Otter Tail Company (NASDAQ:OTTR) is a regulated electrical utility serving prospects in Minnesota and each of the Dakotas. The utility sector is mostly a favourite amongst conservative buyers comparable to retirees as a result of its common stability by any form of macroeconomic setting. Otter Tail Company is one thing of an oddity amongst utilities although for the reason that firm additionally has a producing arm. This manufacturing arm proved to be one thing of a legal responsibility for the corporate in the course of the pandemic as a result of the shut downs had fairly an opposed impact on the companies that comprise this space. They’ve since recovered in a really huge approach, nonetheless, and right this moment the company’s efficiency is basically again to regular. In actual fact, the corporate’s most up-to-date outcomes present appreciable development in comparison with 2020, which is basically what I predicted in my final article on the corporate. Otter Tail is positioned to proceed to ship development over the approaching years and after we mix this with a really affordable valuation, it is perhaps value contemplating in your portfolio.

About Otter Tail Company

As acknowledged within the introduction, Otter Tail Company is primarily a regulated electrical utility serving prospects in components of Minnesota and the Dakotas:

Otter Tail Investor Presentation")

The corporate additionally has a couple of supplies manufacturing companies that shall be mentioned later on this report. Nonetheless, since 70% of the corporate’s income come from the electrical utility, it needs to be largely considered on this approach. It is a lucky factor for a sure sort of investor as a result of utility firms are inclined to get pleasure from remarkably steady funds over time and thru any financial situations. It’s because utilities present a product that’s usually thought-about to be a necessity for our fashionable lifestyle. Consequently, individuals will usually prioritize paying their utility payments forward of different extra discretionary bills throughout occasions when cash will get tight. This was particularly useful in the course of the occasions of 2020 as utilities like Otter Tail Company have been capable of climate by the financial calamities of that yr a lot better than firms in quite a few different industries.

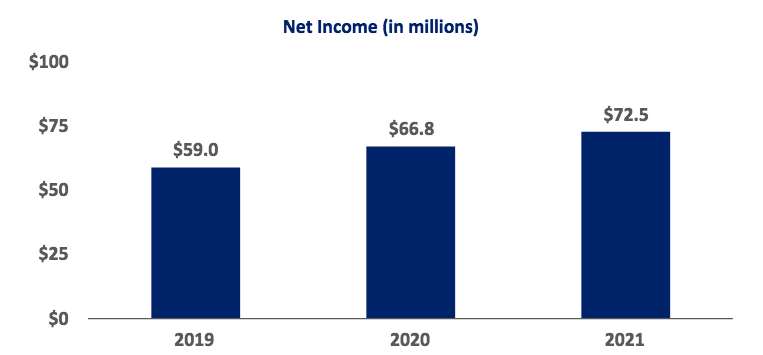

One other defining attribute of utilities is that they usually ship sluggish however regular development. Otter Tail has not been an exception to this because it has grown the online earnings from its utility operations throughout every of the previous three years:

Otter Tail Investor Presentation

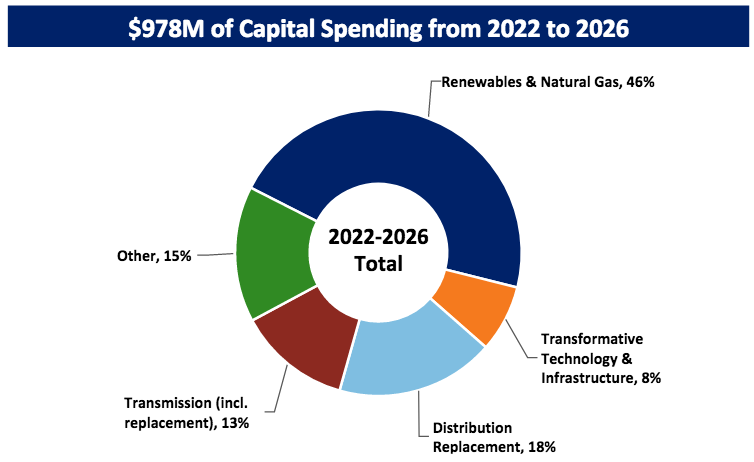

This is because of the truth that these firms are continually rising their price bases. The speed base is the worth of the utility’s property upon which regulators permit it to earn a specified price of return. As this price of return is a proportion, any enhance to its worth permits the corporate to extend the costs that it expenses its prospects as a way to earn that price of return. The same old approach {that a} utility will increase its price base is by investing cash into upgrading, modernizing, and even increasing its utility infrastructure. That is precisely what Otter Tail Company has been doing, a pattern that it intends to proceed going ahead. Over the 2022 to 2026 interval, the corporate plans to speculate $978 million into rising its price base:

Otter Tail Investor Presentation

This could have the impact of rising the corporate’s price base at a 5.9% compound annual development price over the interval, taking it from $1.58 billion right this moment to $2.10 billion by the top of 2026. As some astute readers might level out, it is a decrease worth enhance than the amount of cash that the corporate is investing. There are two causes for this. The primary motive is that a number of the firm’s spending is earmarked for the acquisition of things that may exchange property being taken out of service. Specifically, Otter Tail is anticipating to close down the Hoot Lake Coal Plant within the close to future. As soon as this plant is retired, its worth shall be instantly faraway from the corporate’s price base, which can naturally offset a number of the spending impacts. The second motive why the speed base development won’t be as nice because the amount of cash that the corporate is investing in it’s depreciation. Principally, the worth of the corporate’s property is all the time reducing so one thing that it buys in 2022 in the beginning of this funding program shall be value far much less in 2026. In brief, the corporate’s price base would regularly decline if the corporate isn’t continually investing cash into it. Whereas this does present some tax advantages, it additionally, sadly, offsets a number of the firm’s spending, forcing it to speculate greater than it in any other case would. The corporate has guided for midpoint earnings per share of $1.83 from its electrical utility operation in 2022, which might be a 5.78% enhance over the determine that it had in 2021. Nonetheless, since 30% of the company’s income come from different sources, we should always not undertaking an funding return based mostly solely on this determine.

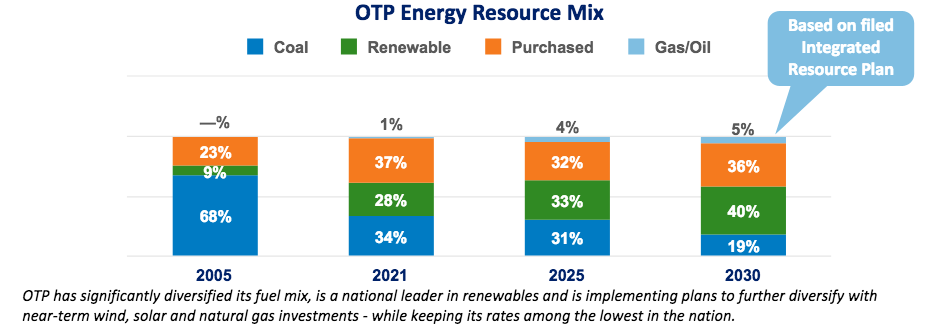

One space the place Otter Tail is investing closely in is the event and deployment of renewables, as we are able to see within the chart above. That is an space by which many electrical utilities are investing, which is basically as a result of calls for of regulators and prospects. Nonetheless, Otter Tail isn’t being as aggressive about its sustainability objectives as a few of its friends. As I’ve famous in a couple of latest articles, there are a number of utilities which have acknowledged their intentions to retire all of their remaining operational coal energy vegetation by 2025. That is largely as a result of the truth that coal energy, generally, is rather more closely polluting than every other technique of producing electrical energy. Otter Tail, in the meantime, is just planning to cut back the proportion of its electrical energy that’s generated by coal however not take away it completely within the close to time period. Certainly, by 2030, the corporate expects 19% of its electrical energy to return from coal as in comparison with 34% right this moment:

Otter Tail Investor Presentation

Sadly, this may occasionally trigger Otter Tail to underperform a number of the different electrical utilities within the business. It’s because it won’t have the benefit of assist from the varied environmental, social, and governance funds which have sprung up over the previous few years. These funds ostensibly spend money on these firms which have an emphasis on sustainability and variety of their enterprise fashions, which might usually imply these electrical utilities with a heavy reliance on renewables on the expense of coal. As I mentioned in a latest article, the recognition of those funds has grown to the purpose the place they now management 10% of all worldwide mutual fund property. That is greater than sufficient cash to push up the inventory worth of any utility and it appears much more probably that these funds would choose to spend money on certainly one of Otter Tail’s friends that’s not using coal relatively than Otter Tail. Finally, this might trigger Otter Tail to underperform a few of its friends.

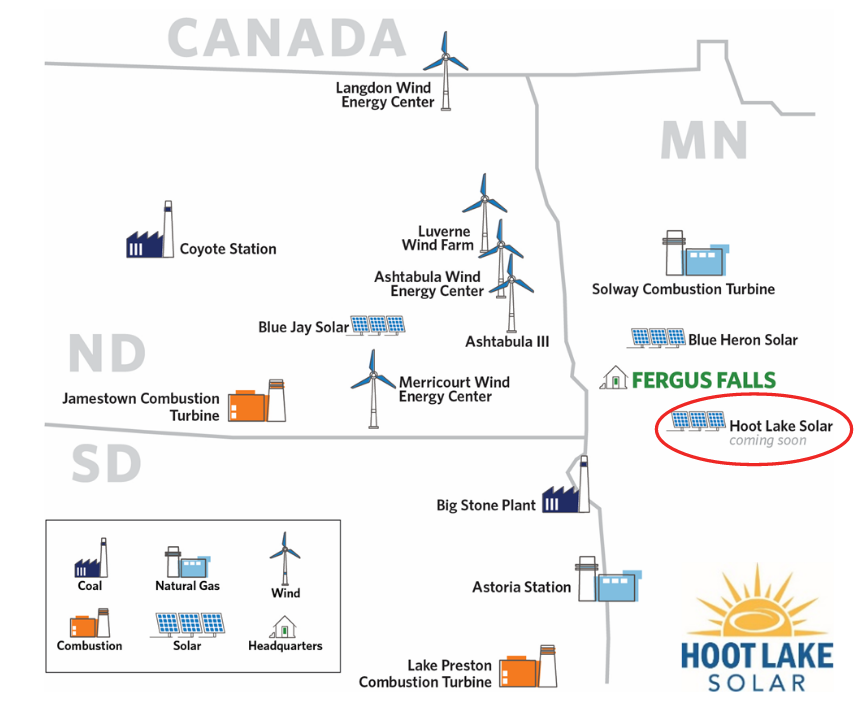

Otter Tail is definitely not and not using a portfolio of renewable initiatives, nonetheless. One of many firm’s present initiatives is the Hoot Lake Photo voltaic Plant, which it’s developing close to Fergus Falls, Minnesota:

Otter Tail Investor Presentation

The Hoot Lake Photo voltaic Plant is able to producing 49.9 megawatts of electrical energy at full capability, which is admittedly nowhere near what a fossil fuel-driven plant might produce however no less than it’s nonetheless one thing. This facility is predicted to return on-line in 2023 and it’ll assist offset a number of the misplaced era capability from the retirement of the Hoot Lake Coal Plant.

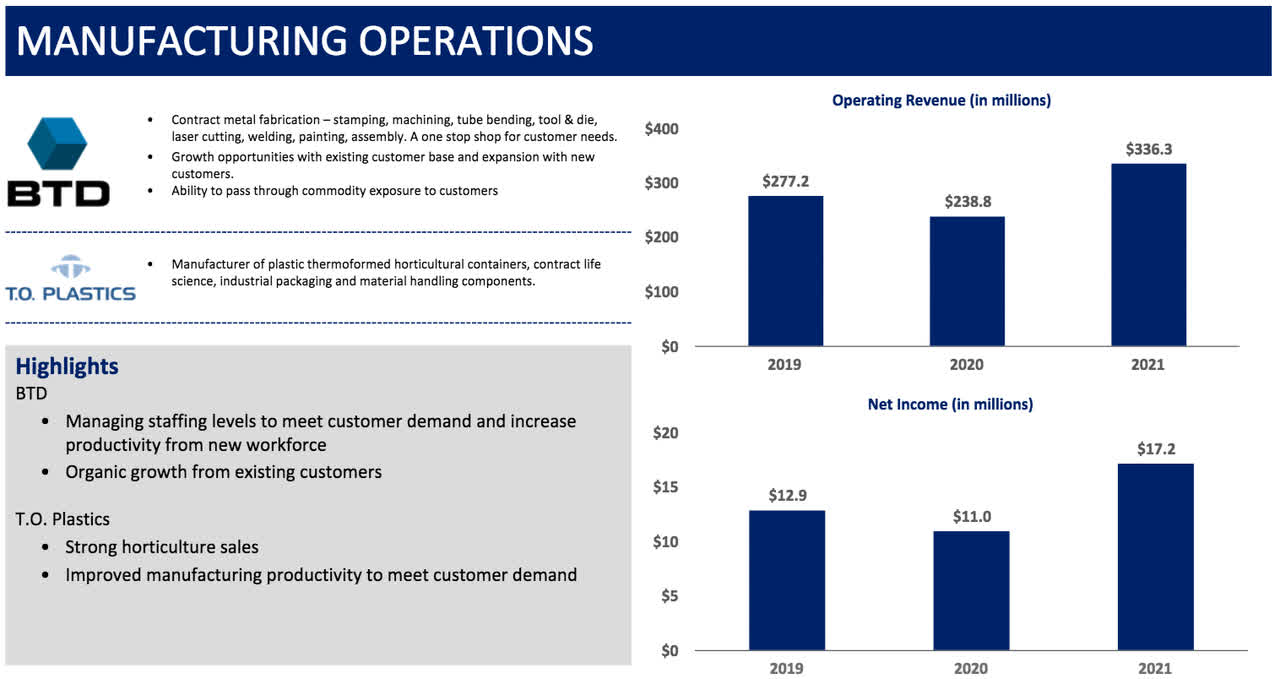

As acknowledged earlier, about 30% of Otter Tail’s income come from its numerous manufacturing companies. These companies primarily manufacture issues comparable to personalized plastic objects comparable to containers for numerous horticultural merchandise in addition to commodity objects comparable to PVC pipes. One of many good issues about many of those merchandise is that the demand for them is considerably recession-resistant, which allowed the company’s manufacturing arm to carry up moderately effectively by the coronavirus lockdowns and the next recession. That is definitely to not say that they carried out completely although as the corporate’s metal-stamping enterprise did see income and web earnings decline in 2020 in comparison with 2019. Nonetheless, it has since recovered and the 2021 numbers got here in a lot better than both 2019 or 2020:

Otter Tail Investor Presentation

That is definitely an excellent signal, notably for the reason that demand for these merchandise is unlikely to go away. As such, the corporate’s manufacturing unit might show to be an extra avenue of development for Otter Tail Company going ahead.

Fundamentals Of Electrical energy

As roughly 70% of Otter Tail’s income come from its electrical utility, we should always check out the basics of those firms. Electrical utilities, generally, have been within the funding media an abnormally great amount currently, which might be as a result of electrification pattern. That is one thing that has been very closely promoted by politicians and progressive futurists and it refers back to the conversion of issues which can be historically powered by fossil fuels to using electrical energy as a substitute. Essentially the most generally cited targets for conversion are transportation (electrical vehicles) and area heating however there are definitely different issues that may very well be transformed as effectively. Naturally, as this pattern progresses, it may be anticipated to considerably enhance the consumption of electrical energy and by extension the revenues and income of electrical utilities.

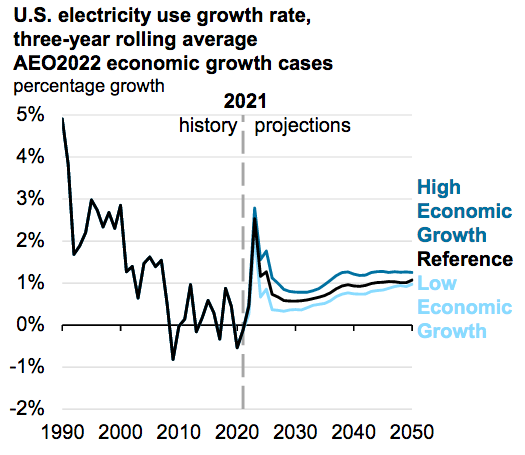

Sadly, the U.S. Power Info Administration doesn’t consider that this pattern will progress wherever close to as shortly as its proponents anticipate. In line with the federal government company, the nationwide consumption of electrical energy will enhance at a 1% to 2% price over the following thirty years:

U.S. EIA 2022 Annual Power Outlook

That is nowhere near the expansion price that will end result have been vast swathes of the economic system changing from fossil fuels to electrical energy. Certainly, I mentioned the impression that electrical vehicles alone would have in a latest article. The company is almost definitely appropriate that the conversion to an all-electric economic system shall be a really sluggish course of since constructing out the electrical grid to the purpose the place it may possibly truly assist the widespread use of electrical energy to the diploma that the proponents of electrification want is extraordinarily cost-prohibitive. Thus, it seems that electrical utilities comparable to Otter Tail will probably ship the identical sluggish and regular development that they all the time have.

Monetary Issues

It’s all the time necessary to have a look at the way in which that an organization funds itself earlier than investing into it. It’s because debt is a riskier solution to finance an organization than fairness as a result of debt have to be repaid. As few firms have adequate money to utterly repay their debt because it matures, this reimbursement is often achieved by issuing new debt and utilizing the cash from that issuance to repay the maturing debt. Relying in the marketplace situations, this may occasionally end result within the firm’s curiosity prices rising. Along with this, the corporate should make common funds on its debt whether it is to stay solvent. Thus, a decline in money flows might push it into monetary misery if it has an excessive amount of debt. Though utilities are inclined to get pleasure from remarkably steady money flows, bankruptcies are definitely not unprecedented within the sector.

One metric that we are able to use to research an organization’s monetary construction is the online debt-to-equity ratio. This tells us the diploma to which an organization is financing its operations with debt versus wholly-owned funds. As well as, this ratio tells us how effectively the corporate’s fairness can cowl its debt obligations within the occasion of a chapter or liquidation occasion, which is arguably extra necessary.

As of December 31, 2021, Otter Tail Company had $873.1 million in web debt towards $990.8 million in shareholders’ fairness. This offers the corporate a web debt-to-equity ratio of 0.88. It is a remarkably low ratio for an electrical utility, as we are able to see right here:

|

Firm |

Web Debt-to-Fairness Ratio |

|

Otter Tail Company |

0.88 |

|

NextEra Power (NEE) |

1.19 |

|

Exelon Company (EXC) |

1.22 |

|

DTE Power (DTE) |

2.09 |

|

CMS Power (CMS) |

1.68 |

|

AES Company (AES) |

3.68 |

As we are able to see, Otter Tail Company is considerably much less leveraged than its friends, which might be as a result of firm’s manufacturing arm. It’s because manufacturing is inherently a considerably riskier exercise than working a utility so producers usually are not capable of assist as a lot leverage. Both approach although, we are able to clearly see that Otter Tail’s debt load mustn’t pose a very outsized threat to buyers.

Dividend Evaluation

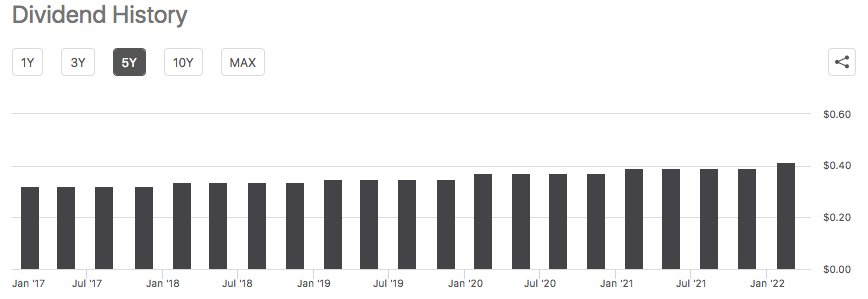

One of many greatest the reason why buyers buy shares of utility firms is as a result of they usually have a better dividend yield than firms in lots of different industries. That is as a result of usually sluggish development of the sector, which leads to them returning a better proportion of their complete return within the type of direct funds to buyers than firms in lots of different sectors. Otter Tail Company is definitely no exception to this as the corporate yields 2.70% on the present inventory worth, which is kind of a bit larger than the 1.31% yield on the S&P 500 index (SPY). As can also be typically the case with utilities, Otter Tail Company has a protracted historical past of steadily elevating its dividend over time:

Looking for Alpha

This historical past of dividend will increase is one thing that’s fairly engaging, notably in right this moment’s inflationary setting. It’s because inflation is consistently lowering the variety of issues that we are able to buy with the dividend. As such then, the truth that the corporate is giving us a bigger amount of cash yearly helps to offset this impact and keep the buying energy of the dividend within the face of rising costs. Naturally, although, it’s all the time vital that we be certain that the corporate can truly afford the dividend that it pays out. In any case, we don’t want it to be compelled to reverse course and lower the dividend since that will each cut back our incomes and sure trigger the share worth to say no.

The same old approach that we analyze an organization’s capacity to pay its dividend is by its free money circulation. The free money circulation is the amount of cash that’s generated by the corporate’s extraordinary operations that’s left over after it pays all its payments and makes all obligatory capital expenditures. That is the cash that’s accessible to do issues comparable to cut back debt, purchase again inventory, or pay a dividend. Within the fourth quarter of 2021, Otter Tail Company had a unfavourable levered free money circulation of $6.3 million. That is clearly not sufficient to pay any dividend, not to mention the $16.2 million that the corporate truly paid out.

Nonetheless, it’s pretty frequent for utilities to finance their capital expenditures by the issuance of debt and fairness and pay their dividend out of working money circulation. That is largely as a result of extremely excessive price of developing and sustaining utility-grade infrastructure over a large geographic space. Through the fourth quarter, Otter Tail Company had an working money circulation of $76.5 million. That is simply sufficient to cowl the corporate’s dividend with cash left over for different functions. Total then, it does seem that Otter Tail Company’s dividend is kind of sustainable. There doesn’t look like something to fret about right here.

Valuation

It’s all the time vital that we don’t overpay for any asset in our portfolios. It’s because overpaying for any asset is a surefire solution to generate a suboptimal return off that asset. Within the case of a utility like Otter Tail Company, a technique that we are able to worth it’s by wanting on the ahead price-to-earnings ratio. This tells us how a lot we’re paying right this moment for every greenback of earnings that the corporate will generate over the following yr. Total, the decrease the quantity, the higher the worth that the inventory at present has. Thus, after we examine the inventory to that of the peer firms, the corporate with the bottom ahead price-to-earnings might symbolize one of the best worth.

In line with Zacks Funding Analysis, Otter Tail Company at present has a ahead price-to-earnings ratio of 15.63. Right here is how that compares to the corporate’s peer group:

|

Firm |

Ahead Value-to-Earnings |

|

Otter Tail Company |

15.63 |

|

NextEra Power |

29.54 |

|

Exelon Company |

17.76 |

|

DTE Power |

21.23 |

|

CMS Power |

23.02 |

|

AES Company |

14.58 |

As we are able to see right here, Otter Tail Company seems to supply a extra engaging valuation than any of its friends apart from AES Company. Nonetheless, as we noticed earlier in our dialogue in regards to the firm’s monetary construction, AES has a considerably larger debt load so it’s probably cheaper for an excellent motive. Thus, we are able to conclude that Otter Tail is pretty attractively valued relative to its friends.

Conclusion

In conclusion, Otter Tail is a considerably distinctive electrical utility in that it derives a major proportion of its income from actions apart from utility operations. The corporate nonetheless has the identical qualities that buyers have a tendency to understand with utilities, nonetheless, notably their steady money flows. After we mix this with the corporate’s very stable stability sheet and its engaging valuation, we are able to see that the corporate has an awesome deal to supply. Total, buyers might need to take into account this firm for his or her portfolios.