eclipse_images

Nvidia Company (NASDAQ:NVDA) appears to have sparked a divided fan base – those that cheer for its success and people who are virtually betting on its downfall.

It brings to thoughts the early days of Apple (AAPL) and Tesla (TSLA), the place you both cherished their merchandise and model or had been fervently towards them, leaving little room for middle-ground opinions.

No matter the place you stand on this, it is exhausting to disregard the simple information: Nvidia has been a standout each when it comes to enterprise success and returns.

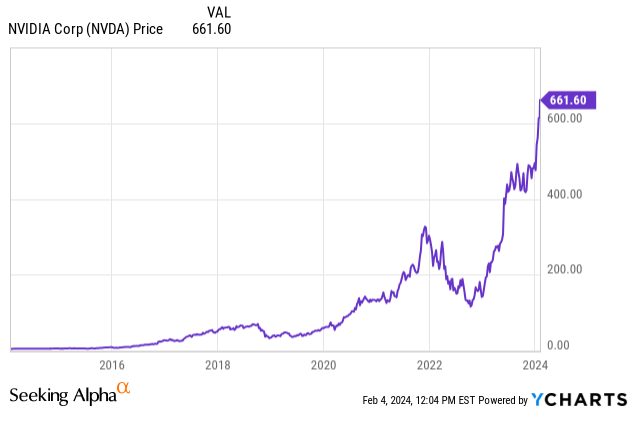

In 2023, it stole the highlight because the top-performing inventory within the S&P 500 (SP500), boasting an eye-popping annual development fee of 237%.

And the momentum did not fizzle out in 2024, with the inventory exhibiting one other spectacular surge of 33.6% in year-to-date returns.

Whether or not you are within the “pro-Nvidia” or “anti-Nvidia” camp, the numbers communicate volumes.

Value Improvement (Searching for Alpha)

Caught up within the buying and selling frenzy or synthetic intelligence (“AI”) FOMO? Maybe.

Nvidia holds the coveted title of being primary AI decide of many and the darling of Wall Road. However delving into the intricacies of its success reveals a narrative past mere value actions.

I wrote an article on Nvidia again in November, “Path to $1,200 by 2030” and in addition put the corporate on “My Prime 3 Inventory Picks For 2024.”

Nevertheless, current earnings experiences and developments have prompted a reassessment of my thesis. The quicker than anticipated AI adoption and Nvidia’s EPS development has pleasantly shocked, making it believable for the goal aim to be reached even earlier, probably by 2027.

Final Protection (Searching for Alpha)

For a extra conservative investor, such a daring prediction may not sit effectively. But, the truth is, regardless of the spectacular inventory value efficiency, Nvidia at present trades at a “mere” blended P/E of 53.6x.

Wanting forward, the inventory seems comparatively low-cost, because of its relentless development trajectory:

- Ahead P/E FY25: 32x its earnings

- Ahead P/E FY26: 27x

- Ahead P/E FY27: 23x.

It is vital to acknowledge that the projected development may not pan out as anticipated. In that state of affairs, Nvidia would not precisely be thought of a discount. Nvidia does have a historical past of untamed value swings, in spite of everything.

However, if AI continues to be the recent subject, we’d simply be gearing up for an additional 12 months of stellar returns.

Enterprise Replace

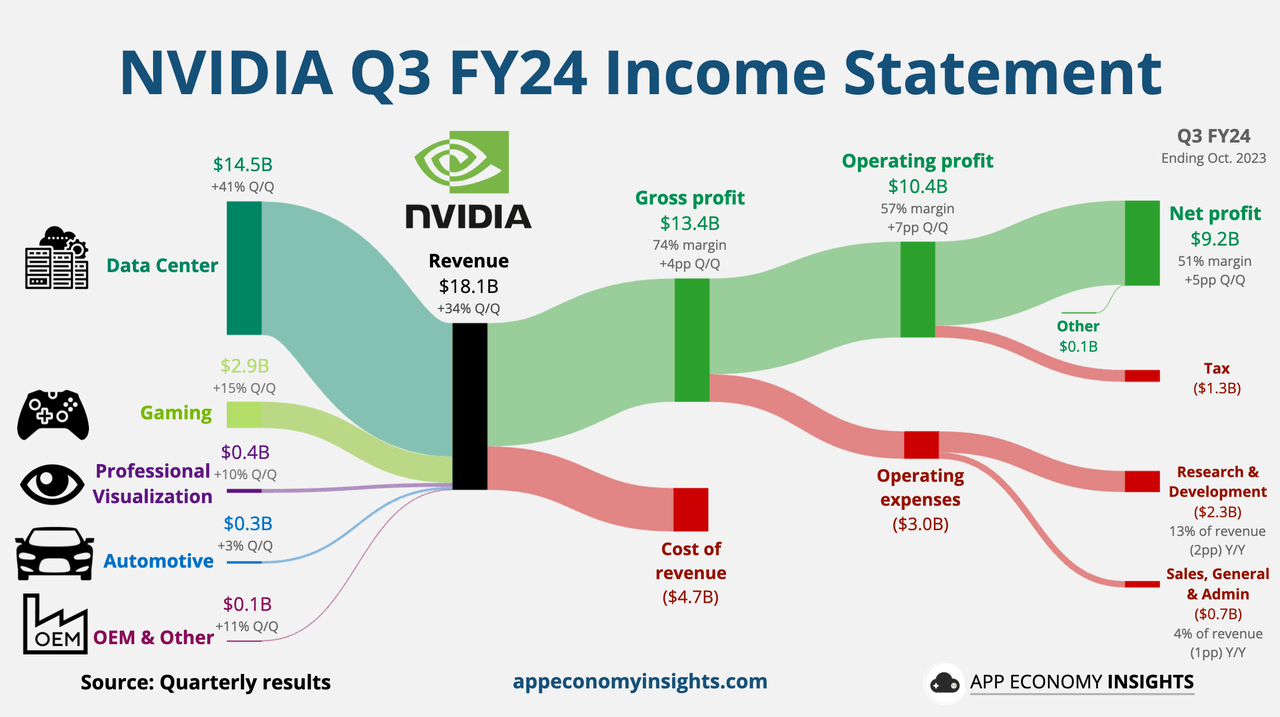

Again in November, when Nvidia unveiled its Q3 FY24 earnings, it marked one more quarter of surpassing expectations on all fronts.

Nvidia achieved a document income of $18.12 billion, exhibiting a outstanding 34% improve from Q2 and an astounding 206% surge from only a 12 months in the past.

The gross margin witnessed a major enchancment, reaching 74% and rising over 2,000 foundation factors because the earlier 12 months. This underscores Nvidia’s present pricing energy, attributed to its superior merchandise.

Working Earnings soared to $10.4 billion, marking a rise of greater than 16x YoY. This sturdy efficiency translated into $9.2 billion in Internet Earnings or $4.02 in diluted EPS, surpassing analysts’ estimates by a major margin of $0.63.

The sturdy development is indicative of the trade’s broader shift from general-purpose to accelerated computing and generative AI.

Nvidia Q3 Earnings (App Economic system Insights)

Nvidia’s CEO, Jensen Huang, is radiating optimism about the way forward for AI. He sees a wave of latest gamers coming into the sphere, past the preliminary wave of enormous language fashions or “LLMs,” client Web firms, and world cloud service suppliers.

Governments and regional cloud service suppliers are investing in AI clouds to cater to native wants. Enterprise software program firms are integrating AI “copilots” and assistants into their platforms. Particular person enterprises are creating customized AI options to automate large-scale industrial processes.

This AI increase is fueling Nvidia’s development throughout varied sectors. Their {hardware} and software program choices, together with GPUs, CPUs, networking options, AI foundry providers, and Nvidia AI Enterprise software program, are all experiencing vital development.

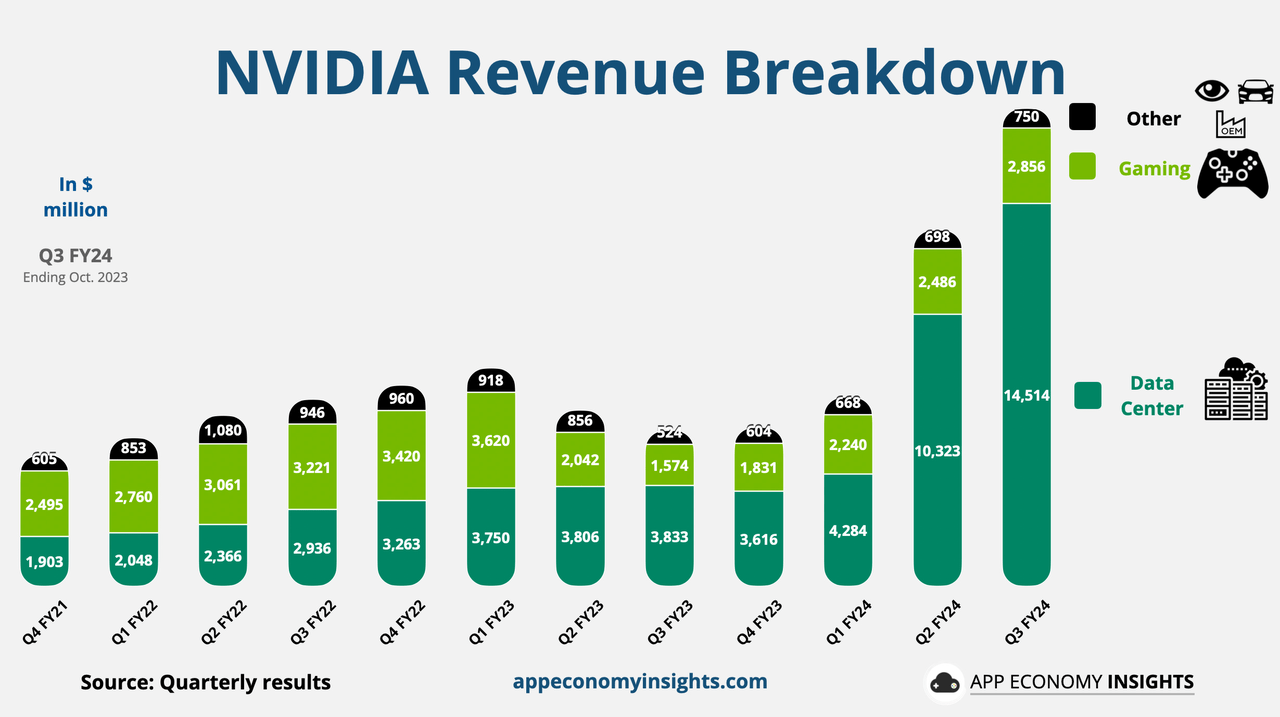

Traditionally identified for powering gaming and crypto mining, Nvidia’s income streams have shifted dramatically. Knowledge heart income now accounts for over 80%, in comparison with 41.3% in Q3 FY22, highlighting the corporate’s transformation and using the trade’s tailwinds.

The NVIDIA HGX platform and InfiniBand networking noticed document income development, solidifying their place as the popular structure for AI supercomputers and knowledge heart infrastructure. Main generative AI purposes like Adobe Firefly, ChatGPT, Microsoft 365 Copilot all depend on Nvidia expertise. Knowledge heart compute income elevated 4x YoY, and networking income grew practically 3x.

With the rising demand, Nvidia is effectively positioned to capitalize on the thrilling alternatives rising on the planet of AI.

Income Breakdown (App Economic system Insights)

AI spending is booming, and that is excellent news for Nvidia. Firms are investing closely in infrastructure for coaching and operating highly effective AI fashions, like LLMs and generative AI purposes. This demand is fueling robust development for Nvidia’s accelerated computing options.

Each client Web firms and conventional companies are driving this development. In actual fact, practically half of Nvidia’s current knowledge heart income got here from these two sectors. Firms like Meta Platforms (META) are utilizing AI for every little thing from deep studying and suggestion programs to optimizing advertising supplies with generative AI. And this pattern is barely anticipated to proceed, with an increasing number of main gamers leaping on the AI bandwagon.

The wave of AI adoption is not simply restricted to massive client names. Even software program firms like Adobe (ADBE), Snowflake (SNOW), and ServiceNow (NOW) are integrating AI “copilots” and AI-powered options into their platforms. This reveals a broader shift in direction of AI-driven options throughout varied industries.

Nvidia is not the one participant within the recreation, although. Rivals like AMD (AMD), Intel (INTC), and cloud suppliers like Amazon (AMZN) and Google (GOOGL) are all creating their very own AI {hardware} choices which might current a problem to Nvidia’s development.

Because the AI enterprise proves profitable, the fierce competitors might finally problem Nvidia’s present undisputed superiority. To compete, AMD has launched the Intuition MI300X accelerator and the Intuition M1300A accelerated processing unit, which the corporate claims work to coach and run LLMs.

To remain forward, Nvidia is planning to launch new merchandise even quicker to cater to the various wants of the rising AI market.

There have been some challenges, like current U.S. export restrictions concentrating on China. These initially raised considerations a few potential impression on Nvidia’s gross sales, however the firm has tailored by launching a modified chip that complies with the rules.

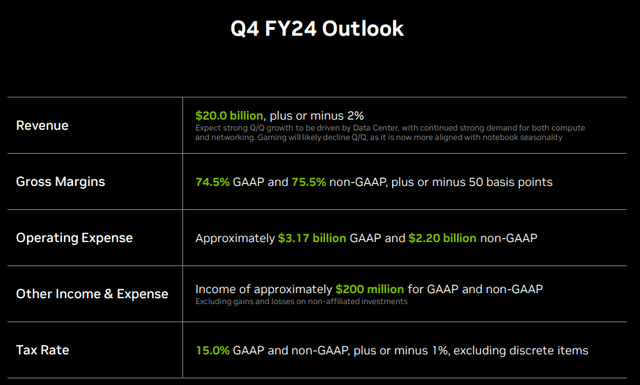

Regardless of these hurdles, Nvidia is anticipating one other record-breaking quarter with $20 billion in income. Their robust product portfolio and pricing energy maintain their gross margins at historic excessive ranges, solidifying their place as a frontrunner within the accelerated computing market.

This fall Outlook (NVDA IR)

Valuation

Given the spectacular 2023 return of 237% and a year-to-date 2024 return of 33.6%, one may assume that Nvidia’s valuation is reaching sky-high ranges.

I urge to vary.

Certain, Nvidia operates within the unpredictable semiconductor trade, the place inventory actions comply with the swings of financial cycles, between durations of euphoria and peak pessimism pushed by underlying demand.

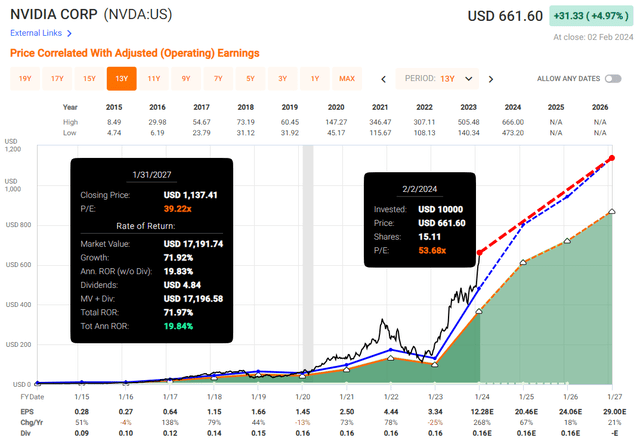

Curiously, Nvidia’s present valuation, at 53.7x its blended P/E, is traditionally decrease than some cases up to now.

Through the peak buying and selling frenzy of 2021, the inventory soared to a whopping 81.4x its earnings.

Evaluating it to its historic common of 33.9x since 2003, immediately’s valuation appears considerably elevated. Nevertheless, it is essential to think about development for a extra nuanced perspective.

Over time, Nvidia has seen a median annual EPS development of 26.4% since 2003. However within the final 4 years, that development has accelerated to a formidable 53.4% yearly.

The expectation, based on analysts polled by S&P World, is for this accelerated development pattern to persist:

- FY25: EPS of $20.46E, YoY development of 67%

- FY26: EPS of $24.06E, YoY development of 18%

- FY27: EPS of $29.00E, YoY development of 21%.

This additionally implies that Nvidia’s Ahead PEG for FY25 is at present 0.8. That is very favorable, contemplating that the valuations are stretched in comparison with different mega-cap tech companies.

- Apple’s Ahead PEG: 2.96

- Microsoft’s (MSFT) Ahead PEG: 2.85.

After all, if the expansion doesn’t materialize, the inventory may very well be closely punished, as we witnessed in 2022 when it plummeted to a low of $108 from its earlier peak of $346 through the COVID-driven buying and selling frenzy, marking a major 70% decline.

Nevertheless, I’m within the camp of people that consider in and actively use AI at my work. I believe will probably be the following leg as much as drive the economic system and permit us to enter instances of unprecedented productiveness. Subsequently, Nvidia is in the correct place on the proper time with the correct product.

If we glance into the long run valuation, the inventory is dear in any respect:

- Ahead P/E FY25: 32x its earnings

- Ahead P/E FY26: 27x

- Ahead P/E FY27: 23x.

Having stated that, in my view, regardless of its robust efficiency, Nvidia stays a discount immediately. Shopping for now might doubtlessly unlock returns of round 20% yearly till 2027, at the same time as I anticipate the valuation to contract to round 39x its earnings by that point.

Assuming the EPS development past 2027 stays round 20% yearly, we might see a inventory value above $2,000 by 2030.

Valuation (Quick Graphs)

Takeaway

Nvidia has been having fun with a outstanding run in current instances, topping the charts because the best-performing inventory of S&P 500 in 2023 and already up over 30% in 2024. This surge is basically fueled by the booming AI trade, which is driving vital development throughout varied sectors for Nvidia.

The corporate’s {hardware} and software program choices are experiencing a surge in demand, because of a number of components. Regional cloud service suppliers are investing in AI clouds to cater to native wants, whereas enterprise software program firms are integrating AI “copilots” and assistants into their platforms. Moreover, particular person enterprises are creating customized AI options to automate large-scale industrial processes.

This surge in AI spending interprets to excellent news for Nvidia. Firms are closely investing in infrastructure for coaching and operating highly effective AI fashions, comparable to massive language fashions and generative AI purposes. Whereas some may dismiss AI as mere hype, the rising CapEx by firms to remain related and drive innovation demonstrates its tangible impression.

At the moment, Nvidia’s inventory is buying and selling at a valuation above its historic requirements. Nevertheless, contemplating the anticipated EPS development over the following three years, if it materializes, the valuation will considerably drop, beneath 23x its earnings by 2027. I’m betting it is going to ship double-digit returns for traders prepared to embrace the potential.

{kind=link}