Printed on April fifteenth, 2026 by Nathan Parsh

Diversified Royalty Company (BEVFF) has two interesting funding traits:

#1: It’s a excessive yield inventory primarily based on its 6.7% dividend yield.

Associated: Checklist of 5%+ yielding shares.

#2: It pays dividends month-to-month as a substitute of quarterly.

Associated: Checklist of month-to-month dividend shares.

You possibly can obtain our full Excel spreadsheet of all 118 month-to-month dividend shares (together with metrics that matter like dividend yield and payout ratio) by clicking on the hyperlink under:

Diversified Royalty Company’s above traits, particularly its excessive yield and month-to-month dividend funds, make it a horny candidate for income-oriented traders.

However there’s extra to the corporate than simply these components. Hold studying this text to be taught extra about Diversified Royalty Company.

Enterprise Overview

Diversified Royalty Company, primarily based in Canada, is a multi-royalty company that acquires royalties from multi-location companies and franchisors in North America. The corporate owns the emblems of Mr. Lube, AIR MILES, Sutton, Mr. Mikes, Nurse Subsequent Door, and Oxford Studying Facilities.

The corporate, previously referred to as BENEV Capital, modified its title to Diversified Royalty Company in September 2014. Its goal is to accumulate predictable, rising royalty streams from various multi-location companies and franchisors.

Diversified Royalty Company has been constructing a diversified portfolio of royalties from multi-locations and franchisors in Canada. It additionally intends to increase its enterprise mannequin within the U.S. To this finish, the corporate has been selling its enterprise mannequin at varied Worldwide Franchise Affiliation occasions within the U.S. Its growth efforts bore fruit with Stratus, the corporate’s first royalty transaction within the U.S.

Stratus is an industry-leading franchisor in industrial cleansing and constructing upkeep, providing each grasp franchises and turn-key janitorial unit franchisees throughout North America. The worldwide industrial cleansing {industry} is immense and grew by 5.8% yearly between 2015 and 2022. It’s anticipated to develop 6.4% per 12 months from 2025 to 2030.

Supply: Investor Relations

Development Prospects

Diversified Royalty Company has exhibited a considerably risky and inconsistent efficiency report, partly because of the impact of the gyrations of the change fee between the Canadian greenback and the U.S. greenback. Nonetheless, the corporate has grown its common earnings-per-share by 9.6% yearly, from $0.07 in 2016 to $0.15 in 2025. Nevertheless, this progress fee has deaccleretered to 0% when taking a look at simply the final 5 years.

Diversified Royalty Company has made a number of acquisitions with the intention to assist develop the enterprise.

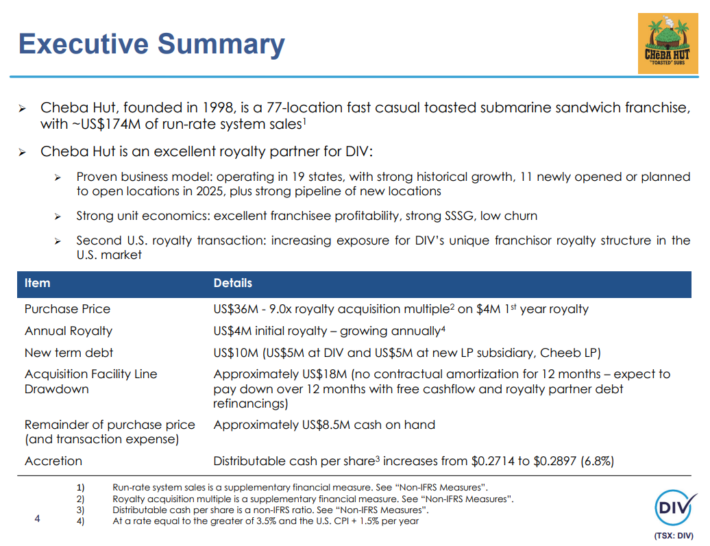

In 2022, the corporate made a royalty acquisition of Stratus that has confirmed to be a big progress driver for the corporate. Stratus expects to have as much as 150 Grasp Franchisees throughout the U.S. and Canada over the subsequent 5-10 years.

Extra not too long ago, the corporate added Cheba Hut in 2025.

Supply: Investor Presentation

Given Diversified Royalty Company’s historic progress report and anticipated enterprise acceleration due to acquisitions, we anticipate 1.0% common annual progress of earnings per share over the subsequent 5 years.

Dividend & Valuation Evaluation

In distinction to many corporations that reduce their dividends in 2020-2021 because of the coronavirus disaster, Diversified Royalty Company defended its dividend throughout that downturn. As well as, the corporate’s dividend has a compound annual progress fee of 5.6% over the past 5 years.

Nevertheless, it’s important to notice that the corporate has stored its dividend unchanged for a lot of the final decade. Throughout this era, it has marginally raised its dividend in CAD a number of instances, however the strengthening of the USD versus CAD has offset these raises.

Furthermore, Diversified Royalty Company typically has a proforma payout ratio of 100%, which may be very excessive. The anticipated payout ratio for 2026 is even increased at 140%. Total, because of the remarkably excessive payout ratio and the fabric debt load of Diversified Royalty Company, the dividend has a skinny margin of security and could also be reduce at any time when the subsequent recession happens.

In reference to the valuation, Diversified Royalty Company is buying and selling for 20.9x anticipated EPS for the 12 months. Given the corporate’s first rate progress prospects, we assume a good price-to-earnings ratio of 15.0 for the inventory. Subsequently, the present price-to-earnings ratio is way increased than our assumed honest price-to-earnings ratio. Subsequently, complete annual returns may very well be decreased by 6.4% by 2031 as a result of a number of compression.

Considering the 1% annual progress of earnings per share, the 6.7% dividend, and a 6.4% annualized headwind from valuation, Diversified Royalty Company might supply a 1.9% common annual complete return over the subsequent 5 years. This can be a pretty low fee of potential return.

Remaining Ideas

Diversified Royalty Company has a horny enterprise mannequin. It does its finest so as to add dependable and rising royalty revenues to its earnings stream, aiming to supply a rising earnings stream to its shareholders.

Furthermore, the corporate has first rate progress prospects forward because it makes use of acquisitions to develop its enterprise.

The primary caveats are Diversified Royalty Company’s sensitivity to recessions and really excessive dividend payout ratio. Moreover, the inventory has exceptionally low buying and selling quantity (lower than 8,000 shares traded most days), which makes it arduous to buy or promote a big place on this inventory.

Whereas the dividend yield is enticing, complete return prospects are low, incomes shares of Diversified Royalty Company a maintain ranking.

Don’t miss the sources under for extra month-to-month dividend inventory investing analysis.

And see the sources under for extra compelling funding concepts for dividend progress shares and/or high-yield funding securities.

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}