izusek

We beforehand coated PayPal Holdings (NASDAQ:PYPL) in November 2023, discussing the pessimistic sentiments surrounding the declining Energetic Accounts and the impacted transaction margins from the dilutive Braintree phase.

Nonetheless, we maintained our bullish stance surrounding PYPL’s prospects, with the underside possible close to, thanks to the refreshed administration workforce and the inventory’s moderating exponential curve.

On this article, we will focus on how the PYPL inventory’s pre-earning efficiency has exceeded expectations, with the administration’s weak FY2024 steering sadly reversing its upward momentum.

Regardless of so, we keep our optimism surrounding its eventual turnabout, with the brand new administration already introducing extremely promising development initiatives whereas shedding further headcounts, with 2024 prone to carry forth prime/ backside line beats regardless of the prudent steering.

The PYPL Funding Thesis Stays Sturdy, Thanks To The Administration’s Progress Initiatives & Prudent Steering

For now, PYPL continued to report a double beat FQ4’23 earnings name, with revenues of $8.03B (+8.2% QoQ/ +8.8% YoY) and adj EPS of $1.48 (+13.8% QoQ/ +19.3% YoY), constructing upon a number of beats over the previous few years.

Most significantly, regardless of the market issues for its declining whole lively accounts to 426M (-2M QoQ/ -9M YoY), the fintech’s whole fee quantity continues to develop to $409.83B (+5.7% QoQ/ +14.7% YoY).

These numbers point out a sustained YoY acceleration noticed since FQ2’23 and the rising stickiness of its platform amongst loyal customers.

With PYPL’s FQ4’23 whole lively accounts and whole fee quantity already rising tremendously from FQ4’19 ranges of 305M and $199B, respectively, we aren’t overly involved about its briefly impacted transaction margin of 45.8% (+0.4 factors QoQ/ -3.9 YoY) in comparison with FQ4’19 ranges of 53.8% (+0.4 factors QoQ/ -0.9 YoY).

Most significantly, the brand new administration already guided flat transaction margin {dollars} in FY2024, implying that their efforts to drive value efficiencies and speed up development might bear fruit over the following few quarters, placing a cease within the decline of its revenue margins.

Consequently, PYPL buyers solely have to patiently wait out the transitionary interval, with a number of layoffs already introduced. As well as, the administration launched a number of new development initiatives within the First Look Name on January 25, 2024:

- Fastlane by PayPal – Accelerated checkout course of, projected to cut back completion time by as a lot as 50%. Early implementation by BigCommerce is already yielding elevated conversion by +70%, with the worldwide rollout prone to carry forth larger fee volumes.

- Sensible Receipts – With 45% in open charge for PYPL’s e-mail receipts, retailers might entice prospects to be repeat purchasers by means of AI-generated customized suggestions and loyalty rewards on receipts.

- PayPal’s new Superior Presents Platform on a brand new client app – providing buying affords and rewards by means of customized commercials, because of the AI-generated suggestions.

- PayPal CashPass – PYPL’s new cashback affords from a number of prime manufacturers within the US, together with: Uber (UBER), Walmart (WMT), Greatest Purchase (BBY), McDonald’s (MCD), Ticketmaster, and eBay (EBAY), with no restrict in cashbacks. Prospects are additionally allowed to stack a number of cashback affords from retailers, PYPL, and fee companions, corresponding to PayPal Cashback Mastercard (MA).

- Venmo Enterprise Profiles – The combination of social media/ advertising and marketing outreach/ cashback affords on the digital pockets platform, with cashback immediately saved in buyer’s Venmo stability.

Due to this fact, anybody involved in regards to the supposedly weak FY2024 steering might need to perceive that it’s extra prudent for PYPL to set a decrease bar after which beat these estimates over the following 4 quarters, particularly since these development initiatives are anticipated to be launched from Q1’24 onwards.

For now, the identical competence has already been noticed in its bettering stability sheet, with rising web money of $4.38B (+386.6% QoQ/ +873.3% YoY/ -24% from FY2019 ranges of $5.8B).

That is on prime of the superb shareholder returns to date, with 60M shares or the equal 5.5% of its float already retired during the last twelve months, and 90M / 8.3% since FY2019, respectively.

The Consensus Ahead Estimates

Searching for Alpha

For now, the consensus stays bearish on PYPL’s prospects, with it anticipated to document a decelerating prime/ backside line development at a CAGR of +7.4%/ +7.1% by means of FY2026, worsened by the administration’s weak FY2024 steering.

That is in comparison with the earlier estimates of +13.4%/ +15.6% and the historic development at a CAGR of +15.5%/ +19.1% between FY2016 and FY2023, respectively.

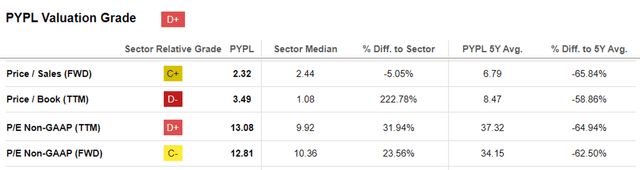

PYPL Valuations

Searching for Alpha

Because of the constant downgrades, we are able to perceive why the market continues to low cost PYPL’s FWD P/E valuations at 12.81x. That is in comparison with its direct friends, corresponding to Block (SQ) at 35.38x, MA at 32.07x, Visa (V) at 28.18x, and SoFi (SOFI) at 57.13x.

Nonetheless, readers should additionally word that the market has reasonably upgraded PYPL’s FWD P/E valuations from the 9.42x recorded within the October 2023 backside.

These numbers suggest that the PYPL inventory stays extraordinarily undervalued particularly when in comparison with its 3Y pre-pandemic imply of 32.28x, with it being a superb worth play candidate.

So, Is PYPL Inventory A Purchase, Promote, or Maintain?

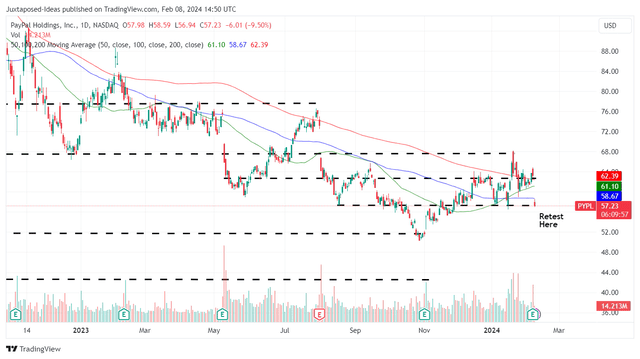

PYPL 1Y Inventory Value

Buying and selling View

Previous to the earnings name, PYPL has quickly bounced from the October 2023 backside, broke out of the 50/ 100/ 200 day transferring averages, whereas showing to retest the earlier resistance ranges of $60s. The +11.6% restoration has exceeded expectations certainly, regardless of it underperforming the SPY by +14.4% over the identical time interval.

Sadly, the weak steering has additionally reversed its latest good points, with the inventory’s upward momentum successfully halted and the earlier assist ranges of $60s breached.

Nonetheless, right here is the place we keep our bullishness, with the brand new PYPL administration decided to show the ship round by means of drastic efforts and prudent steering, as outlined above.

Mixed with the constant profitability and wholesome stability sheet, we imagine that the inventory’s October 2023 backside of $50 might maintain, providing buyers with the chance so as to add relying on their greenback value averages.

With the selloff being overly completed, we proceed to charge PYPL as a Purchase for affected person buyers, with the inventory’s upward rerating a probable incidence over the following few years.

{kind=link}