WANAN YOSSINGKUM

Overview

Following 4Q22 earnings, I consider it’s best to carry lengthy positions regardless of potential short-term weak spot (place sizing is essential right here). With dominant merchandise within the profitable index knowledge area and the brand new ESG info trade, MSCI (NYSE:MSCI) is, in my view, a confirmed high-growth compounder. The agency is extensively considered the trade commonplace in terms of establishing and sustaining worldwide fairness indices and serving as a benchmark for these indices. To high all of it off, they’re the trade commonplace in terms of ESG indices, knowledge, and analysis.

Income and EPS for MSCI’s fourth quarter had been each larger than anticipated, contributing to the agency’s total wholesome outcomes. I consider that the low double-digit development in subscription run fee is a mirrored image of the benefits supplied by MSCI’s recurring income streams and the secular tailwinds supplied by the rising complexities of portfolio development. Extra importantly, I feel the corporate is doing a superb job of sustaining development and innovation investments whereas additionally implementing cost-cutting measures from their downturn playbook. Nevertheless, the Analytics retention fee dropping and the ESG income development slowing from the earlier quarters are each early warning indicators that MSCI’s subscription revenues could also be softening. Additionally, the asset-based charges that make up 22% of MSCI’s whole run fee fell by double digits. As such, it’s essential to appropriately dimension the place in order that one can improve its dimension if MSCI had been to fall.

Earnings replace

The 4.8% development in income (6.8% organically) to $576.2 million was higher than the three.4% development anticipated by consensus. The natural development fee for Index revenues was 0.4%, whereas the expansion fee for Analytics revenues was 9.5%. Each ESG & Local weather and Non-public Belongings noticed spectacular natural development, with the previous exhibiting a 43.0% improve and the latter a 13.8% improve. Complete subscriptions elevated by 11.9%, whereas asset-based charges decreased by 12.7% in run fee. Because of implementing the downturn playbook and realizing working leverage, EBITDA margins elevated by 80 foundation factors to 58.8%. The $2.84 EPS was larger than the anticipated $2.76.

The nice

On condition that MSCI’s subscription run fee income (which accounts for 78% of whole) grew by 12% in 4Q, it’s secure to say that the corporate has confirmed its resilience within the face of a difficult macro surroundings. This, I consider, is a mirrored image of MSCI’s enduring enterprise mannequin and the secular tailwinds related to the rising issue of portfolio administration. That stated, I would not need to draw any agency conclusions concerning the future from the present sturdy efficiency. The buy-demand aspect’s for portfolio development and analysis instruments has been regular as measured by the subscription run fee, however this may occasionally change if market volatility persists into the foreseeable future. Administration did observe that extended market declines (a number of quarters) are likely to lead to longer gross sales cycles and elevated cancellations attributable to fund closures, mergers, and employees reductions.

Moreover noteworthy is the truth that natural subscription income development within the Index section reached 12% 12 months over 12 months attributable to investor demand for customized indices, and that natural income development in ESG & Local weather remained at 40%+ 12 months over 12 months attributable to sturdy adoption of Local weather options. Moreover, MSCI retention charges remained at very wholesome ranges, at 93%, albeit with a slight lower from 4Q21’s 94.4%. Furthermore, futures and choices volatility-related revenues, which accounted for 29% of MSCI’s whole income in 4Q22 because of a rise of 31.5 million contracts traded, supplied a partial hedge for the corporate’s asset-based charges.

MSCI is implementing cost-cutting measures from its “downturn playbook” in response to the present macroeconomic local weather. Such cuts embrace measures comparable to halting new hires, reducing again on skilled charges, reducing again on journey prices, and reevaluating incentive pay. All of those, in my view, would assist MSCI meet its long-term objective of excessive EBITDA margins this 12 months (FY23). The cash saved via this technique can then be reinvested by administration into the corporate for development sooner or later. As a matter of reality, in 2023 MSCI intends to extend its funding spending, greater than doubling its total expense development, to pursue development alternatives. Nonetheless, administration is cognizant of the market state of affairs and would reduce funding spending in a extreme or extended market downturn.

The unhealthy

Subsequent, the elements that left me feeling lower than thrilled. As AUM dropped throughout the quarter, so did the asset-based payment run fee. Given the persevering with near-term market uncertainty, I count on this decline to proceed. The fourth quarter’s 5% run fee development in Analytics was comparatively gradual, and in addition the retention fee fell to 90.0% from 93.4% within the prior 12 months’s fourth quarter attributable to giant shopper cancellations. Moreover, the expansion of ESG income has slowed in latest quarters attributable to challenges posed by the present financial surroundings, longer gross sales processes, and an absence of huge offers, indicating that the corporate is prone to macroeconomic components.

Partnership with Google and Microsoft

Information ingestion is on the coronary heart of MSCI and Google’s (GOOG)(GOOGL) new cloud partnership. The partnership was conceived by higher administration as a complement to, moderately than a alternative for, Microsoft (MSFT) Azure in powering the corporate’s technological enablement. In response to my analysis, MSCI makes use of Azure for supporting knowledge processing and product growth, Google Cloud to help in knowledge assortment and the creation of latest knowledge units, and Snowflake (SNOW) to help within the environment friendly distribution of content material to purchasers. Due to this fact, I contemplate this new partnership to be an train in “diversification” and a way of enhancing all the know-how stack.

The steerage

MSCI has launched steerage for FY23 working bills within the vary of $1.09–1.130 billion, EBITDA bills within the vary of $965–$995 million, and FCF within the vary of $1.06–$1.12 billion. The corporate’s preliminary 2023 outlook signifies spectacular working leverage, regardless that MSCI doesn’t present steerage on income, adjusted EBITDA, or adj. EPS. On condition that in FY22, subscriptions accounted for 74% of MSCI’s whole income. Beneath the idea that subscription income grows on the identical charges because it has this quarter in 2023, all else being equal, this might suggest a development of close to 10% in FY23, which is larger than the guided bills development.

Valuation

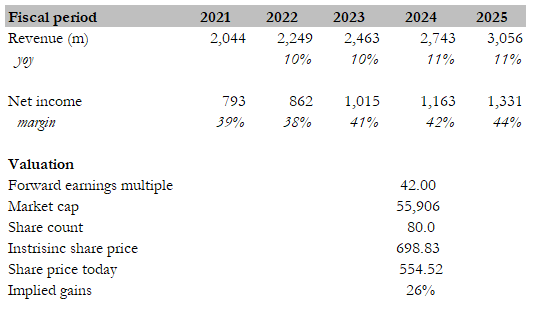

I consider MSCI is price ~$700/share based mostly on my mannequin and consensus figures. The expansion expectation right here is comparatively steady given the character of the enterprise. Nevertheless, I count on margins to increase steadily as MSCI profit from working leverage and scale. Additionally given the prime quality nature of this enterprise, I consider the comparatively excessive valuation, on an absolute foundation, is justified.

Writer’s estimates

Danger

Depending on fairness market

A decline in fairness markets has a detrimental impact on MSCI’s backside line. The impression on EBITDA, EPS, and free money movement is exacerbated as a result of these charges are incurred by the corporate’s Index division, which has margins of 75% or extra. MSCI has a plan in place to cope with market downturns, together with each automated and proactive measures. However the MSCI inventory reacts positively (when fairness markets are excessive) and negatively (when they’re low). I count on sturdy inflows into worldwide equities and ESG funds to contribute to the MSCI inventory’s outperformance.

Conclusion

I consider that regardless of short-term weak spot, it’s best to carry lengthy positions in MSCI attributable to its dominant merchandise within the index knowledge and ESG info industries, that are seen as high-growth alternatives. The agency’s 4Q22 earnings confirmed higher-than-expected income and EPS, however early warning indicators of softening subscription revenues and declining asset-based charges could point out a slowdown. I might recommend being cautious with place sizing to benefit from potential worth drops.

{kind=link}