Leon Neal/Getty Photographs Information

We beforehand coated Rivian Automotive (NASDAQ:RIVN) in November 2023, discussing the promising improvement surrounding its manufacturing/ supply numbers and bettering gross margins over the previous few quarters.

Mixed with the raised FY2023 manufacturing steerage and strong ASPs, we had rated the inventory as a speculative Purchase, with it prone to emerge as one of many potential winners within the start-up EV business.

On this article, we will focus on why we keep our Purchase ranking, attributed to the engaging danger/ reward ratio from the misunderstanding surrounding RIVN’s supposed supply miss in FQ4’23.

With the PPI within the Automotive sector already peaking and borrowing prices prone to average because the Fed pivots, we consider that its high line growth might outperform expectations, as extra TSLA drivers think about the R1S and R1T to be different EV fashions.

The Close to-Time period EV Funding Thesis Seems To Be Blended

Whereas RIVN has but to report FQ4’23 earnings, it seems that the market has determined to low cost its prospects first, attributed the supposed supply miss within the quarter.

For context, the automaker produced 17.54K automobiles (+7.6% QoQ/ +75% YoY) whereas delivering 13.97K automobiles (-10.2% QoQ/ +73.5% YoY), implying a widening ratio of 79.6% (-15.8 factors QoQ/ -0.7 YoY).

Nevertheless, readers should additionally word that the RIVN administration has already warned of this occasion within the FQ3’23 earnings name, with Amazon (AMZN) anticipated to “restrict consumption of latest business vans throughout its peak vacation supply interval, leading to a big hole between manufacturing and deliveries in This autumn relative to prior intervals.”

Consequently, it seems that the market has not been paying consideration, for the reason that automaker has already produced a formidable sum of 57.23K automobiles (+135.2% YoY) and delivered 50.12K automobiles in FY2023 (+146.5% YoY), with a narrowing ratio of 87.5% (+4 factors YoY).

These numbers simply exceed the administration’s unique FQ4’22 manufacturing steerage of 50K automobiles, FQ2’23 steerage of 52K automobiles, and FQ3’23 steerage of 54K models certainly.

With RIVN nonetheless sustaining a formidable double digit manufacturing/ supply progress charges, it seems that demand for its EV choices stay wonderful, versus the problems confronted by a number of legacy automakers, akin to Common Motors (GM) and Ford (F), prompting their subsequent moderation in EV ambitions/ capex.

Nonetheless, these developments might pose near-term uncertainties to RIVN’s prospects certainly, relying on how readers interpret them.

On the one hand, F has dedicated to lowering its FY2024 F-150 Lightning manufacturing from the deliberate capability of three.2K automobiles to 1.6K automobiles every week, following the completion of the EV early adopter wave and pending the introduction of mass-market (ie: cheaper) fashions in 2025/ 2026.

On the similar time, GM has additionally confirmed that “the tempo of EV progress has slowed,” regardless of the supposed “100K reservations and orders for EV pickups by means of 2025.” The uncertainty has already triggered the administration’s lowered 2024 capex steerage to $11B, in comparison with the unique top-end steerage of as much as $13B by means of 2025.

To place the ultimate nail down, we consider that Tesla (TSLA) solely managed to report double digit FQ4’23 manufacturing and supply progress due to the drastic worth cuts, with the fee reductions/ efficiencies already “approaching the bounds inside its present platforms.”

The identical has been noticed within the peaking Producer Value Index for Car, Mild Truck, and Utility Car Manufacturing at 169.361x by November 2023.

Whereas the index has moderated to 168.432x by December 2023, there stays a fantastic distance to the 155.1x reported in 2019, implying that RIVN’s constructive gross margin goal by the tip of 2024 could also be an underwhelming determine certainly.

Due to this fact, whereas the worst might very nicely be behind us, permitting start-up automakers, akin to RIVN, to enhance their price foundation as they ramp up in manufacturing quantity, readers should additionally mood their near-term expectations because the reversal is not going to happen over evening.

However, assuming that RIVN is ready to maintain the strong shopper demand, we might even see its EV market share speed up from present ranges, as extra TSLA drivers think about the previous’s R1S and R1T to be different manufacturers with 34.1% in recognition ranking (double of the F-150 Lightning).

Whereas it stays to be seen how issues might progress for RIVN, we consider that its near-term prospects could also be briefly impacted by the continuing EV uncertainties.

That is till the automaker releases mass market fashions ranging from $40K on the R2 platform in 2026, as borrowing prices for brand spanking new automobiles average from the 7.1% reported in December 2023, in comparison with the normalized 5.4% in December 2019.

Solely time might inform.

So, Is RIVN Inventory A Purchase, Promote, or Maintain?

RIVN Valuations

Searching for Alpha

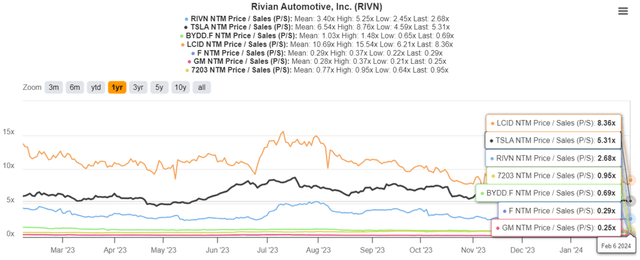

For now, RIVN continues to commerce at premium FWD Value/ Gross sales valuations of two.68x, whereas moderated from its 1Y imply of three.40x, nonetheless elevated in comparison with the automotive sector median of 0.90x.

On the similar time, we consider that a part of the premium is warranted, with RIVN’s valuations showing to be the most affordable amongst all start-up EV friends.

The Consensus Ahead Estimates

Searching for Alpha

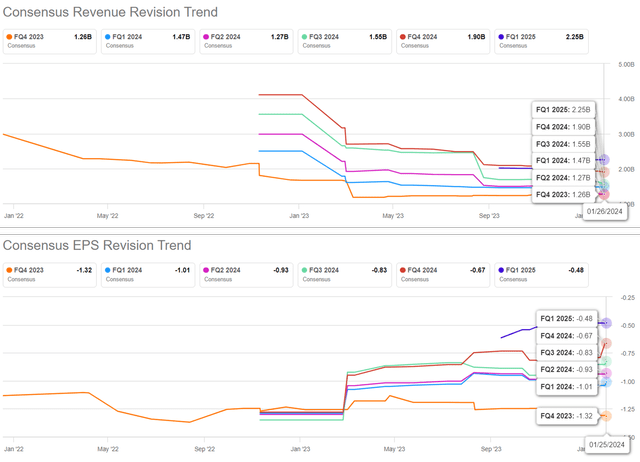

With a persistently raised EPS ahead estimates regardless of the moderating top-line estimates, additionally it is obvious that the consensus believes that RIVN could possibly file bettering gross margins shifting ahead, naturally decelerating its money burn charge forward.

RIVN 1Y Inventory Value

Buying and selling View

Whereas the RIVN inventory might have fallen in sympathy to the uncertainties surrounding EV demand, with the 2 leaders, TSLA and BYD Firm Restricted (OTCPK:BYDDF) additionally charting decrease highs and decrease lows YTD, we’re not overly involved.

After opening up their business van orderbook from November 2023 onwards, RIVN has additionally inked new offers with AT&T (T), with extra prone to come after costs turns into extra engaging as lithium spot costs/ battery costs average and EV parity is achieved by 2026.

With the optics briefly skewed towards pessimism, attributed to the hole between its manufacturing and deliveries in FQ4’23, we consider that these depressed ranges provide traders with the opportunistic probability to greenback price common accordingly.

Assuming that RIVN is ready to maintain its premium FWD Value/ Gross sales valuation of two.68x, we may see a wonderful upside potential of +162.5% to our long-term worth goal of $40.70, based mostly on the consensus FY2026 income projection of $15.19B.

On account of the engaging danger/ reward ratio, we keep our Purchase ranking on the RIVN inventory.

{kind=link}