Monty Rakusen

Healthcare REIT Omega Healthcare Traders (NYSE:OHI) could probably be primed for a dividend minimize within the close to future if its funds from operations trajectory would not enhance. The REIT did report in Q3’23 that quite a few operators have fallen behind making funds — whose lease shortfall was utilized in opposition to posted safety deposits — so new payer issues within the fourth quarter may probably endanger the REIT’s dividend. Omega Healthcare’s facility occupancy did enhance within the final two years, nonetheless, however I do not imagine the dividend is as secure as some traders might imagine it’s. Given a rise within the FAD-based payout ratio within the final 12 months, there’s a very actual threat that the healthcare REIT will under-earn its dividend within the close to time period.

Deal with expert nursing portfolio

Healthcare REITs have a quantity of choices to spend money on actual property belongings that profit from rising healthcare spending, together with hospitals, senior housing, medical workplaces or expert nursing properties. The core development for all of those completely different kinds of healthcare investments is the getting old of the worldwide inhabitants. The 65+ inhabitants, primarily based on Aetna projections, is about to develop from 7% in 2000 to 16% by 2050 which creates basic long-term demand progress for healthcare REITs.

Aetna

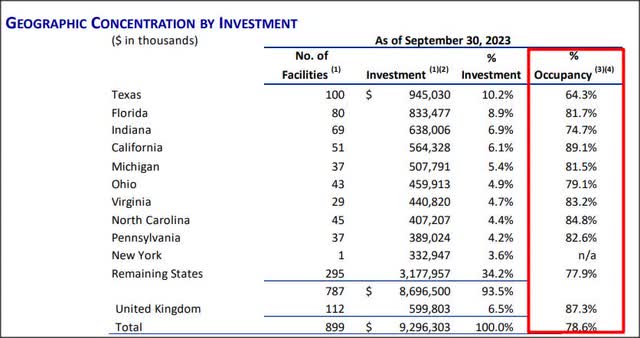

Omega Healthcare Traders is a blended healthcare REIT with a major deal with expert nursing/transitional care operations and a secondary deal with senior housing. As per the newest complement, Omega Healthcare’s portfolio included 899 healthcare properties, 688 of which fell into the first class and 211 into the secondary class, whereas one other 14 belongings have been thought of belongings to be bought.

Omega Healthcare

Omega Healthcare is generally centered on the U.S. market, however has about 111 properties within the U.Okay. From a diversification perspective, I just like the publicity to a non-U.S. market.

Omega Healthcare

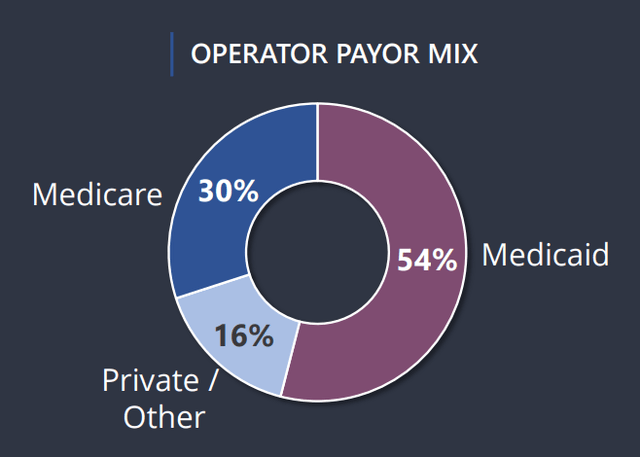

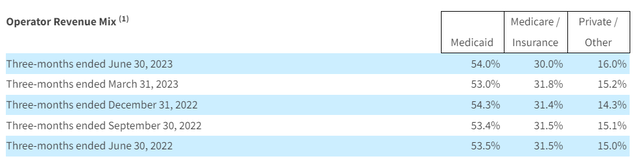

The common dimension of an Omega Healthcare facility represents roughly 100 beds and operators are likely to mainly obtain funds from both Medicare or Medicaid. There’s a small proportion of private-pay beds included in Omega Healthcare’s portfolio, however the operators operating the REIT’s amenities principally rely upon government-funded disbursements to attain revenue. Consequently, these operators usually face predictable money circulate and revenue patterns.

Omega Healthcare

The fee combine has been constant over time with about 15-16% of operator revenues coming from private-pay sufferers whereas the overwhelming majority of revenue comes from Medicaid (54%) and Medicare (30%).

Omega Healthcare

The occupancy price fluctuates wildly throughout amenities. The occupancy price on a portfolio foundation was ~79% as of the September quarter and has been growing. The portfolio has seen a restoration in occupancy within the final two years, particularly because the SNF market recovered from the COVID-19 pandemic. On the finish of FY 2021, the REIT’s portfolio occupancy price was 74% and within the following 12 months 76%, so occupancy charges have improved roughly 2 PP yearly throughout this time.

Omega Healthcare

Operator lease fee delays and asset gross sales translate into shrinking FFO, rising dividend dangers

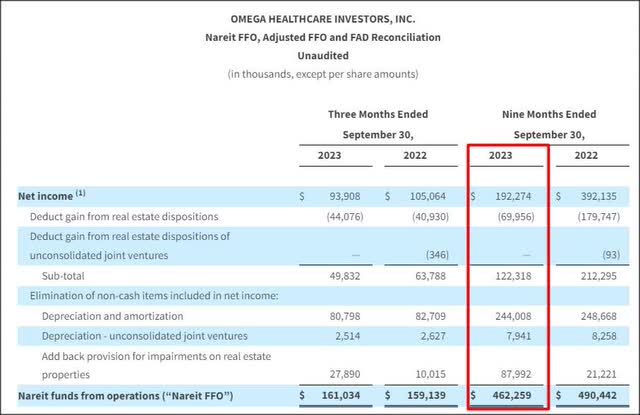

Omega Healthcare didn’t present steerage for FY 2023 when it comes to FFO or AFFO and that is associated to the REIT reporting that some operators haven’t saved up with their lease fee schedules, creating uncertainty round money circulate projections.

Based mostly on the November replace, Omega Healthcare bought seven amenities within the third-quarter that have been leased to LaVie for $84.4 million. LaVie is the third-largest tenant producing about 7.8% of the REIT’s lease/curiosity. Omega Healthcare bought one other 29 amenities leased to LaVie after Q3 quarter-end which can be a sign that fee issues have gotten worse throughout This fall’23.

The REIT additionally disclosed that Maplewood Senior Dwelling — the fourth-largest tenant with a 7.1% lease/curiosity share — short-paid its lease by $1M per 30 days and that Guardian Healthcare did not make its contractual lease funds in August and September as properly.

These and different payer points have resulted in a 6% decline in its FFO within the first 9 months of 2023 to $462M and chances are high that This fall’23 might also see a decline within the REIT’s funds from operations, particularly if new payer issues emerged. New payer points in This fall’23, given Omega Healthcare’s rising payout ratio, may foreshadow a dividend minimize within the close to future, for my part, and make the 9% yield extra dangerous than traders could need to admit.

Omega Healthcare

The FAD-based dividend payout ratio (column on the very proper within the desk under) reveals that the ratio exceeded 100% in Q1’23, however remained fairly near 100% within the two succeeding quarters as properly, leaving solely a really slim margin of error for This fall’23. FAD stands for funds accessible for distribution and is a core metric for healthcare REITs that make dividend funds to their traders.

If Omega Healthcare discloses new fee issues for This fall’23, which isn’t fully unlikely, there’s a good likelihood that the payout ratio will ratio above 100% once more, probably necessitating a dividend minimize. Consequently, because the This fall’23 earnings date approaches, I imagine traders face materials dividend threat.

|

AFFO/share |

Dividend |

Payout Ratio |

FAD |

Payout Ratio |

|

|

This fall’22 |

$0.7271 |

$0.67 |

92.15% |

$0.7040 |

95.17% |

|

Q1’23 |

$0.6571 |

$0.67 |

101.96% |

$0.6046 |

110.82% |

|

Q2’23 |

$0.7445 |

$0.67 |

89.99% |

$0.7023 |

95.40% |

|

Q3’23 |

$0.7118 |

$0.67 |

94.13% |

$0.6784 |

98.76% |

(Supply: Writer)

We now have no FY 2023 steerage for FFO or AFFO, so we may approximate Omega Healthcare’s doubtless money circulate potential by annualizing Q3’23 AFFO… which was $0.71 per share. This calculates to an annualized $2.84 per share in AFFO, a 5% decline relative to FY 2022. Based mostly on annualized AFFO, shares of Omega Healthcare are valued at 10.5X projected ahead AFFO. This valuation implies a 9.5% AFFO yield.

Is Omega Healthcare’s 9% yield costly?

It relies upon. Omega Healthcare pays a 9.0% yield and, at the very least thus far, the dividend is roofed by AFFO. Nonetheless, if OHI have been to under-earn its dividend with AFFO within the close to time period, traders may even see a dividend minimize after which shares impulsively are dearer. Omega Healthcare’s shares traded between 9-12X AFFO within the final 12 months, so traditionally talking, OHI is buying and selling at about its common valuation of the final 12 months. Given the dangers to the dividend, nonetheless, I’d say shares are doubtless leaning a bit on the costly aspect. Given the chance to the dividend, I’d not pay greater than ~9X AFFO for Omega Healthcare at the moment, implying a good worth of ~$26.

Dangers with Omega Healthcare

A brief-term threat is the disclosure of incremental payer issues in This fall’23 which can trigger not solely a collection of inventory downgrades but in addition an extra deterioration within the payout ratio. The development is already not good. New payer points would enormously enhance the possibility of a dividend minimize which I contemplate to be the largest threat for traders. For these causes, traders who actually depend on dividend revenue from their investments could need to keep away from OHI.

Last ideas

Given the development in Omega Healthcare’s FAD payout ratio, there’s a threat that incremental payer issues will lead to an unsustainable dividend payout. The dividend is already not rising, and the dangers to the dividend have clearly elevated. Though occupancy developments have improved within the final two years, Omega Healthcare is probably going primed for a dividend minimize. Given the excessive threat of a dividend minimize at this level, I’d warning in opposition to shopping for Omega Healthcare’s 9.0% dividend yield.

{kind=link}