Maskot

All acknowledged quantities are in Canadian {dollars} besides the place in any other case acknowledged.

Pricey readers/followers,

Medical Amenities Company (OTCPK:MFCSF) is a type of investments that I made and the place I acted “incorrectly”. I offered my small stake a few years in the past however saved an eye on the enterprise. I began protection once more in late 2023, with a “Maintain” ranking, however then gave a “Maintain” ranking in April of this 12 months as effectively. After each of those scores, the corporate noticed a considerable enhance in valuation, which suggests that there is a threat that I incorrectly valued the corporate relative to the danger profile and upside.

On this article, I am going to have a look at the corporate once more. In my final article, the place I gave the corporate a PT of $6.5, the corporate nonetheless continued to outperform upwards from this. The query turns into not solely did I incorrectly worth the corporate and is there a cause for this upside, but in addition is there extra upside to this?

Clearly, the corporate is seeing a present pattern of outperformance. However on the similar time, it is necessary to level out that the corporate isn’t in any means outperforming over the long run. In truth, in 2019 when the corporate began dropping it was buying and selling above $15/share. It is now at $13.90/share. The ten-year RoR for traders is adverse ~22%.

So whereas risk-tolerant traders have seen a major upside in 2-3 years, that isn’t the case for long-term shareholders.

Let’s have a look at what we now have right here as of the most recent quarterly report, which got here in on August sixth.

Medical Amenities Corp – a 2Q24 replace

Revisiting this firm jogs my memory numerous once I had a stake within the enterprise, and spent numerous time digesting, researching, and theorizing about outcomes and potential upsides. Let me be clear that DR.UN, or Medical Amenities Corp, isn’t in any means a nasty firm. Once I invested in it, and the remainder of the market as effectively by the way in which, it was simply maybe considerably overestimated on the upside, and with a little bit of underestimation and a little bit of “too conservative” for the danger consideration.

However in a constructive macro, with much less leverage, and with some higher concerns for a few of its belongings, the enterprise concept and the idea have been very sound.

That is additionally what we’re seeing at this specific time. The corporate is seeing will increase in income, in surgical circumstances, and a major enhance in operational revenue of 21% (though excluded for share-based compensation plans, extra on that little element later). EBITDA elevated 13.7% as effectively, however once more, adjusted for SBC. The corporate managed to repay $5M on its credit score facility – however do not forget that this enterprise Is definitely a fairly small enterprise – so $5M is kind of a bit – and returned nearly $4M to shareholders by way of buybacks.

The corporate went from being a month-to-month to a quarterly dividend payor. That is when it misplaced a lot of the market “help”. It additionally minimize the dividend to the bone and at the moment yields lower than 2.6% for the native DR.CA ticker, which makes it a no-go for me from that alone. The relative threat/reward ratio when taken this into consideration simply is not there to me.

However, I may additionally have misjudged/misvalued this enterprise – so let’s maintain going.

Medical Amenities Corp stays a play on a mixture of payor, case, and operator mixes and diversification. When these go in keeping with plan, the corporate does effectively – as we see this quarter. Surgical circumstances are up, and this in flip drives operational revenue and EBITDA. This in flip allows paying debt, which improves the profile even additional.

Additionally, a major constructive for the corporate is the complete forgiveness of the PPP loans excellent as of two months again. Full particulars right here:

Subsequent to quarter finish, the U.S. Small Enterprise Administration completed its evaluate pertaining to $6.9 of the $12.0 million in PPP loans excellent as of June 30, 2024. Their evaluate concluded with no findings, confirming full forgiveness of those specific loans. As such, we plan to file this $6.9 million quantity as authorities stimulus revenue within the third quarter and reverse the corresponding legal responsibility beforehand recorded beneath authorities stimulus funds repayable. We are going to proceed to hunt forgiveness on the remaining PPP loans, diligently pursuing all moderately obtainable channels for reversing any remaining denials.

(Supply: Jason Redman, President/CEO of Medical Amenities Corp)

A full quote is warranted right here, I consider, as a result of significance of this. It is principally like “getting” that cash again and leaving the corporate in a fair higher place. It additionally explains among the issues occurring to the corporate’s share value at the moment.

This firm now generates near half a billion CAD per 12 months in revenues, from which it makes round $88M in annual EBITDA from 114 doctor companions throughout the nation. This is because of possession of qualitative surgical services throughout the US. The enterprise concept is an effective one – contain physicians within the working of their services, with direct administration involvement, leading to superior processes and engagement. The corporate’s concentrate on leverage and excessive yield made the corporate “fail” to maintain its earlier mannequin a couple of years in the past, but it surely’s truthful to say at this specific level that the difficulty appears to be over. The corporate’s services appear higher managed, and the combo appears higher, with a concentrate on short-duration, non-emergency surgical procedures, diagnostics, imaging, and ache administration. Most of it Is Orthopedic and Neurosurgical procedures, and the opinions for the corporate are very stable.

Medical services Corp IR (Medical services Corp IR)

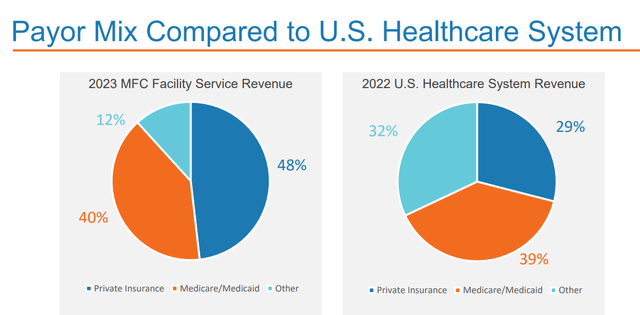

The payor combine is now additionally higher diversified- with 32% non-public, 29% different, and 39% Medicare/Medicaid in 2022 for the US healthcare system, whereas MFC has a 2023 income combine principally coming from the non-public sector.

Medical Faciliies corp IR (Medical Faciliies corp IR)

The corporate has been utilizing its vastly improved place to buy again vital quantities of shares. That is a part of why the corporate’s share value has seen such upside over a comparatively quick time. Since September of -22, the corporate has, actually, purchased again over 5M shares of its frequent inventory, for nearly $40M, which involves nearly 50% of a 12 months’s value of firm EBITDA going solely to share buybacks.

The corporate additionally elevated the dividend – however not precisely to a powerful yield as a result of it is nonetheless at an general comparatively low degree to the place it was.

The principle downside with this firm isn’t what it’s doing and the way it’s going – as a result of these are constructive developments. As a substitute, the issue is that the corporate is a comparatively small participant working within the healthcare sector and with a less-than-stellar historical past, no credit standing value contemplating, and a low yield. The potential for upside and taking a look at it relative to different potential investments right here doesn’t end in a very enticing general view for MFC.

Outdoors of my protection, most protection of this firm is now over 4 years outdated. Most appear to have deserted this firm as a possible funding. It is not that straightforward for me.

Let’s take a look at the place the valuation stands at the moment, and the way it could possibly be thought-about from right here on and ahead, relying on how the corporate does.

Medical Amenities Corp Valuation – Enticing, not less than probably, but in addition probably too dangerous

To get any kind of truthful worth for this firm we have to low cost for the impacts of buybacks, whereas additionally having a look at what’s occurring to the rest of the corporate. Now we have some attention-grabbing issues which are occurring right here – the primary of which is that the corporate has reported for the previous 2 years a adverse quantity of SBC, which I’ve not seen for a few years since I checked out some Dell (DELL) statements. The explanation could possibly be the suspension of choices after which accounted for actual money bills when the corporate pays some issues out to choice holders. Nonetheless, it is a small quantity (lower than $800k per 12 months), so I am keen to miss this for now.

As a substitute, let’s take a look at the precise firm valuation, which at the moment involves a P/E a number of of round 10x. That is to be in comparison with a mean P/E of 15x, however the firm can be usually fairly “unstable” right here – so there’s that to contemplate as effectively. Additionally, the truth that the corporate has a 58-80% probability over a 1- to 2-year foundation to negatively miss its estimates – so although the corporate is at the moment estimated to extend at 70% EPS enhance this 12 months, the chance of this appears so-so.

What I’d need to do is forecast this firm, attributable to its historic failures, at under 10x P/E. I put the valuation at someplace of a 9-11x normalized P/E over time, which once we take present estimates is not more than a 9-12% annualized charge of return, which as issues stand right here isn’t sufficient to make me .

The corporate stays an unrated and low-yielding healthcare-exposed enterprise, with a really poor historical past when it comes to working efficiency and shareholder returns.

For that cause, I am unwilling at this level to go in at above $10/share, and I’d give the corporate a “Maintain” right here till it goes again to a single-digit share value. At the moment, I might be keen to revisit this thesis.

My threat concerns for this firm are as follows.

Medical Amenities Company – Dangers

Dangers to this firm could be primarily backward-facing. The corporate has a well-established historical past of not performing very effectively over the previous 10 years, and that may be a interval the place most investments, for those who observe “valuation logic” and concentrate on qualitative companies, have achieved pretty effectively for themselves. On the very least, we have not misplaced cash – however MFC has.

For that cause, although issues appear considerably higher at the moment, I’d nonetheless be considerably cautious right here and would say that the valuation doesn’t in full mirror a “correct” weighing of threat/reward. Sure, some would possibly argue the corporate has double-digit return potential right here. I say you may get 10-15% far simpler and with an A-rating, moderately than an unrated, comparatively small enterprise.

For that cause, I am very cautious right here and would think about MFC a “Maintain” nonetheless.

Thesis

- Medical Amenities Company is a enterprise with the thought of partnering with physicians and surgeons to handle varied specialty care establishments round North America, centered on the U.S.

- The corporate has been by way of a number of iterations, together with being a high-yielding month-to-month payor that failed to carry on to this pattern and needed to minimize down its dividend not solely in yield but in addition went again from its month-to-month to a quarterly dividend mannequin. The corporate as an alternative of accelerating its distribution focuses on share buybacks given the very pressured valuation at the moment.

- Regardless of what may be argued to be a gorgeous general valuation, I don’t view Medical Amenities Company as a “BUY” right here – there are much better alternate options on the market. On the present yield, I’d “BUY” the corporate, barring no deterioration of fundamentals, at $ 9CAD for the native DR.UN ticker.

Keep in mind, I am all about:

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – corporations at a reduction, permitting them to normalize over time and harvesting capital beneficial properties and dividends within the meantime.

2. If the corporate goes effectively past normalization and goes into overvaluation, I harvest beneficial properties and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is basically secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at the moment low-cost.

- This firm has a practical upside primarily based on earnings progress or a number of growth/reversion.

This firm fulfills possibly 1-3 of my standards relying on the way you select to use them, and I don’t view it as justifying an funding in any case right here.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.

{kind=link}