")

[ad_1]

stockelements/iStock Editorial by way of Getty Photos

Many American traders are targeted on the earnings their holdings would possibly present. Some need present earnings; others need future earnings. The previous are likely to deal with buying shares in corporations or funds with larger yields. What constitutes a excessive yield can depend upon the investor. Some have a look at 4% as a comparatively excessive yield. Others attempt to lock in yields of 8%, 10% or larger.

There are different traders who deal with dividend progress. More often than not, dividend progress shares have decrease yields with a dividend that grows over time. Continuously, decrease yielding shares can afford to develop their dividends at a fee that exceeds 10% yearly. One such firm that I personal is Lowe’s (LOW). This inventory yields round 2%, however over the previous a number of years, the dividend fee has doubled roughly each 4 years, give or take.

One other firm that matches into the latter group can be Nike (NYSE:NKE). This firm has a protracted observe report, and it is grown its dividend rapidly lately. I can keep in mind my grandparents shopping for me a pair of Nikes earlier than Air Jordans had been widespread. As soon as Michael Jordan signed on, Nike grew to become an iconic model. The “swoosh” emblem is thought all through the globe, and the corporate sells footwear, athletic attire, and gear to brand-conscious shoppers. Along with promoting the Nike model, the much more conventional basketball model Converse (assume Larry Chook and Magic Johnson) is owned by NKE.

The corporate’s inventory additionally has a powerful observe report. Buyers in Nike have accomplished properly over the long term, and the corporate isn’t more likely to go away anytime quickly. Nevertheless, simply because an organization has had a powerful observe report, it doesn’t essentially make sense for an investor who is targeted on earnings to buy its inventory.

Nike’s Dividend Progress

The dividend progress report of Nike is robust. The corporate has grown its dividend yearly since 2004. Whereas this isn’t a powerful as another corporations like Johnson & Johnson (JNJ) or McDonald’s (MCD) which have a dividend progress report of fifty years or extra, it is nonetheless continued by means of a few main recessions and a worldwide pandemic.

Not solely has the dividend grown, it is grown fairly quickly. Over the previous 5 years, NKE has grown its dividend 11.14% per 12 months. This fee would result in the doubling of the dividend in a bit of greater than six years.

It’s seemingly that NKE can proceed elevating its dividend at a wholesome fee within the close to future. The payout ratio for many of the previous decade has been round a 3rd of earnings. There have been a few outliers, however these years solely had a payout ratio within the 60% vary. A decrease payout ratio typically corresponds with a secure dividend that permits for future raises, and Nike suits the invoice.

The yield, even with this sturdy report of progress, is kind of low, nonetheless. The present yield is just one.07%, which is properly beneath the yield provided by the S&P 500 as an entire. These on the lookout for present earnings together with sturdy dividend progress can discover different choices that might seemingly work higher.

Monetary Overview

Over the previous ten years, Nike has almost doubled its income, going from $25.3 billion to $46.7 over that time period. The latest quarterly report confirmed a 17% enhance in income on a year-over-year foundation. Nevertheless, the corporate famous that its gross margin decreased due to larger markdowns supposed to liquidate stock. Present inventories had been really up 43% over the prior years as provide chains improved as pandemic restrictions eased. This stock will have to be offered, however with the latest enhance in gross sales, it stays to be seen how rapidly Nike can flip it round.

Web earnings has greater than doubled over the previous decade, as have earnings per share, from $2.472 billion to $6.046 billion and $1.34 (diluted) to $3.75, respectively. The corporate paid down a bit of little bit of its debt over the previous annual report, as properly, bettering its monetary place. As of the Could 2022 annual report, the corporate owed $12.722 billion. Primarily based upon latest gross sales numbers, this shouldn’t be a very regarding degree of debt.

One issue that would bode properly for NKE shareholder returns is a brand new share repurchase program. The corporate authorised an $18 billion buyback. The corporate has lower its share rely by about 1/9 over the previous ten years, and this newest buyback program might lower barely greater than 9% from the present variety of shares excellent, based mostly upon the corporate’s present market cap.

Evaluation

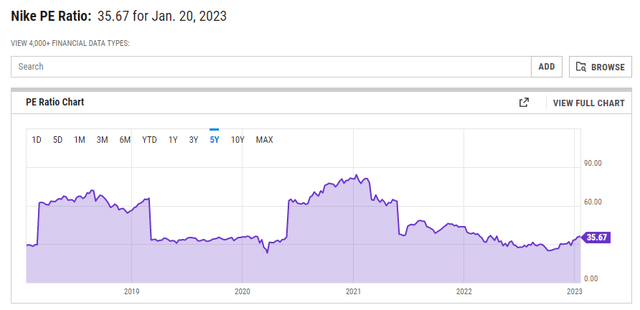

Whereas the dividend yield is low, Nike remains to be an excellent firm with strong financials and a rising dividend. It is value holding in a portfolio. Nevertheless, I’m not prepared to begin a place at present ranges. The present worth of $126.62 (as of January 21, 2023) corresponds to a PE ratio of almost 36. Whereas that is pretty regular when wanting on the final 5 years, there have been a couple of alternatives to buy shares at a lower cost.

Nike PE ratio (YCharts)

Most lately, shares fell as little as $83 a share on the finish of September 2022. This may have been a chief shopping for alternative. The worth has elevated by about 50% in lower than 4 months. Such fast progress isn’t actually sustainable for the long run.

Moreover, if the priority over a recession turns into a actuality, client discretionary shares like Nike might get hit as folks cease spending as a lot as they could in any other case spend. This might present a greater entry worth and dividend yield, even when the PE ratio is larger. If the financial system recovers comparatively rapidly, those that maintain off on buying till the value drops may benefit fairly a bit. At this worth and this yield, I am not more likely to be a purchaser, but when I held the inventory, I would proceed to take action.

[ad_2]

Source link