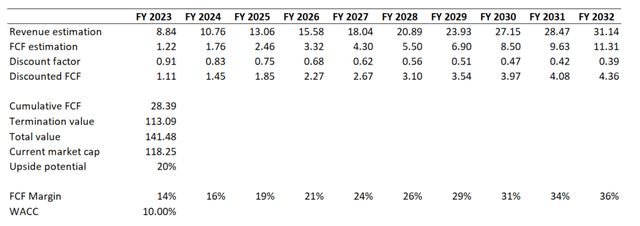

I’ll proceed with the discounted money circulate [DCF] method to get extra proof. I exploit the identical 10% low cost price as I did in March. Earnings consensus estimates have been up to date because the newest earnings launch, so I additionally incorporate it into my DCF. The highest line is projected to develop at a 15% CAGR. The stock-based compensation [SBC] is a considerable a part of income, almost 20%. Due to this fact, this time I wish to simulate a extra conservative situation with the FCF margin ex-SBC. I count on the FCF margin to broaden by 250 foundation factors yearly.

Writer’s calculations

Even underneath considerably extra conservative assumptions associated to the FCF margin, the inventory nonetheless seems attractively valued with a 20% upside potential.

Writer’s calculations

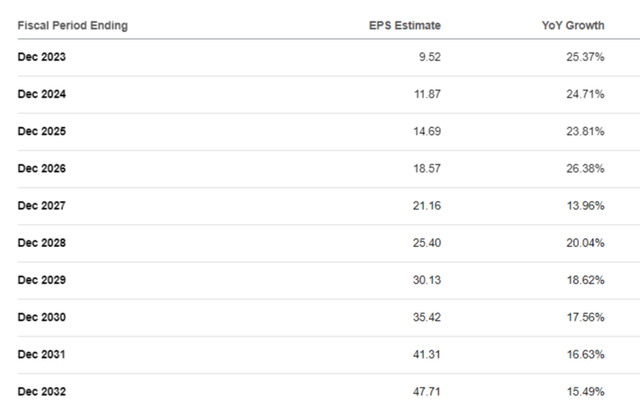

Some pessimists would possibly argue that the annual 250 foundation factors FCF margin enlargement is approach too optimistic. However, I believe it’s truthful given the consensus projections of the adjusted EPS progress over the subsequent decade.

In search of Alpha

Dangers replace

ServiceNow is a progress firm with a difficult income progress profile priced into the share worth. As we have now seen above, the EPS enlargement expectations are additionally excessive. Due to this fact, the corporate has virtually no room for errors if it needs to again up its market capitalization with underlying fundamentals sooner or later. Any earnings miss or steerage downgrade would possibly result in traders’ disappointment and big sell-offs. Even when challenges for the corporate are non permanent and never secular, traders nonetheless can turn out to be disenchanted quickly. It’ll take a number of quarters for the corporate to regain traders’ confidence within the firm’s brilliant future and secular potential.

Being a expertise firm providing cutting-edge options, there’s all the time a excessive degree of uncertainty relating to the merchandise’ life-cycle size. The corporate needs to be able to innovate so as to not be disrupted continually. I take into account this danger distant as a result of the corporate invests a few quarter of its complete gross sales in R&D. What is significant for the corporate is to maintain its high-efficiency of R&D efforts. It’s also vital to say that even if the danger is distant, its adverse impression is very prone to be huge.

The general inventory market, particularly the Expertise sector, seems barely overheated after a large year-to-date rally. CNN’s Concern and Greed Index has been in an “Excessive Greed” zone for a very long time. I believe {that a} market correction is very probably within the close to time period, and the sell-off would possibly have an effect on even high-quality and undervalued names like NOW. That stated, traders needs to be able to tolerate short-term volatility in the event that they determine to speculate at these ranges.

Backside line

To conclude, ServiceNow inventory continues to be a “Sturdy Purchase”. Income progress momentum is huge. I like that profitability metrics are nonetheless on their enchancment path, even within the present difficult and high-inflationary setting, which was nonetheless there in Q1 of 2023. The administration continues to construct a large “moat” by reinvesting a few quarter of the overall gross sales in R&D. Final however not least, valuation seems very enticing even given the strong year-to-date rally.

Editor’s Word: This text was submitted as a part of In search of Alpha’s Finest AI Concepts funding competitors, which runs by means of August 15. With money prizes, this competitors — open to all contributors — is one you don’t need to miss. If you’re focused on turning into a contributor and collaborating within the competitors, click on right here to seek out out extra and submit your article as we speak!

{kind=link}