ipuwadol/iStock by way of Getty Photos

A Fast Take On Pegasystems

Pegasystems Inc. (NASDAQ:PEGA) offers workflow automation software program and associated companies to enterprises worldwide.

I beforehand wrote about PEGA with a Maintain outlook.

Whereas Pegasystems Inc. could have some potential for an upside shock, given identified macroeconomic softness and a slower ahead income progress fee, I stay Impartial [Hold] on PEGA within the close to time period.

Pegasystems Overview

Cambridge, Massachusetts-based Pegasystems was based in 1983 and sells a wide range of workflow automation software program to main business verticals.

The agency is headed by founder and CEO Alan Trefler, who can be founding father of the Trefler Basis.

The corporate’s major choices embrace the next:

-

Platform.

-

Buyer Determination Hub.

-

Buyer Service.

-

Gross sales Automation.

-

Consumer Lifecycle Administration.

-

Know Your Buyer.

The agency acquires prospects by its direct gross sales and advertising and marketing efforts in addition to by accomplice referrals.

PEGA additionally operates a Market, Companion Portal and Launchpad.

Pegasystems’s Market & Competitors

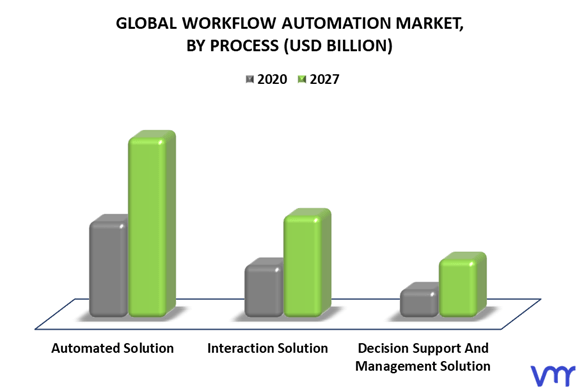

In accordance with a 2022 market analysis report by Verified Market Analysis, the worldwide marketplace for workflow automation was estimated at $8 billion in 2019 and is forecast to achieve $39.5 billion by 2027.

This represents a forecast very excessive CAGR of 23.7% from 2020 to 2027.

The primary drivers for this anticipated progress are demand from varied main business verticals for improved digital processes that may drive real-world product efficiencies, decrease prices and enhance gross sales volumes.

Additionally, the chart beneath exhibits the worldwide workflow automation market progress outlook by the three predominant classes of resolution:

World Workflow Automation Market (Verified Market Analysis)

Main aggressive or different business members embrace:

-

IBM.

-

Appian.

-

Oracle.

-

Software program AG.

-

Newgen.

-

AURA.

-

AgilePoint.

-

Agiloft.

-

Monday.com.

-

Jira.

-

Others.

Pegasystems’ Current Monetary Traits

-

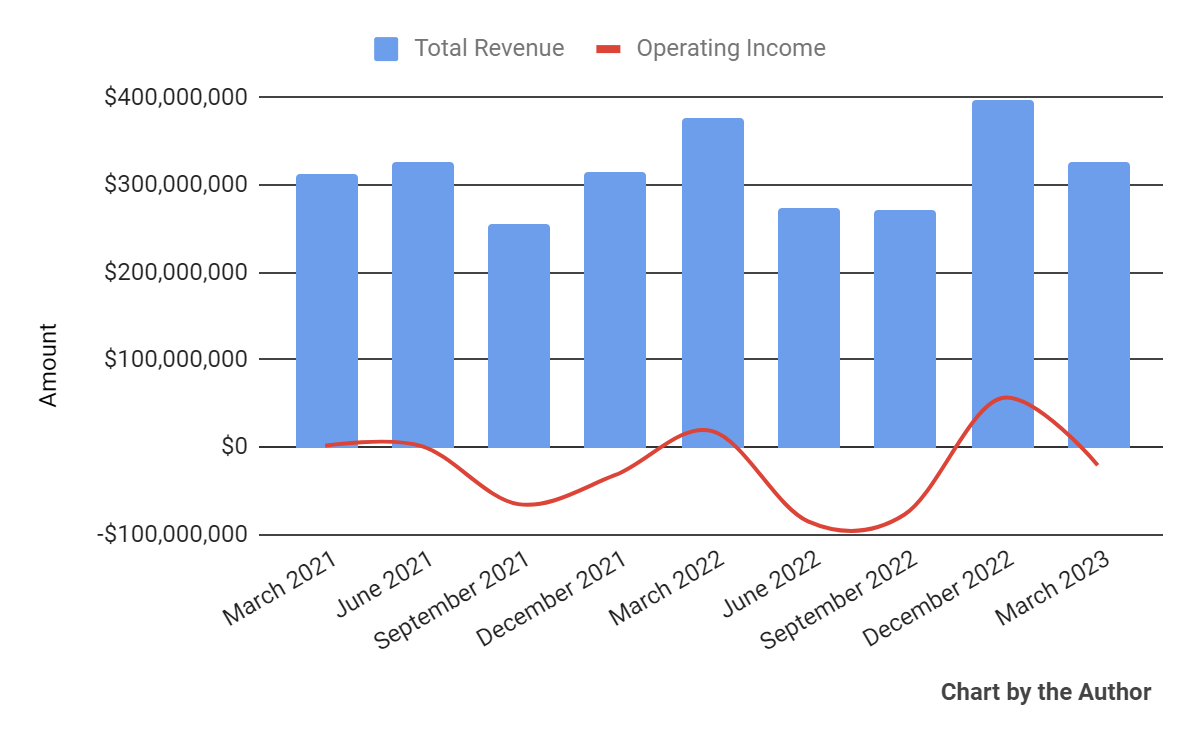

Complete income by quarter has fallen YoY for the latest quarter; Working earnings by quarter has fluctuated markedly.

Complete Income and Working Earnings (Searching for Alpha)

-

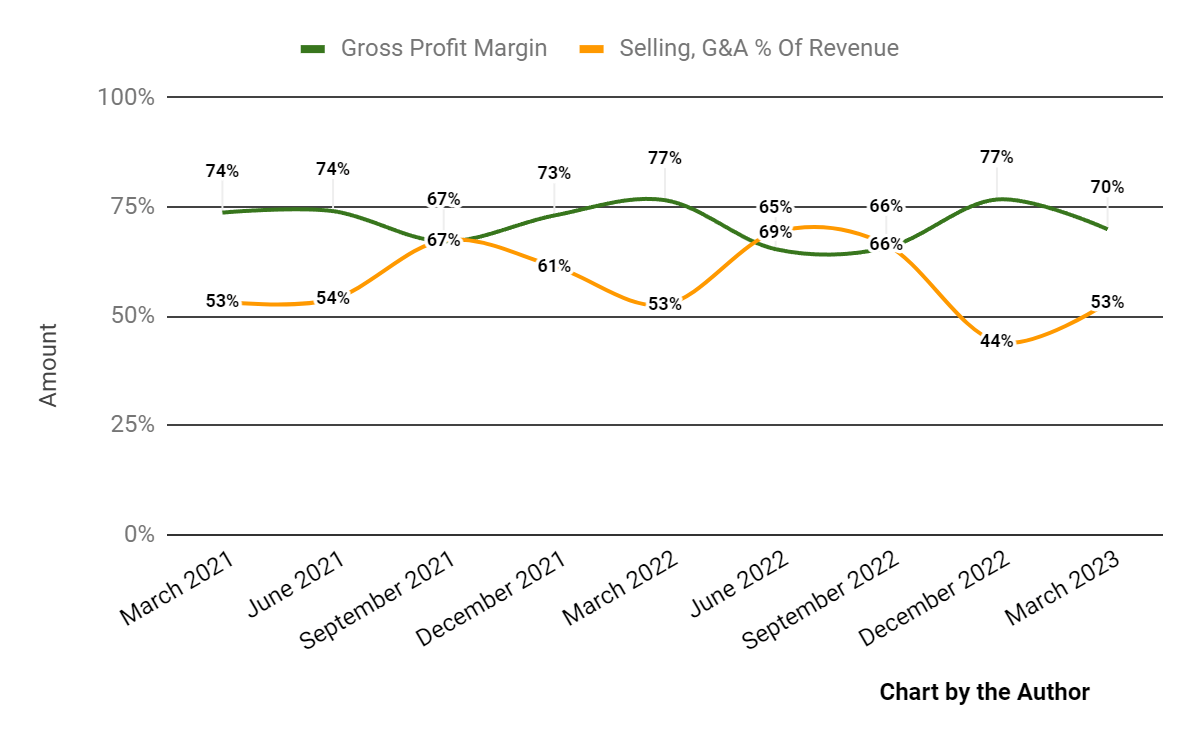

Gross revenue margin by quarter has trended decrease in current quarters; Promoting, G&A bills as a share of whole income by quarter have dropped sharply just lately.

Gross Revenue Margin and Promoting, G&A % Of Income (Searching for Alpha)

-

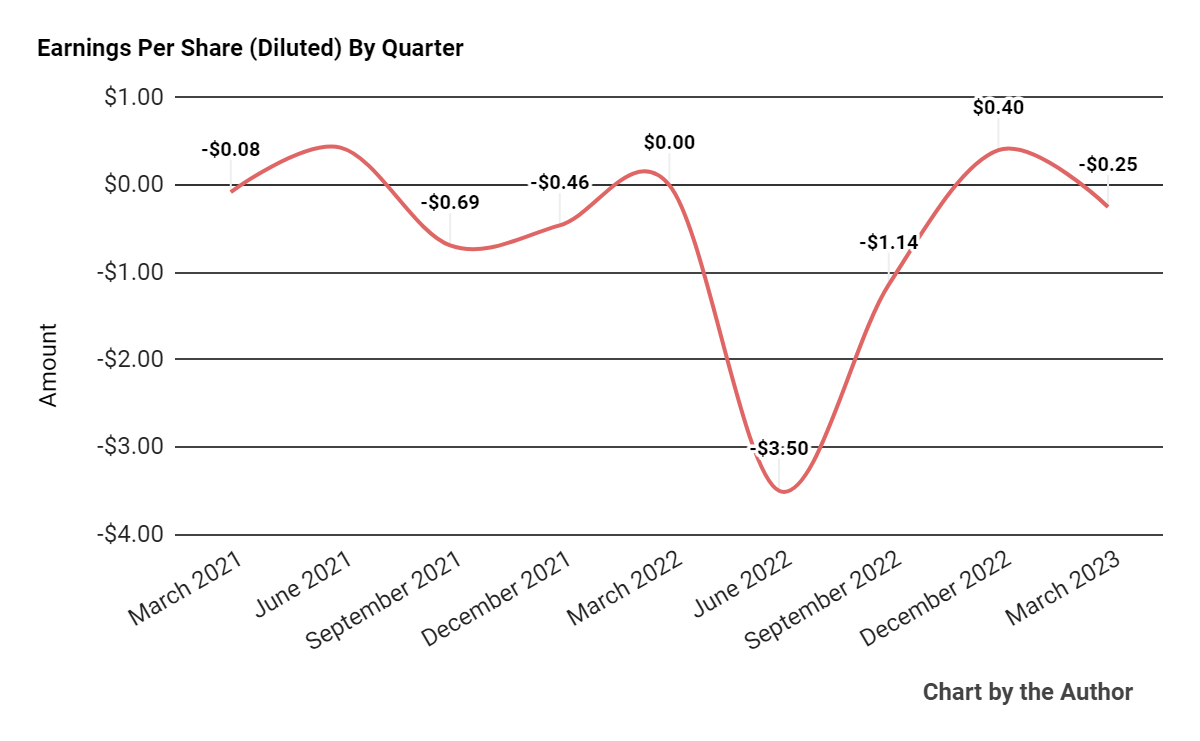

Earnings per share (Diluted) have produced extensive fluctuations in current quarters.

Earnings Per Share (Searching for Alpha)

(All information within the above charts is GAAP.)

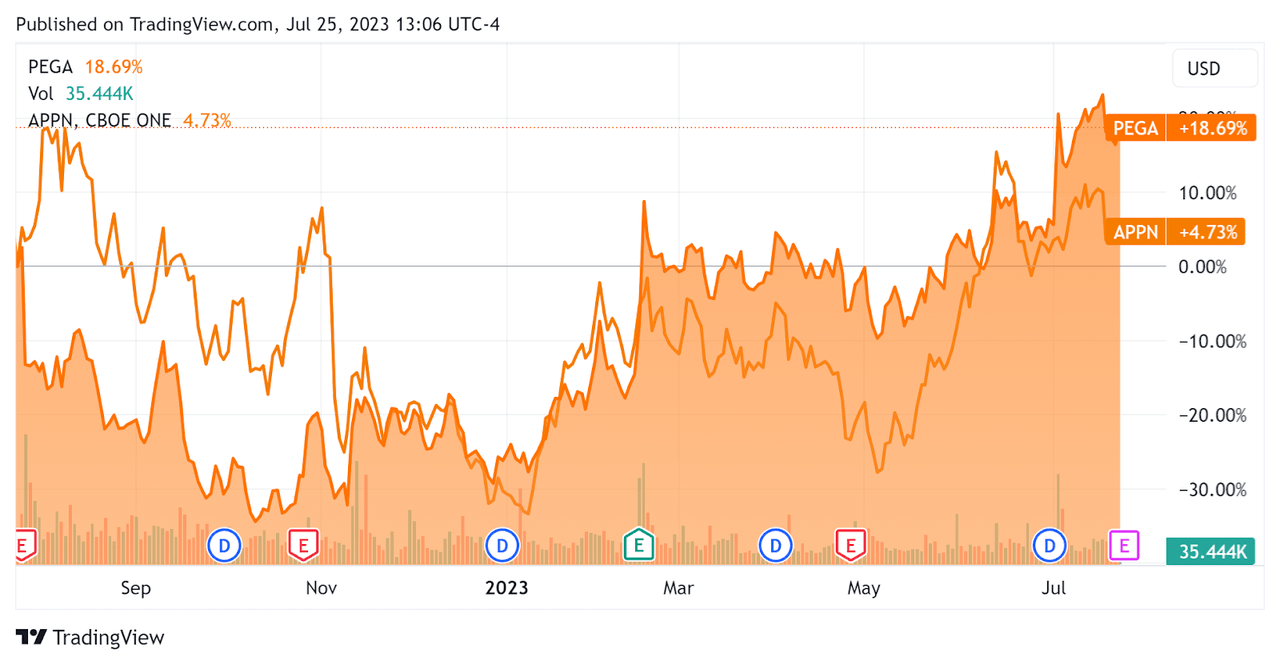

Previously 12 months, PEGA’s inventory worth has risen 18.69% vs. that of Appian Company (APPN) progress of solely 4.73%, because the chart signifies beneath.

52-Week Inventory Value Comparability (Searching for Alpha)

Pegasystems ended the quarter with $323.9 million in money, equivalents and short-term investments and $561.7 million in whole debt, none of which was categorized as the present portion due inside 12 months.

Over the trailing twelve months, free money move was $35.1 million, throughout which capital expenditures had been a hefty $40.2 million. The corporate paid $136.5 million in stock-based compensation within the final 4 quarters, the best trailing twelve-month determine prior to now eleven quarters.

Valuation And Different Metrics For Pegasystems

Under is a desk of related capitalization and valuation figures for the corporate.

|

Measure [TTM] |

Quantity |

|

Enterprise Worth / Gross sales |

3.8 |

|

Enterprise Worth / EBITDA |

NM |

|

Value / Gross sales |

3.5 |

|

Income Development Price |

-0.6% |

|

Internet Earnings Margin |

-28.9% |

|

EBITDA % |

-8.5% |

|

Internet Debt To Annual EBITDA |

-2.2 |

|

Market Capitalization |

$4,520,000,000 |

|

Enterprise Worth |

$4,850,000,000 |

|

Working Money Movement |

$75,330,000 |

|

Earnings Per Share (Absolutely Diluted) |

-$4.49 |

(Supply – Searching for Alpha)

As a reference, a related partial public comparable could be low-code firm Appian; proven beneath is a comparability of their major valuation metrics.

|

Metric [TTM] |

Appian |

Pegasystems |

Variance |

|

Enterprise Worth / Gross sales |

7.3 |

3.8 |

-47.5% |

|

Enterprise Worth / EBITDA |

NM |

NM |

–% |

|

Income Development Price |

23.9% |

-0.6% |

–% |

|

Internet Earnings Margin |

-33.7% |

-28.9% |

-14.2% |

|

Working Money Movement |

-$111,210,000 |

$75,330,000 |

–% |

(Supply – Searching for Alpha)

The Rule of 40 is a software program business rule of thumb that claims that so long as the mixed income progress fee and EBITDA share fee equal or exceed 40%, the agency is on an appropriate progress/EBITDA trajectory.

PEGA’s most up-to-date unadjusted Rule of 40 calculation was unfavorable (9.1%) as of Q1 2023’s outcomes, so the agency’s efficiency has worsened sequentially, per the desk beneath.

|

Rule of 40 Efficiency (Unadjusted) |

This fall 2022 |

Q1 2023 |

|

Income Development % |

8.8% |

-0.6% |

|

EBITDA % |

-5.2% |

-8.5% |

|

Complete |

3.6% |

-9.1% |

(Supply – Searching for Alpha)

Commentary On Pegasystems

In its final earnings name (Supply – Searching for Alpha), overlaying Q1 2023 outcomes, administration highlighted the curiosity the agency is receiving from shoppers concerning using AI applied sciences.

So, the agency seeks to teach prospects and prospects about its integration of AI into its varied merchandise and its plans to develop generative AI applied sciences sooner or later.

Pega goals to allow its shoppers to include AI capabilities by way of their very own API permissions into its Pega Infinity platform, like plug-in modules, growing the extent of customization accessible to prospects.

Administration did not disclose any firm, buyer, or income retention fee metrics.

Complete income for Q1 2023 dropped 13.5% year-over-year whereas gross revenue margin fell 6.7% YoY.

Promoting, G&A bills as a share of income rose by 0.5 share factors YoY and working earnings fell sharply into unfavorable territory.

The corporate’s monetary place is reasonable with important liquidity offset by long-term debt; free money move was constructive.

PEGA’s Rule of 40 efficiency has worsened sequentially into unfavorable territory.

Trying forward, administration had beforehand guided prime line 2023 full-year income of $1.4 billion, for a progress fee of 6.2%.

If achieved, this could signify a lowered progress fee versus 2022’s progress fee of 8.76% over 2021.

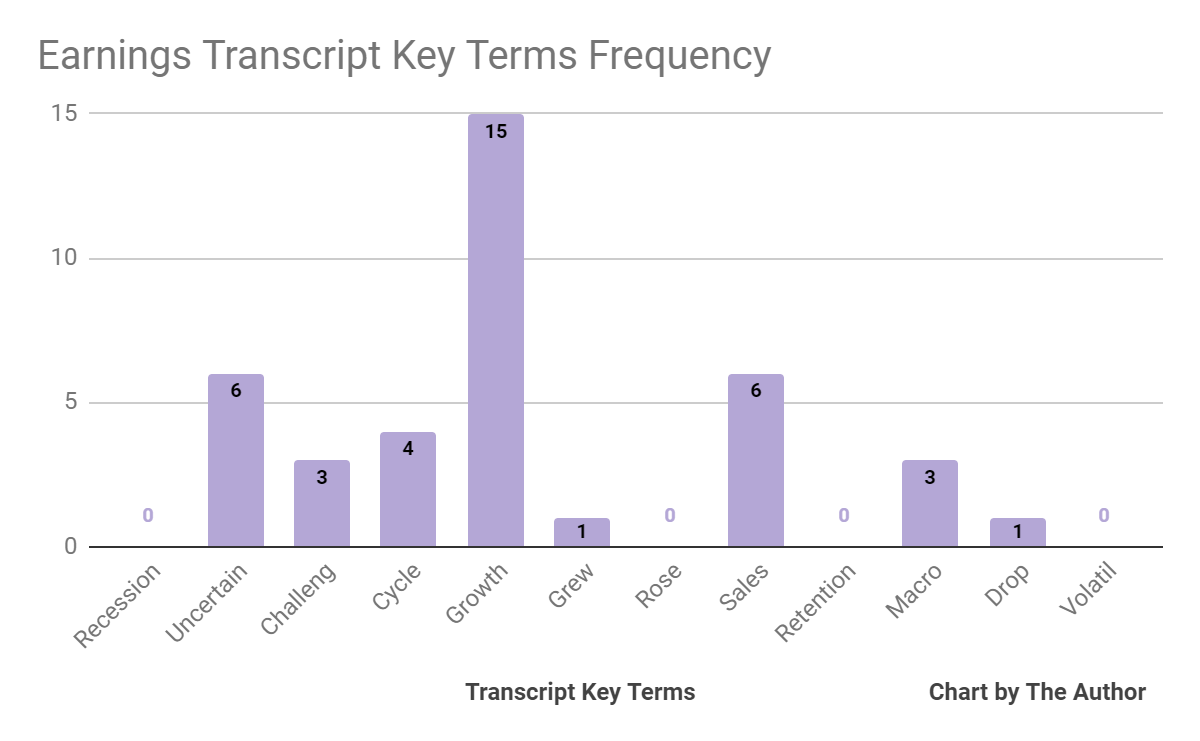

From administration’s most up-to-date earnings name, I ready a chart exhibiting the frequency of key phrases talked about (or not) within the name, as proven beneath.

Earnings Transcript Key Phrases Frequency (Searching for Alpha)

I am most within the frequency of probably unfavorable phrases, so administration or analyst questions cited “Unsure” six instances, “Challeng[es][ing]” 3 times, “Macro” 3 times and “Drop” as soon as.

Analysts questioned firm management about lengthening of gross sales cycles, to which administration responded by saying that it’s seeing higher “financial concern” and a form of “timidity” by prospects and prospects.

Concerning valuation, prior to now twelve months, the agency’s EV/Gross sales valuation a number of has risen from the underside of two.33x in October 2022 to its present degree of three.79, for an increase of 62.6% off the low, because the chart from Searching for Alpha exhibits beneath.

EV/Gross sales A number of Historical past (Searching for Alpha)

The first enterprise danger to the corporate’s outlook is slowing progress attributable to lengthened gross sales cycles as Pegasystems seeks to proceed to transition to a subscription income mannequin.

Potential upside to the agency’s fortunes may embrace capitalizing on the sturdy curiosity in AI-enhanced applied sciences.

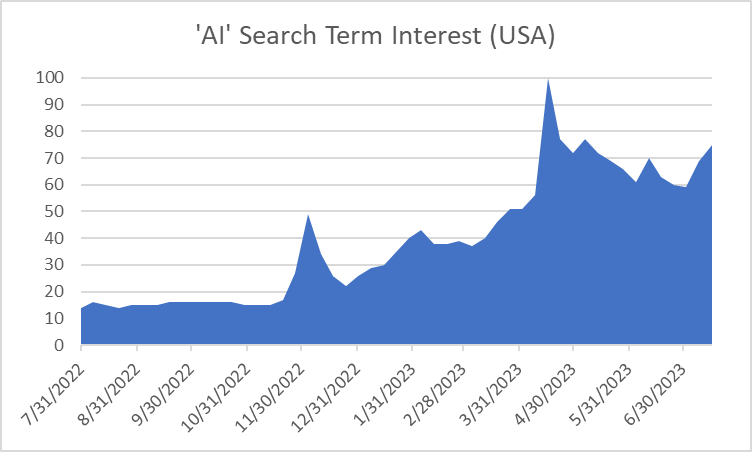

Actually, with income steering for 2023 indicating slower progress than 2022’s progress over 2021, a lot of the inventory’s rise has been pushed by an increase in its worth a number of and, I believe, from the narrative surrounding AI in course of automation.

Can the inventory proceed to rise? In fact, the AI hype could proceed, though this search time period historical past exhibits some drop in curiosity in current months:

AI Search Time period Curiosity – USA (Google Traits)

Whereas Pegasystems could have some potential for an upside shock, given identified macroeconomic softness and a slower ahead income progress fee, I am Impartial [Hold] on PEGA within the close to time period.

{kind=link}