Picture by Rafa Elias/Second by way of Getty Photographs

ON Semiconductor Company or onsemi (NASDAQ:ON) traders who determined to purchase in November after its third-quarter earnings plunge have finished properly, outperforming the S&P 500 (SPX) (SPY) since my earlier replace. I highlighted the capitulation of ON in my November article, arguing why ON’s valuation has normalized from its 2023 highs. Because of this, it appeared rather more engaging, main me so as to add publicity, given the unbelievable dip-buying alternative. Because of this, I upgraded ON, assessing a strong setup for brand new and present traders to choose their spots.

Regardless of that, the preliminary restoration in ON topped out in mid-December 2023, as the continued weak point within the EV and renewable vitality markets probably did not encourage confidence in ON dip-buyers to carry on to their positions. Regardless of that, I assessed onsemi administration and supplied an affordable fourth-quarter earnings commentary. Nevertheless, onsemi’s ahead steering suggests 2024 will probably be one other yr of progress normalization, as its topline progress reached its cycle peak in 2022.

Buyers ought to recall that onsemi achieved This fall income progress of -1% in 2023, according to the broad weak point in its automotive and industrial market segments. These two segments accounted for 80% of its FY23 income base, as onsemi pivots towards capitalizing on the “high-growth megatrends for sustainable ecosystem growth.” Nevertheless, whereas the long-term secular progress themes stay intact, near-term cyclical challenges emerged in late 2023, significantly within the EV business. Given onsemi’s growing publicity, it needs to be clear why traders should be circumspect about their earlier bullish thesis, as ON surged towards its unsustainable July 2023 highs.

Buyers have been additionally probably caught off-guard by the marked shift in sentiments, as even the EV gamers have been shocked by the current weak point. Even the main clear vitality leaders took a major tumble, highlighting the necessity to remind ourselves to respect market cycles.

onsemi’s first-quarter outlook additionally got here in under the earlier analysts’ estimates. Accordingly, the corporate guided to a midpoint income estimate of $1.85B, reflecting “continued softness throughout all finish markets.” Shut followers of onsemi ought to pay attention to the corporate’s market share positive aspects in silicon carbide or SiC. Accordingly, onsemi up to date us that it has attained a 25% market share. Administration believes it may “develop at 2x the market progress in 2024, leveraging buyer ramp-ups in industrial and automotive sectors.”

Furthermore, administration’s commentary signifies that its utilization may backside out within the first half. onsemi highlighted its confidence in sustaining a “gross margin above the mid-40% ground with utilization within the mid-60% vary.” With its utilization dropping to 66%, it is cheap to imagine that we must always have noticed its medium-term backside. The corporate indicated a midpoint gross margin outlook of 45.5% in Q1, down from This fall’s 46.7% metric. Revised analysts’ estimates counsel that the corporate may end 2024 with a gross margin of 45.7%. onsemi indicated that it stays centered on execution in 2024, being attentive to bettering its profitability profile because it digests the continued progress normalization. Accordingly, it anticipates the actions taken to give attention to higher-valued market segments as constructive to rising from the downturn in a greater form.

I assessed that the near-term demand/provide dynamics within the auto chips market may stay unsure. That ought to clarify why ON fell towards its November 2023 lows, down almost 45% from its July 2023 highs. Nevertheless, even the lowered Q1’24 steering did not result in an additional selloff, suggesting that ON probably struck peak pessimism late final yr. Because of this, the market is probably going trying forward, as onsemi stays well-positioned to guide its potential cyclical upswing. Buyers who determine to attend till the coast is evident may proceed lacking out on its ongoing restoration.

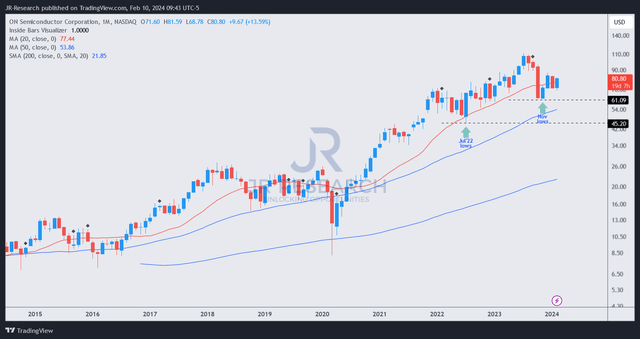

ON worth chart (month-to-month, long-term) (TradingView)

ON’s worth motion clearly signifies its long-term uptrend bias. Dip patrons robustly defended ON’s November 2023 lows on the $61 degree. Whereas the January selloff digested its December positive aspects, the post-This fall earnings restoration means that the market wasn’t unduly involved with the tepid Q1’24 steering.

Because of this, traders are given one other alternative to purchase into ON’s long-term progress thesis earlier than it continues on its uptrend bias towards its 2023 highs. Do not wait till all the excellent news arrives earlier than you make your transfer. By then, you could possibly find yourself chasing the following potential cycle peak.

Score: Preserve Purchase.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a vital hole in our view? Noticed one thing necessary that we did not? Agree or disagree? Remark under with the goal of serving to everybody in the neighborhood to study higher!

{kind=link}