Robert Manner

Funding thesis

The story of Moncler (OTCPK:MONRY) (OTCPK:MONRF) is an enchanting story of evolution that has taken this firm from its humble beginnings in France in 1952 as a producer of high-quality cold-weather clothes to its present standing as an Italian semi-luxury model. This exceptional transformation skilled a pivotal turning level in 2003 when the visionary entrepreneur Remo Ruffini acquired the corporate and utterly revamped its technique and route.

My funding thesis in Moncler is grounded in the truth that we’re nonetheless within the midst of this transition from a premium clothes model to a luxurious model, and as traders, we will capitalize on this course of. On this article, I’ll try to clarify why I imagine Moncler has the potential to determine itself as one of many main luxurious manufacturers, and the advantages this might deliver each to the corporate and traders. Moreover, given the latest declines within the sector, we could also be introduced with an intriguing shopping for alternative, so I’ll endeavor to conduct a valuation to find out a goal buy value.

What units aside a luxurious model from a premium model?

This can be a difficult query to reply, however it’s essential when analyzing a luxurious sector firm. From my standpoint, a luxurious model is one through which its prospects have such excessive buying energy that even throughout a recession, they will nonetheless comfortably purchase their merchandise and may settle for periodic value will increase. In distinction, a premium model is delicate to financial cycles, and value will increase are restricted attributable to a extra elastic demand. I imagine that an instance makes this a lot clearer; A luxurious model, for my part, can be Hermes or Christian Dior, whereas a premium model is likely to be Michael Kors-.

I feel the benefits of being a luxurious model are clear, however what does an organization want to achieve this standing? For my part, it’s essential for the general public to understand it as unique and never inside everybody’s attain. Needless to say the aim of those merchandise is exactly to permit high-level customers to distinguish themselves from the remaining. To realize this aim, I imagine there are three basic elements that Moncler is dealing with very nicely: historical past, advertising and expertise.

Historical past

Historical past is essential for all these manufacturers as a result of the longer you have been available in the market, the extra you have been capable of set up your self within the minds of customers, and the extra recognizable your model turns into. Simply take a look at the years when manufacturers like Hermes (1837) or Louis Vuitton (1854) have been based. Moncler was established in 1952 as a producer of cold-weather clothes. Right now, they’ve efficiently positioned their flagship product, cold-weather jackets, within the minds of all customers. While you consider luxurious jackets, you consider Moncler, and this might have been not possible to attain with out their roots as a producer of those merchandise and greater than 70 years of cultivating this model picture.

monclergroup.com

Advertising and marketing

On the planet of luxurious, advertising is not the identical as in shopper markets. It isn’t about having your model in all places however about having it in the best locations. For example, it is not about seeing the LV model on tv on daily basis, however about presenting it in unique settings, like on the World Cup remaining or the Monaco Grand Prix, the place the trophy arrives in a custom-designed field.

On this regard, Moncler is doing what I take into account a wonderful job. They’ve organized top-tier occasions with influential figures within the vogue world, similar to Pharrell Williams and Lewis Hamilton. The thought is to steadily elevate the model’s standing by way of this extra selective advertising strategy, centered on enhancing the notion of exclusivity.

Expertise

Other than efficient advertising, offering an distinctive buyer expertise is essential for a luxurious model. This encompasses all the pieces from the second a buyer steps into the shop to post-sales service. Moncler excels on this facet. Their shops are positioned in prime metropolis areas and boast gorgeous designs. Throughout the shopping for course of, a devoted salesperson is all the time obtainable to help and meet your wants. After the acquisition, you may instantly contact their gross sales crew for inquiries, info on future occasions, or to schedule appointments within the retailer. All of this elevates the model’s notion amongst prospects, making them extra prepared to spend money on their merchandise.

Luxurious Retail Journal

The transition from a premium model to a luxurious model takes many years of profitable execution, and the problem is immense. Nevertheless, the reward on the finish of the journey is nicely value it. Moncler is executing their technique accurately and has a transparent aim. Because of this, I belief that over time, they’ll be capable of enhance the worth of their manufacturers and full this transition. Now, let’s examine how all this basic evaluation has translated into concrete numbers.

Earnings assertion

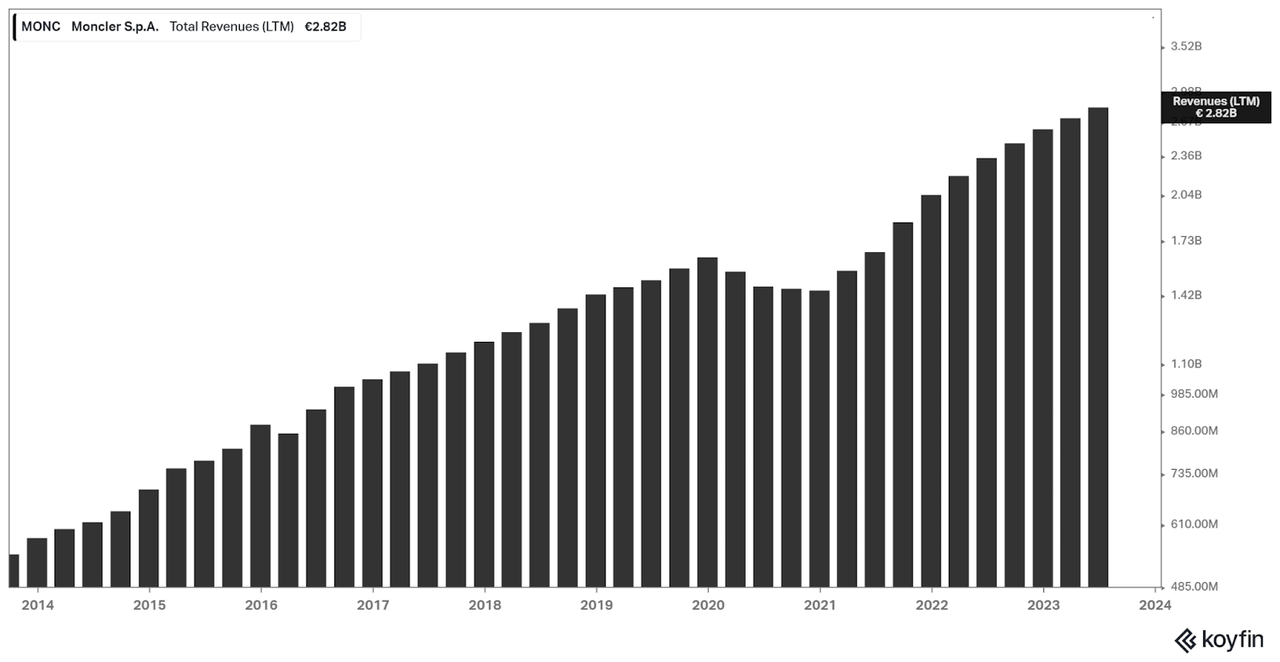

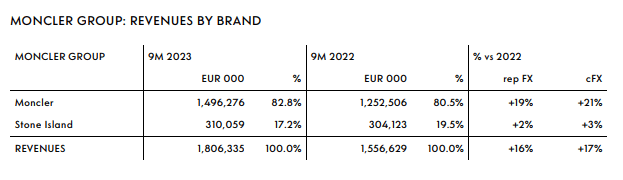

Earlier than delving into the numbers, it is essential to notice that Moncler not too long ago acquired the model Stone Island. We are going to talk about this acquisition in additional element shortly, however for now, it is essential to grasp that it presently accounts for 15% of the corporate’s revenues. As seen within the following chart, the corporate’s complete revenues have surged from 610 million euros in 2014 to 2,820 million euros in 2023, representing a exceptional compound annual development charge of 18%.

Moncler Income (Koyfin)

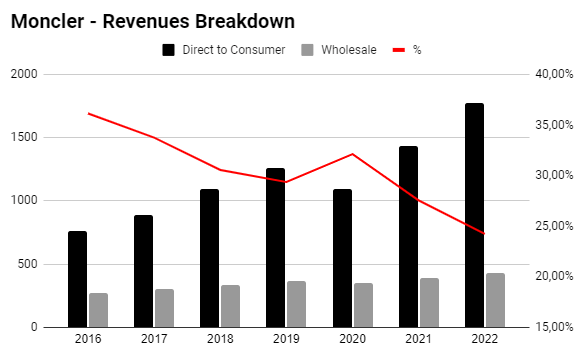

One thing essential to notice is that Moncler sells its merchandise in two alternative ways: firstly, by way of multi-brand shops, and secondly, in its personal retail shops. Making an allowance for all the pieces we mentioned earlier, it’s much more advantageous to promote merchandise in your personal shops to keep up full management over the shopper expertise, with the final word aim of enhancing model notion. In actual fact, the foremost luxurious manufacturers completely promote by way of all these shops, utterly eschewing multi-brand retailers.

Moncler, attributable to its considerably decrease standing, is just not but able to promoting everything of its merchandise by way of its personal shops. Nevertheless, it is essential to watch the development on this information. This development is very favorable in Moncler’s case, as the proportion of gross sales by way of multi-brands shops has decreased from representing 38% of gross sales in 2016 to solely 25% previously 12 months.

As you may see, Moncler’s technique is centered on elevating the model’s worth, and all choices made by the administration are oriented on this route. Promoting nearly all of their merchandise by way of their very own means is only one extra methodology to attain their long-term aim, serving as one other instance of the efficient execution of their technique.

Moncler Income Breakdown (self-made)

Capital allocation

Capital allocation is a key facet for a corporation’s long-term development, and undoubtedly, it is likely one of the factors to which I pay essentially the most consideration when analyzing an organization. On this regard, Moncler and its administration, led by Remo Ruffini, appear to be doing a spectacular job.

At the start, natural development of the Moncler model is of utmost significance. To realize this, they spare no expense on advertising and occasions, as now we have beforehand mentioned on this evaluation. Within the brief time period, revenue margins may very well be increased by decreasing this funding. Nevertheless, in the long run, the return on this funding far exceeds the present one-time value. I respect that the administration understands and applies this technique.

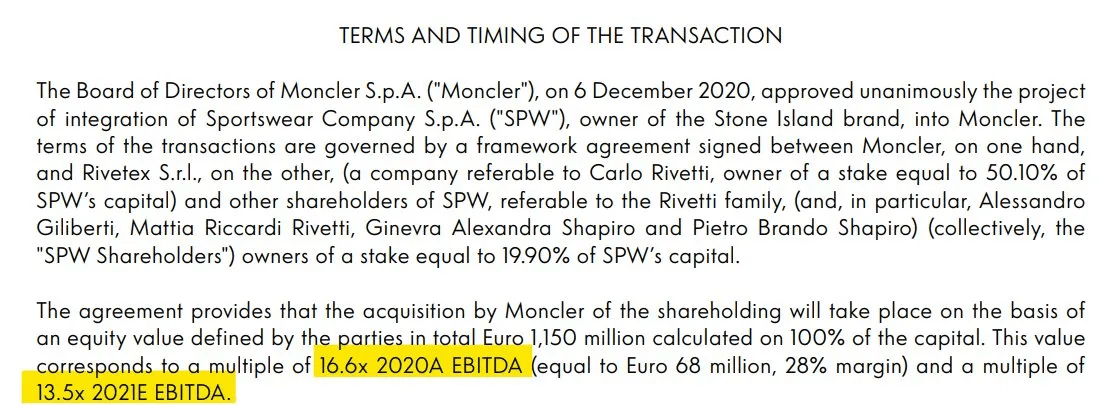

Inorganic development is just not a pillar for the corporate’s growth. They’ve solely accomplished one acquisition of their historical past, that of Stone Island, as talked about earlier. Nonetheless, regardless of their restricted expertise in acquisitions, I imagine that this buy was a masterstroke on Moncler’s half. Let’s delve into it intimately.

Stone Island, very like Moncler, is an aspirational luxurious model, in all probability just a few steps beneath Moncler within the hierarchy. It focuses on premium clothes with a extra sporty fashion, emphasizing the standard and sturdiness of its clothes. Moncler determined to accumulate Stone Island in 2020 for 1.15 billion euros. The acquisition was executed with 50% in money and 50% by issuing Moncler shares. Some may elevate considerations at this level, because the prevailing knowledge on Wall Avenue usually leans in the direction of the idea that issuing shares is all the time a foul transfer. Nevertheless, let’s dig a bit deeper.

If we take a look at the data offered by the corporate itself, the acquisition of Stone Island was made at a a number of of 16.6x EBITDA, whereas the shares issued to finance the acquisition have been at a P/E ratio of 38. What does this imply? It signifies that the dilution to the shareholders was a lot decrease than the asset acquired, leading to a direct creation of worth. The golden rule of funding is that the return on funding ought to exceed the price of capital, and this seems to be an ideal instance of that rule.

World Shares Weblog

Moreover, contemplating the expansion of Stone Island in recent times, the a number of paid in 2020 is now lower than 10 occasions EBITDA. The administration has indicated that they see Stone Island in a state of affairs much like Moncler in 2003, and given how successfully they’ve optimized their flagship model, the potential for development in Stone Island may be very promising for shareholders. The technique they’re pursuing is similar as with Moncler: enhancing the model’s worth by way of correct advertising and growing management over the worth chain.

Lastly, any surplus capital from reinvestment is returned to shareholders within the type of dividends. The dividend has skilled a exceptional compounded annual development charge of 35% since 2016. At the moment, it provides a yield of two.26%, with a payout ratio hovering round 49%. Subsequently, this seems to be a really enticing inventory for dividend traders.

Q3 revenues

Every week in the past, Moncler introduced its figures for the third quarter of 2023. Regardless of a formidable 17% natural development within the first 9 months of the 12 months, development within the third quarter has slowed all the way down to 9%. This isn’t essentially unfavourable within the luxurious sector, as I mentioned in my latest article on LVMH.

Moncler Investor Relations

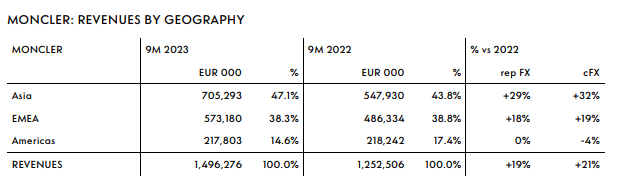

If we break it down by areas, we will see that Asia is undoubtedly essentially the most important and fastest-growing market. The Moncler model has managed to penetrate this market very efficiently and is benefiting greater than others from the area’s restoration. Europe stays sturdy, pushed particularly by tourism, whereas the American market is presently essentially the most affected.

Moncler Investor Relations

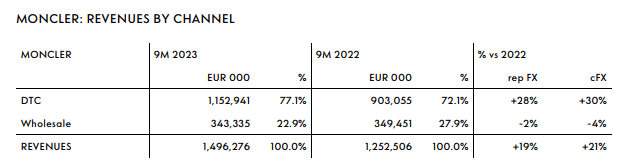

Nevertheless, it appears extra essential to spotlight that direct gross sales have elevated by 30%, whereas wholesale gross sales are declining. We’ve got already mentioned the advantages of this transition, and right here we will see it persevering with to speed up, which is superb for the way forward for the enterprise.

Moncler Investor Relations

Usually, the outcomes present that the post-COVID growth has come to an finish, and it is time to return to more healthy and extra sustainable long-term development. Regardless that this slowdown is clear, it’s value noting that Moncler has remained way more resilient than different comparable corporations like Kering, reaching efficiency much like that of LVMH or Hermes.

Valuation

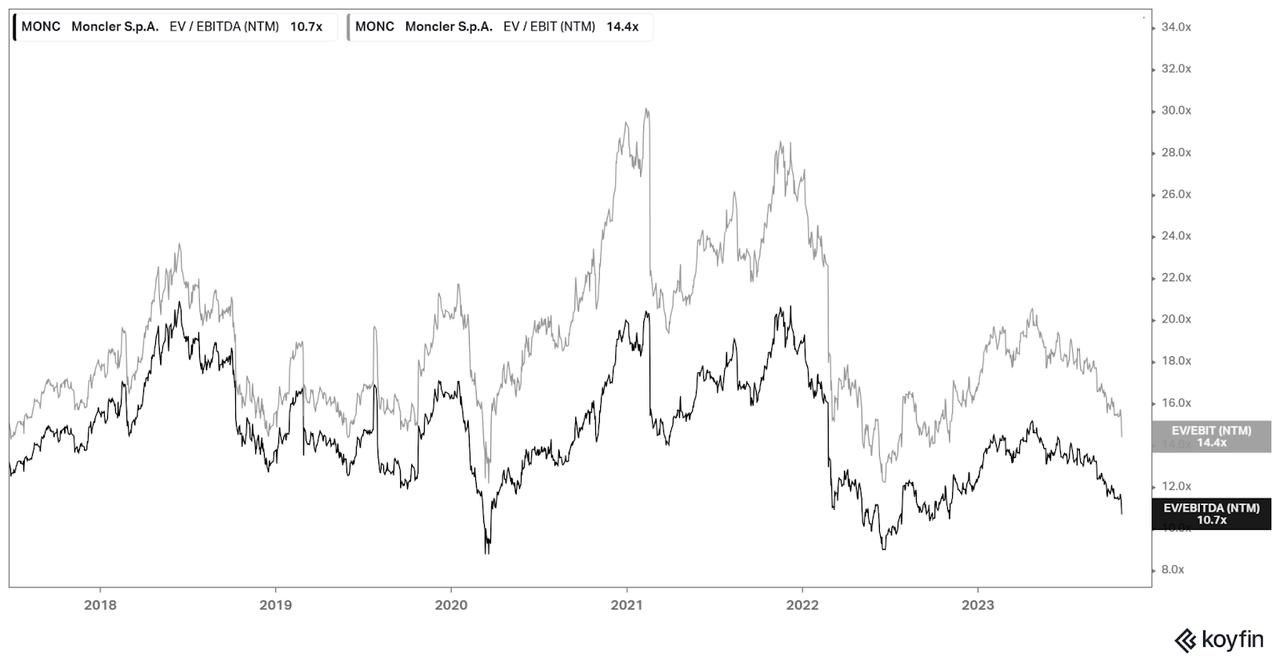

Moncler is presently buying and selling at valuation ranges practically equivalent to these it had in March 2020, on the peak of the pandemic, with a price-to-EBITDA ratio of 9.7x and a price-to-EBIT ratio of 12.5x. Right now, these figures stand at 10.7x and 14.4x, respectively. These valuations are considerably beneath their historic common, offering a considerable margin of security for contemplating the potential for buying shares within the firm.

Moncler Valuation (Koyfin)

In Might of final 12 months, Moncler’s shares have been additionally buying and selling at very related multiples to the present ones. At the moment, Remo Ruffini, the CEO selected to purchase shares on the identical valuations we see at present. This may very well be interpreted as a constructive sign, because it means that the executives discover the acquisition costs at that degree enticing. Moreover, it is essential to notice that after the executives’ purchases final 12 months, the worth of the shares elevated by practically 100%. Subsequently, if we observe new purchases by the executives, it may very well be an encouraging signal to think about shopping for Moncler shares.

Screener Insider

It is value noting that I usually favor utilizing the discounted money circulate (DCF) methodology to guage these corporations. Nevertheless, I imagine that Moncler remains to be in an early stage of its development, which makes it troublesome for me to estimate its terminal worth. This worth will depend upon whether or not the corporate’s administration can efficiently obtain their objectives of elevating the worth of their manufacturers to increased ranges inside the luxurious hierarchy. One possibility can be to make a conservative estimate of this terminal development to restrict potential losses in case of failure. However for now, I’ll chorus from conducting this valuation till I’ve a clearer image of the terminal development they will obtain.

Dangers

The primary danger when investing in Moncler, for my part, is its publicity to Asia. Regardless that its merchandise should not thought-about as strategically very important as semiconductors, now we have already seen that Asia accounts for 50% of its gross sales, and any recession or battle within the area might affect its outcomes.

One other potential danger is the poor execution in model administration and product growth. Moncler has achieved spectacular development in recent times, however market saturation within the luxurious sector or a shift in shopper preferences might have an effect on its monetary efficiency. Moreover, the corporate should keep the integrity of its model and keep away from methods that dilute its picture of exclusivity.

Conclusion

In conclusion, we will summarize the funding thesis for Moncler because the potential for its manufacturers to ascend to increased echelons inside the luxurious market. Central to this endeavor is the pivotal function of the administration, as now we have seen of their mission to boost the worth of their manufacturers by way of advertising, historical past, and buyer expertise. This can be a difficult goal, however given their sturdy execution over the previous decade, I’ve confidence that the administration will proceed to carry out nicely within the coming years. Contemplating the expansion prospects and the present interesting valuations, I assign a ‘Purchase’ ranking to Moncler’s inventory.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.

{kind=link}