Povozniuk/iStock by way of Getty Photos

Quantum-Si Inc. (NASDAQ:QSI) launched its Q2 2023 earnings report on Monday, August 7th, and the market didn’t take it effectively.

Q2 income fell effectively under expectations at $200K v $400K, and ahead steering was decreased. A key product was shelved, and issues with the AI software program had been itemized. Consequently, the share worth dropped precipitously (down 30% on the day), and continued to fall on Tuesday.

I’ll clarify why I consider the market is overreacting to the replace and why I’m searching for a turning level to purchase QSI.

Within the FY2022 report, QSI itemized three key aims for 2023

Our first precedence is to commercialize Platinum, Carbon and the 2M chip.

The Carbon product is not a precedence; administration implied it has been shelved for now. Efforts to promote the Platinum (which makes use of the 2M chip) are growing with a brand new gross sales staff and improved gross sales administration.

Our second precedence is to steer with innovation.

QSI stays the market chief on this space, first to market, and at present the one protein sequencing software obtainable. A latest peer-reviewed in Nature was the primary printed by any firm making an attempt to commercialize protein sequencing.

Our third precedence is to protect monetary power.

The flawless steadiness sheet, decreased bills throughout Q2, and the deal with commercialization impressively keep the steadiness sheet and protect the money runway.

QSI has a first-mover benefit in an enormous market with an unmet want for a dependable, low-cost protein sequencing machine. The QSI product made its first gross sales in Q1 2023, and if QSI can work to resolve points and suggestions, it may rapidly scale into an enormously worthwhile enterprise.

The significance of Proteins

Proteins are a folded string of amino acids and symbolize many of the molecules in our physique (after water). Proteins are accountable for nearly each organic perform in our physique; in contrast to the genome, the proteome is in fixed flux. Proteins perform as antibodies, hormones, and enzymes. The entire set of proteins is named the proteome.

The knowledge in cells begins with DNA encoding, resulting in round 20,000 genes often known as the genome. Greater than 90% of the genome is transcribed into RNA, producing greater than 100,000 transcriptions that mix to make greater than 1 million proteins. Nearly all of variation inside dwelling cells is within the proteome.

Lately the genome has been sequenced and decoded, giving a larger understanding of the genes and the data they carry. Genomics has allowed genetic variation investigation and led to new medication and medical advances. To this point, the identical just isn’t true for proteomics; sequencing proteins has confirmed technically difficult and costly.

The proteome is crucial in most cancers analysis and has been used to detect the presence of various kinds of most cancers. Biomarkers (a measurable indicator of a medical state) have been discovered utilizing mass spectrometry. Mass Spectrometry is at present the usual technique to check the proteome. In Might 2014, a draft map of the human protein was printed in Nature that was derived utilizing mass spectrometry.

The advanced nature of the proteome has held again analysis that requires the sensitivity of study obtainable with DNA sequencing methods. A cell can have greater than 10,000 proteins and Mass spectrometry requires excessive protein ranges to detect it. Aberrant proteins can exist in tiny portions which might be undetectable by mass spectrometry. A single molecule-based sequencing technique can doubtlessly revolutionize protein science and medication.

QSI’s mission is exactly that, and the purpose is usually repeated in earnings calls

to carry next-generation sequencing to each lab, in every single place

There may be at present no excessive throughput expertise (an automatic tech) to research single proteins. QSI is creating a desktop unit that may discover a protein, work out the sequence of amino acids it accommodates, and use AI to output related data to the analysis science group.

The Whole Addressable Market

Markets and Markets printed a analysis paper in Might 2023 estimating the dimensions of the Proteomics market to be $32.4 billion in 2022 and with a 14.6% CAGR $72.9 billion by 2028. The paper focuses on the usage of mass spectrometry-based imaging to develop an understanding of the proteome, and it quotes the excessive price of devices and applied sciences as being the principle brake on the expansion of the market itself, resulting in restricted adoption in areas that will result in novel drug improvement, vaccines, and diagnostic instruments.

QSI’s product, with a price ticket of $70,000, is considerably lower than the $1 million at present required for Mass Spectrometry

Quantum Sci Method

The long-term purpose of QSI is to develop a machine that may sequence all proteins and establish errors within the sequencing code.

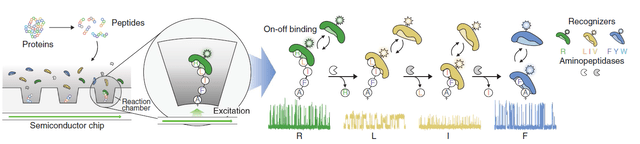

QSI has developed a desktop machine based mostly round a silicon chip of their design. The M2 chip is the principle part of the gadget and accommodates a lot of its IP.

Simplifying the method, it goes like this

- The pattern is loaded into the gadget.

- Proteins are break up into peptides (quick strings of amino acids).

- The peptides fall into thousands and thousands of response chambers on the M2 silicon chip.

- A mix of chemical recognizers is added to the response chambers, binding to sure Amino Acid strings.

- Lasers are fired on the luminescent recognizers, and light-weight measurements are taken.

- The software program makes use of gentle measurements to find out the character of the protein.

Recognizers

The event of the recognizers is a key a part of the IP; they’re short-lived fluorescent molecules that bind to specific sequences of amino acids and single molecules, the silicon chip measures the fluorescence in a number of methods and the data results in an intensive understanding of which protein is current.

QSI Technique (QSI web site)

The event of the receptors and the software program’s potential to find out what’s current based mostly on the fluorescence is essential; when the Nature article was printed (October 2022), it mentioned

Recognizers for brand spanking new amino acids or PTMs might be advanced from present recognizers or recognized in screens of different scaffolds, resembling different sorts of NAA- or PTM-binding proteins or aptamers. Extension to detection of all 20 pure amino acids and a number of PTMs is possible for de novo sequencing; nonetheless, partial sequences are adequate for many proteomics purposes, which depend on mapping to predefined units of candidate proteins

(Supply: The Nature article white paper)

The white paper is the one peer-reviewed article printed by any firm investigating this expertise (QSI earnings name FY 2022).

This fall 2022 earnings name expanded on the present state of the recognizers

accelerated our product improvement efforts and efficiently demonstrated the flexibility to acknowledge 15 out of the 20 amino acids. This represents a path to greater than 70% protection of the Human Proteome identification of as much as 90% of proteins,

(QSI: Earnings name This fall 2022 Transcript, 2023-3-6)

Presently, QSI can detect 75% of amino acids and the software program can use that recognition to establish 90% of the human proteome. It represents a major advance on what is accessible out there.

The M2 Sequencing chip

The semiconductor is the center of the expertise and is produced in an ordinary fab. The chip, designed to research thousands and thousands of chambers in parallel, one molecule at a time, controls the laser and the sensors that detect emitted photons. It’s unattainable to amplify proteins, so the chip’s single-molecule sensitivity is essential.

In November 2021, QSI acquired Majelac Applied sciences LLC (1022 FY 10K), a semiconductor packaging firm in Pennsylvania. The chip is a consumable on this gadget and might be part of future consumable gross sales together with the recognizers.

They’re the primary firm (I may discover) that has efficiently enabled NGPS (next-generation protein sequencing), permitting for the identification of proteins that may unlock new analysis areas in a few of the most essential medical fields, together with most cancers and immunology.

The individuals

These small disruptive tech corporations all have a compelling story, a terrific concept that may serve a big market. For my part, the story just isn’t sufficient to speculate, the science is one factor, however the potential to commercialize that concept is kind of one other. In my buying and selling plan, industrial income is a vital differentiator. As soon as an organization has precise gross sales, I take into account its expertise validated, giving it a considerably increased likelihood of success.

In QSI’s case, industrial validation arrived in Q1 2023 with a small variety of gross sales of its Platinum gadget (3 items, I estimate). These items had been all positioned with educational analysis establishments representing probably the most vital a part of the QSI gross sales funnel. The small variety of items and the character of the purchasers has me classifying them as early adopters moderately than industrial prospects; they’re testing the expertise to see what it will probably provide moderately than utilizing it in industrial operations.

The flexibility of the administration staff to completely make the most of these early adopters and their findings relating to the product might be an important factor within the success of this firm. Within the Q2 earnings name, we heard about some preliminary suggestions from the early adopters, which weren’t all optimistic. The software program didn’t ship the insights the researchers sought, and the wide range of pattern sorts, preparation methods, and pattern concentrations brought about points.

Can the administration negotiate these points and use the suggestions positively to develop QSI and its merchandise?

Firstly who’re they?

CEO Jeff Hawkins

Earlier than becoming a member of QSI, Jeff was CEO of Truvian Sciences. Truvian has developed a desktop blood testing gadget proven in July to be comparable with laboratory blood testing companies. Jeff led Truvian through the improvement of the gadget, leaving simply earlier than the product went to remaining testing and an FDA utility, because the article says the testing was profitable. (He additionally notably mentioned that Theranos was science fiction, not science).

President Patrick Schneider

Patrick was with MilliporeSigma for greater than eight years earlier than becoming a member of QSI. MilliporeSigma is a life science firm that Merck & Co (MRK) owns. Patrick was accountable for enterprise technique, partnerships, and M&A exercise.

These two guys collectively give me monumental confidence that QSI has the individuals with the proper mix of qualities to handle QSI by means of this early adopter section and transfer it towards industrial success over the subsequent 12-18 months.

Poor outcomes decreased steering.

The Merchandise

QSI is creating a protein discovery platform; earlier than Q2, they’d mentioned it will include three parts (Carbon, Platinum, and Software program).

The rationale for Carbon was convincing,

Carbon is an automatic pattern preparation gadget due for launch in 2023. I assumed Carbon can be a vital gadget growing the potential buyer pool for QSI. Pattern prep is handbook, difficult, and requires extremely skilled employees with particular expertise and information. Folks with these expertise are in excessive demand and carry excessive salaries. Throughout the Q2 earnings name, the CEO defined that the early adopters had skilled issues integrating Platinum into their workflow and {that a} change was wanted within the R&D methods of QSI; he mentioned QSI ….

had gaps when it comes to addressing the total scope and complexity of the proteomics workflow.

The CEO mentioned that Carbon is probably not one of the best long-term answer, and QSI had been now engaged on aligning their Platinum gadget with commercially obtainable liquid dealing with platforms and pattern prep chemistry that could be an equal or higher match for purchasers.

Carbon was placed on maintain within the Q2 2023 earnings launch, which resulted in decreased steering. I assumed every sale would probably be one Carbon and one Platinum within the early days.

Platinum:

The flagship product is designed to permit single molecule detection and next-generation protein sequencing historically carried out on mass spectrometry units costing as a lot as $1,000,000. The Platinum retails for $70,000, and the protein sequencing unit obtained its first gross sales in Q1 2023.

I estimate that QSI bought three units in Q1 and two in Q2. Income got here in under expectation as a result of we had been instructed QSI had two orders for Europe that had not been shipped attributable to import/export paperwork and can be shipped in Q2. It’s potential that no gross sales had been made in Q2 if the income booked was the 2 delayed units from Q1.

Quantum-Si Cloud:

Software program is a key software that makes use of the data gathered from Platinum to establish proteins and post-translational modifications that affect its location and performance inside a cell.

Early adopters have discovered the software program to carry out under their expectations, with the CEO commenting.

Early buyer suggestions recognized a set of software program options that had been essential for purchasers to effectively analyze and interpret their experimental knowledge.

Administration mentioned within the Q2 earnings name how they’ve re-distributed R&D in the direction of bettering the software program. An replace was printed in July that administration mentioned has been positively obtained and is a greater match with what the customers want.

The aim of the QSI idea is to ship the data researchers want to grasp the proteins within the pattern they’re taking a look at. One factor of that’s the Platinum gadget capturing the information from the pattern; the opposite is the software program deciphering this knowledge right into a kind usable by the researcher.

Ongoing R&D might be required to enhance this and to this point; the data from administration is optimistic. They’re responding rapidly to buyer requests, altering the main target of R&D, and delivering the modifications required. Sustaining good relations with the early adopters might be an important factor of QSI fulfilling its purpose of getting a platinum gadget in each lab globally.

The Financials

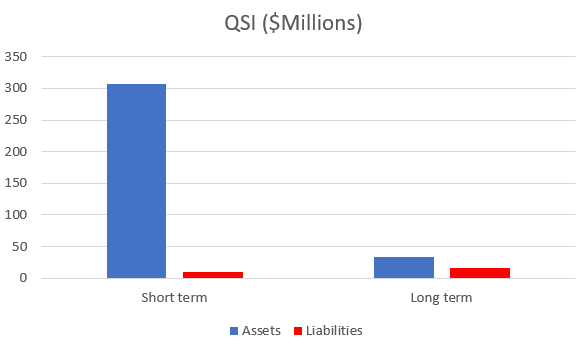

QSI has a near-flawless steadiness sheet with zero debt and a money runway effectively into 2026. With gross sales already starting and a advertising and marketing ramp up deliberate, issues look very promising.

QSI abstract Steadiness Sheet (Creator Database)

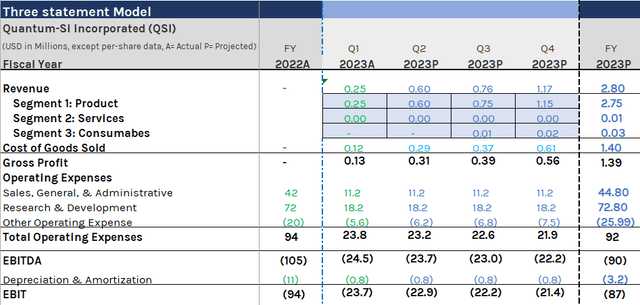

A key a part of my buying and selling plan is to construct a three-statement mannequin of an organization and use it to trace its progress and, when I’ve sufficient knowledge, produce a good worth calculation. In Q1 2023, QSI reported its first gross sales, and though it declined to present any correct steering, the earnings name contained lots of their ideas.

Beneath are some key line objects from the mannequin written earlier than the Q2 outcomes. I had forecast income of $ 0.6 million in Q2, some 50% increased than the road forecast, with a gross margin of 48%, and all different prices flat Q on Q for the 12 months. (inexperienced textual content precise knowledge, blue textual content creator forecast, black textual content calculation)

Line objects from Mannequin (Creator)

This preliminary forecast was based mostly on data gleaned from the Q1 earnings name. The income forecast included the deferred income of $0.2 to Europe and new offers in keeping with Q1 (so $0.2+$0.4). Q2 was a giant miss, and steering for the rest of the 12 months was decreased. The Carbon gadget has successfully been shelved and won’t present the This fall bump anticipated.

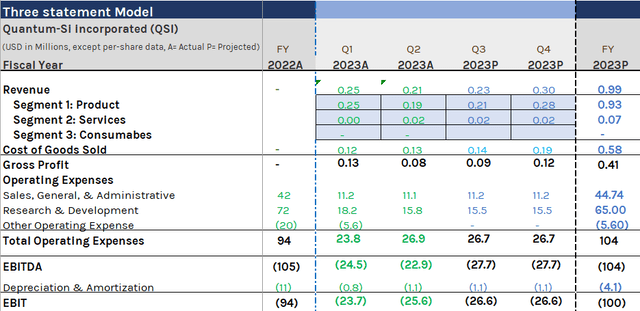

The screenshot under reveals the up to date mannequin with the Q2 knowledge changing the projected. My forecast income for FY 2023 has fallen from $2.8 million to $0.99 million. Margins dropped from 48% to 38%.

Up to date mannequin (Creator)

I’ll replace the mannequin every quarter, and the forecasts will grow to be extra correct as I do. Future articles will comprise the updates.

Conclusion

Shares fell over 30% following the Q2 outcomes and proceed to fall. Income missed by 50% margins got here in effectively under expectations. Carbon was faraway from sale, and issues with software program had been recognized.

It sounds horrible, but when, as administration suggests, Carbon was unlikely to promote because of the buyer’s workflow, then there was little level in bringing it to market or spending any additional cash to develop it.

The early adopters highlighted Software program points, and rapidly redeploying employees resolved these points.

The modifications led to a major drop in R&D expenditure, down $2.4 million from Q1 2023, and a smaller drop in SG&A regardless of growing advertising and marketing efforts, which speaks to strong money preservation methods.

The administration has the expertise to navigate this early income / early adopter section and their actions in transferring rapidly to refocus the R&D in gentle of buyer suggestions, delivering a software program replace in July, and stopping improvement of the carbon product in favor of integrating the Platinum gadget with present workflows will assist the longer term gross sales of Platinum which was at all times going to be the make or break product.

The market is big, QSI has the primary product obtainable at a decrease price and all proof suggests it really works effectively and is correct. It isn’t but the ultimate model however QSI are transferring rapidly to present researchers the output they need and want.

I did have two positions in QSI, one from simply after the Q1 report at $1.58 and the opposite final week at $3.10 after I was anticipating an earnings beat. The 2 positions closed for a small combination loss when the share worth gapped decrease on the market open Monday, August seventh.

I’ll purchase once more after I suppose the present drop is full and replace within the feedback after I do.

{kind=link}