helen89/iStock Editorial by way of Getty Pictures

Introduction

Microsoft Company (NASDAQ:MSFT) is the corporate which has been disrupting our world for greater than 4 a long time because it began introducing its first working programs. Microsoft’s iconic Workplace instruments, akin to Phrase and Excel, revolutionized the best way folks work and considerably boosted the productiveness of employees worldwide in comparison with the instances when workplace work was carried out on paper and numbers have been manually summed up with calculators.

Whereas Workplace instruments boosted productiveness by making the “content material” digital and extra simply editable and analyzable, these days generative synthetic intelligence, or AI, instruments even can do all of the routine work by themselves. And, as soon as once more, Microsoft is on the forefront of this new wave known as “the AI revolution.”

The corporate leverages its strategic partnership with an rising OpenAI startup, which permits it so as to add unmatched AI options throughout the entire set of its choices spanning from Cloud to Workplace Productiveness. My discounted money circulation, or DCF, evaluation means that the inventory is attractively valued with a 14% low cost, and the present share worth makes this inventory a “Sturdy Purchase.”

Elementary evaluation

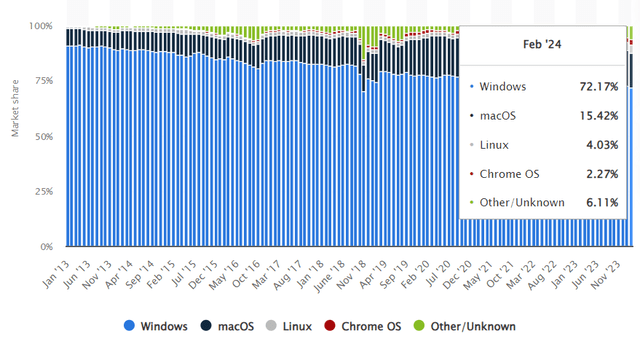

Microsoft, the world’s largest firm by market capitalization, is likely one of the most well-known manufacturers on the planet. The corporate’s affect is large because it holds 72% world market share for desktop PC working programs. Over the previous decade, the corporate’s market share within the business declined from 90% to 72%, however MSFT’s constant dedication to innovation enabled the corporate to unlock new progress and profitability drivers in recent times.

Statista

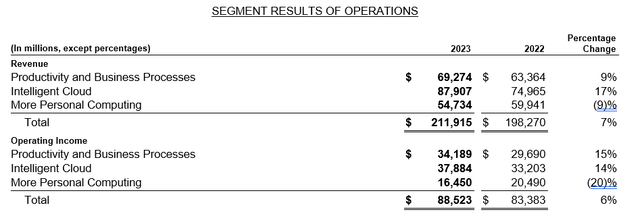

The corporate capitalized nicely on the emergence of cloud applied sciences, and its flagship Azure cloud providing turned MSFT’s new star. As of FY2023 Clever Cloud was the biggest section each primarily based on income and working revenue with greater than 40% share of the whole. Regardless of turning into the biggest section, Clever Cloud can also be the quickest rising section with a 17% YoY progress in FY 2023.

Microsoft’s 2023 annual report

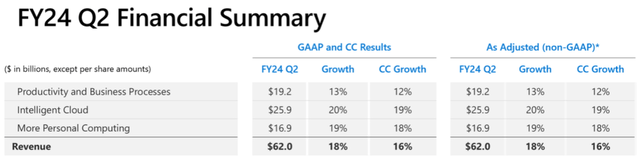

Sturdy progress momentum for the cloud remains to be there. In line with the fiscal Q2 2024 outcomes, Clever Cloud stays the foremost progress contributor for Microsoft. Development within the broader cloud market is predicted to speed up in 2024 after cooling down throughout 2023. The emergence of AI performance seems to be a powerful progress driver for the cloud business, which is a agency tailwind for Microsoft as one of many world’s main cloud gamers. The corporate competes with Amazon.com, Inc. (AMZN) and Alphabet Inc. (GOOG) (GOOGL) within the cloud business, the place all three giants account for two-thirds of the worldwide market.

Fiscal Q2 2024 presentation

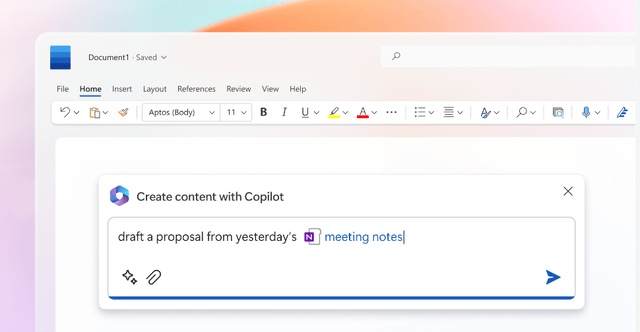

The competitors appears harmful, however I’m optimistic. As I discussed earlier, the business remains to be rising quickly, that means that there shall be sufficient room for all three giants to get pleasure from business progress. Microsoft’s substantial funding in one of many hottest corporations of 2024, OpenAI, offers it with unique entry to include OpenAI’s (the corporate which developed ChatGPT) options into Microsoft’s merchandise. And Microsoft makes use of this technological benefit throughout all its choices, not solely the cloud enterprise. For instance, Microsoft affords generative AI “Copilot” performance throughout its workplace productiveness suite Microsoft 365.

Microsoft

In an period of ecosystems and seamless integration of varied instruments, I imagine that Microsoft’s complete software program enterprise options, which counterpoint one another (Cloud and Productiveness), present a stable aggressive edge. Whereas I do not anticipate a pointy income spike because of Copilot this yr, I anticipate regular and sustainable progress as extra customers acknowledge the huge financial advantages of leveraging generative AI performance.

The robust optimistic indicator is that Microsoft and OpenAI proceed collaborating carefully to enhance their technological edge in AI. The 2 corporations are evaluating alternatives to provoke a brand new $100 billion knowledge heart with a brand new potential “Stargate” supercomputer, which can allow the companions to leverage new and extra subtle AI capabilities. One other optimistic piece of knowledge is that OpenAI plans to roll out a brand new GPT-5 model of its well-known chatbot, that means that Microsoft will even extremely probably introduce new capabilities to its product set. This may probably be a powerful reply to the current Anthropic’s launch of its Claude 3.

It seems that Microsoft doesn’t solely wager on its partnership with OpenAI to develop its footprint within the rising AI business, but additionally goals to construct a powerful AI group throughout the firm. The corporate just lately appointed one of many AI business’s pioneers, Mustafa Suleyman as its head of AI. The corporate additionally has a partnership settlement with a startup known as Inflection (the place Mr. Suleyman was one of many founders) to leverage an AI startup’s fashions and algorithms via Azure. Microsoft additionally has a waiver from claims in opposition to the corporate associated to hiring Inflection workers, that means that it has the potential to fortify its AI group with new robust engineers.

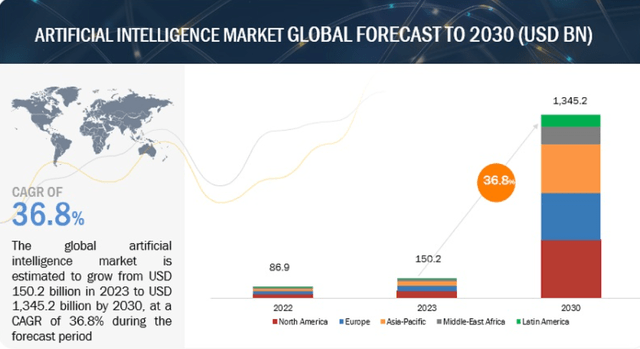

marketsandmarkets.com

To conclude, Microsoft’s huge wager on AI seems to be sound from a enterprise perspective. The AI business is predicted to achieve $1.3 trillion by 2030 and report an enormous 37% CAGR over the following a number of years. I recognize Microsoft’s agency dedication to turning into the primary software program AI firm, which can not have been publicly declared, however all of the developments counsel that Microsoft certainly plans to be the cornerstone of the AI revolution.

Valuation evaluation

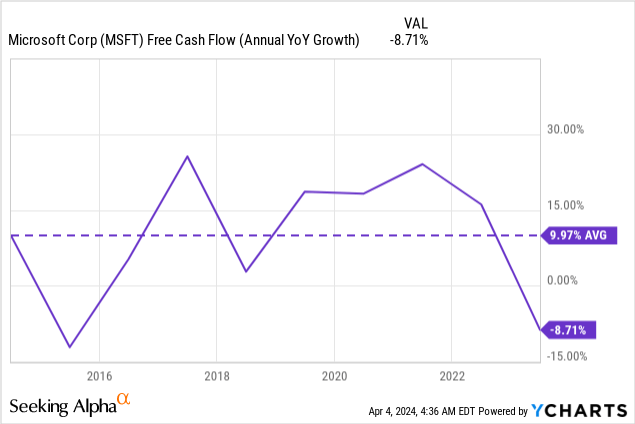

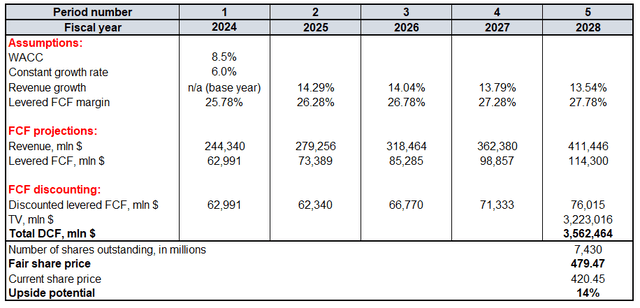

MSFT has demonstrated robust momentum throughout numerous timeframes throughout the final yr. Microsoft is at present the world’s most useful firm with a $3.13 trillion market capitalization. To worth MSFT I’ll run a reduced money circulation mannequin with an 8.5% WACC. The DCF mannequin is all about income progress charges and free money circulation (“FCF”) enhancements. In line with the under chart, MSFT’s FCF margin has been compounding with a mean 9.97% charge over the previous decade.

Contemplating traditionally speedy FCF progress along with MSFT’s standing as one of the essential corporations of the digital revolution, it seems honest to use a 6% fixed progress charge for my DCF mannequin. I consult with income consensus estimates for FYs 2024-2025 and anticipate income progress to decelerate slowly, by 25 foundation factors per yr after FY 2025. For the FCF margin, I take advantage of a TTM 25.78% stage and challenge 50 foundation factors yearly enlargement. In line with In search of Alpha, there are at present round 7.43 billion MSFT shares excellent.

Calculated by the creator

My DCF mannequin means that MSFT has round 14% upside potential. The justifiable share worth beneficial by my DCF is round $480. A inventory like MSFT buying and selling with a 14% low cost seems to be a discount.

Mitigating elements

MSFT is at present near all-time highs, and the inventory worth virtually doubled inside a comparatively quick interval (round 18 months). In these circumstances, there’s the danger that swing merchants would possibly begin recording their earnings and trim their positions within the inventory. Elevated promoting stress from profit-taking can probably drive the inventory worth decrease.

Furthermore, having such a speedy share worth progress displays considerably improved sentiment round MSFT and far greater expectations relating to the corporate’s future. Due to this fact, any antagonistic deviation from expectations (destructive information or earnings miss), may result in a pointy worth drop as traders would possibly begin reevaluating their positions.

Because the world’s largest firm and a software program behemoth, Microsoft is more likely to be a really engaging goal for potential cyberattacks. The corporate just lately revealed data that it prevented assaults from China, Russia, and Iran. All these international locations have tense relationships with america, softly talking. Due to this fact, cyberattacks on one of many U.S. enterprise flagship entities from these unfriendly regimes would possibly happen once more. Any profitable notable breaches may compromise delicate knowledge and undermine belief in Microsoft’s safety measures.

Whereas at present Microsoft is on the forefront of the AI revolution, applied sciences are evolving quickly and there’s no assure that Microsoft won’t ever lose its aggressive technological edge. The corporate had its “misplaced decade” when the inventory worth stagnated for a number of years at first of the twenty first century. Due to this fact, Microsoft’s present success doesn’t assure that AI-driven progress will final for many years.

Conclusion

Microsoft is likely one of the most necessary corporations within the ongoing digital revolution with its huge share in essential data know-how areas: working programs, cloud, and workplace productiveness. The inventory is attractively valued with a 14% low cost and in addition affords a quickly rising dividend, making it a “Sturdy Purchase” for long-term traders. There is perhaps a short lived pullback contemplating the inventory is at present buying and selling near all-time highs, however from the long-term perspective, I contemplate Microsoft’s inventory to be any investor’s must-have.

{kind=link}