spawns

Written by Nick Ackerman.

For some background on this month-to-month publication, right here is my view on dividend development shares:

Dividend development shares aren’t at all times essentially the most thrilling investments on the market. They usually aren’t grabbing the headlines, and so they aren’t the shares working up tons of of percentages in a yr. Actually, they’re usually a few of the least thrilling shares. And that’s exactly their strongest promoting level. With such an unlimited world of dividend development shares obtainable on the market, it is very important display by to see if there are any worthwhile investments to discover.

They’re shares that present rising wealth over time to earnings buyers. Dividend growers are sometimes bigger (not at all times), extra financially steady firms that may pay out dependable money flows to buyers. Some are slower growers than others. Some are going to be cyclical that require a robust economic system. Some are going to be secular, which does not usually depend on a extra sturdy economic system.

Dividend development can promote share worth appreciation. After all, that’s if these firms are rising their earnings to help such dividend development within the first place. Belief me. There are yield traps on the market – I’ve owned a couple of that I am not significantly happy with.

I like to think about investing in dividend shares as a perpetual mortgage of kinds. Basically, each dividend is a compensation of your unique capital. Ultimately, holding lengthy sufficient, you have got the place “paid off.” It’s all returned again into your pocket from that time ahead.

All of this being mentioned, it is very important perceive my strategy to dividend shares and why screening dividend shares may be essential for earnings buyers. As with all preliminary screening, that is simply an preliminary dive – extra due diligence could be mandatory earlier than pulling the set off.

The Parameters For Screening

I will be utilizing some useful options that Looking for Alpha supplies proper right here on their web site for this display. Particularly, I will likely be screening using their quant grades in dividend security, dividend development and dividend consistency.

Dividend Security is comparatively self-explanatory. These will likely be shares that SA quants present affordable security in comparison with the remainder of their varied sectors. The grade considers many various components, however earnings payout ratios, debt and free money stream are amongst these. This class will likely be shares with A+ to B- rankings.

For the dividend development class, we’ve components such because the CAGR of varied intervals relative to different shares in the identical sector. Moreover, the quants additionally take a look at earnings, income, and EBITDA development. As we’ll see, this does not imply that each inventory with the next grade has the expansion we’re searching for. This simply components in that the dividend has grown or earnings are rising to help doable dividend development. For these, the grades will even be A+ by B- grades.

Lastly, for dividend consistency, we wish shares that will likely be paying dependable dividends for us for a really very long time. Particularly, hopefully, they’re elevating yearly, although that is not an specific requirement. We will even embody shares with a normal uptrend in dividend funds, which implies there might have been intervals the place they paused will increase for a yr or two.

After these components alone, we’re left with 399 shares presently from the 406 listed final month. I will hyperlink the display right here, although it’s a dynamic record that continuously updates recurrently. When viewing this text, there could possibly be roughly when going to the hyperlink.

From there, I needed to slim down the record much more. I then sorted the record by ahead dividend yield, from highest to lowest. Since these will likely be safer dividend shares within the first place, screening for these among the many greater payers should not damage.

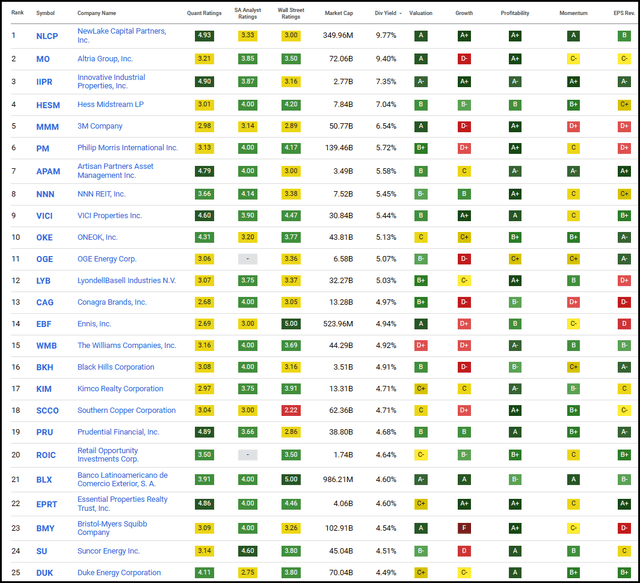

I’ll share the highest 25 that confirmed up as of 03/03/2024.

High 25 Screening (Looking for Alpha)

The names just lately lined within the final couple of months embody NewLake Capital Companions (OTCQX:NLCP) and Revolutionary Industrial Properties (IIPR), so we’ll skip over these for this month.

With that, immediately we’ll be giving a take a look at Altria (MO), Hess Midstream (HESM), 3M (MMM), Philip Morris (PM) and NNN REIT (NNN).

Altria Group 9.59% Yield

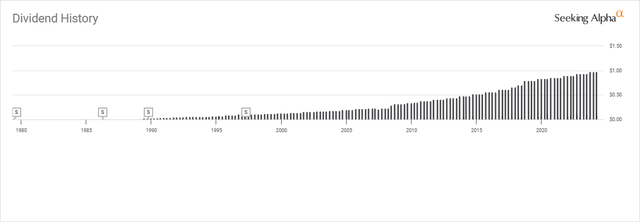

MO is a daily for this text, as we lined it simply final December and plenty of instances earlier than that as properly. That is because of the robust yield that the corporate pays out to its buyers and the dedication it’s making to rising that yield as properly. This firm is a dividend king with over 50 years of consecutive dividend development underneath its belt.

MO Dividend Historical past (Looking for Alpha)

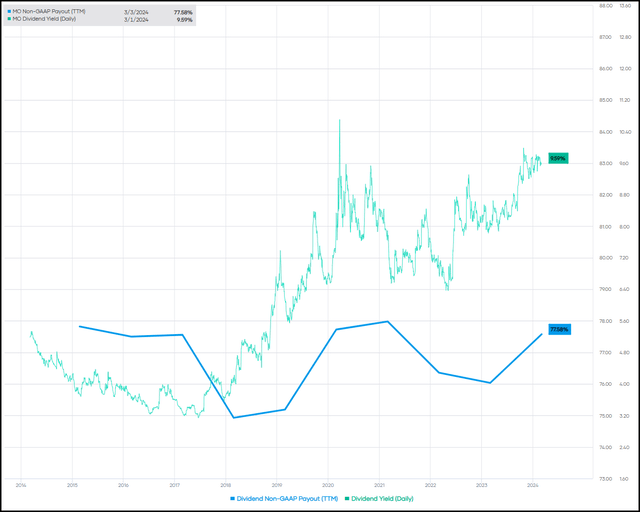

With a dividend payout ratio of round 77% primarily based on the most recent $3.92 annualized dividend and an estimated $5.05 in earnings for 2024, the payout ratio does look excessive. That mentioned, that is really fairly regular for the corporate during the last decade, and it does not imply that it appears to be like elevated in any respect. Analysts estimate that earnings ought to develop between 2 and 4.5% over the subsequent 4 years, which means that dividend development might proceed with out having to extend the payout ratio.

MO Dividend Yield Vs. Payout (Portfolio Perception)

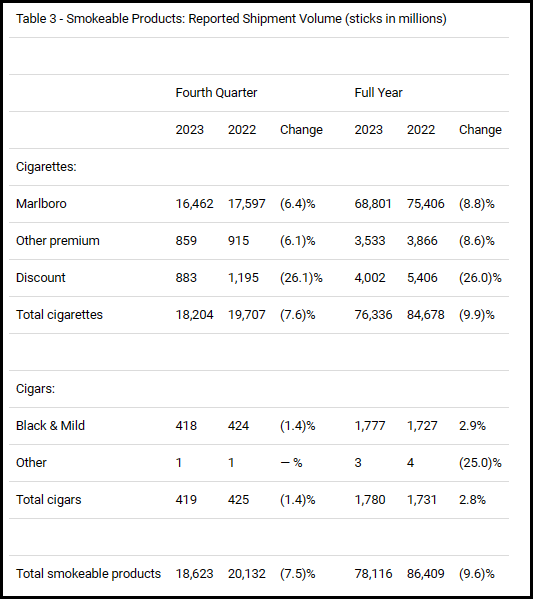

After all, the most important danger right here is individuals quitting smoking with out Altria actually having another plan that has labored to interchange conventional cigarettes. Declining cigarette shipments confirmed up as soon as once more within the newest earnings report.

For the full-year outcomes, complete cigarette gross sales fell 7.6% in This autumn and 9.9% in 2023 from 2022. The declines had been in all their classes. Actually, it was even worse for his or her low cost class, however Marlboro did not fare properly both.

MO Cargo Quantity (Altria)

The corporate has skilled income and earnings development as a result of rising costs. As a shareholder, I actually do not see that as a long-term viable path ahead. So, they do not seem like in an excessive amount of bother with the dividend but, however they are going to finally want one other product to work out for them.

Hess Midstream 7.32% Yield

HESM is one other title that makes its method on our month-to-month article now and again. Although it has been a short time, with the final time we touched on this title was final October.

HESM is a midstream C-corp for tax functions, so they are going to have a 1099 reporting and no Okay-1, which some buyers favor. The corporate describes itself as a “fee-based, growth-oriented midstream firm that owns, operates, and develops a various set of midstream belongings to offer companies to Hess and third-party prospects.”

With Hess Company (HES) seeking to be taken over by Chevron (CVX), HESM’s predominant buyer is wanting like it is going to be set to be Chevron. After all, that is not assured to occur. Exxon Mobil (XOM) appears to be placing up a roadblock to the deal however Hess is assured the deal can nonetheless get executed with CVX.

Of their earnings name, they famous that CVX is predicted to then additionally purchase Hess’s possession in HESM and be capable to appoint board members.

Hess midstream expects upon consummation of the proposed transaction, Chevron will purchase Hess’s 37.8% possession in Hess midstream, together with its proper to nominate 4 administrators to the board of Hess midstream. Hess midstream’s contract construction stays in place.

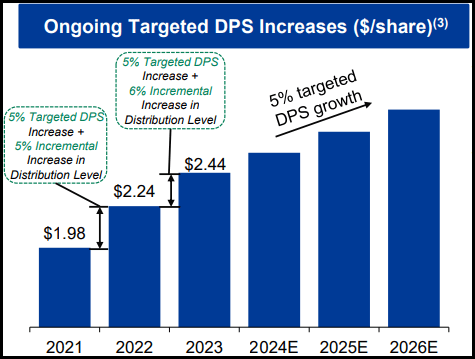

On condition that the contracts are additionally in place, it might look like this transfer is reasonably impartial for HESM and extra like “enterprise as ordinary” can proceed. That ought to additional preserve them on the right track to proceed rising their distribution to buyers. This can be a firm that has been rising its payout each quarter, and it has a focused DPS development of 5% by 2026.

HESM DPS Enhance Targets (Hess Midstream)

This development is not simply supported by hopes and desires both. They observe that they count on free money stream development of better than 10% in every of 2025 and 2026 to assist help that distribution development whereas leaving money for CAPEX.

3M 6.58% Yield

MMM is one other dividend king to make the record this month. This title hasn’t been a frequent one which we contact on, however that is now the second time it has come up. The primary was final September.

The corporate is seeking to spin off its healthcare division, named Solventum, on April 1, 2024. MMM will retain some possession over the corporate with a 19.9% stake, however that is going to be a sizeable portion of its enterprise being spun off as an unbiased firm. In This autumn, the healthcare enterprise was round 26.5% of the corporate’s adjusted internet gross sales, with the working earnings equally round a 23% portion of the enterprise.

For that, we might roughly see a 25% adjustment to the dividend. They even elevated their dividend proper on schedule to maintain the dividend king standing just lately. Nonetheless, I additionally consider the corporate will take this time to make a good bigger reduce to the dividend.

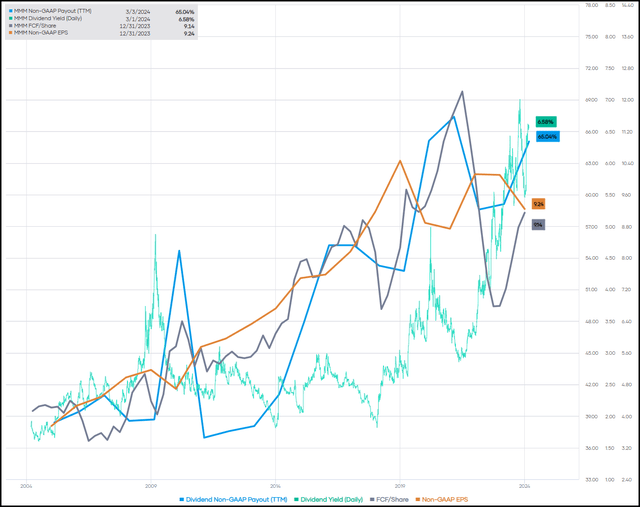

The issue is not simply the spinoff however the litigation this firm has been having to take care of. Its payout ratio is not essentially absurd presently, nevertheless it has been trending greater during the last 20 years as earnings have not been maintaining with the will increase. Earnings and free money stream have been shifting sideways, however they saved rising the dividend. Sooner or later, one or the opposite must give method: the corporate would want to see earnings development, or the dividend turns into even more durable to maintain.

MMM Dividend Payout And Dividend Yield (Portfolio Perception)

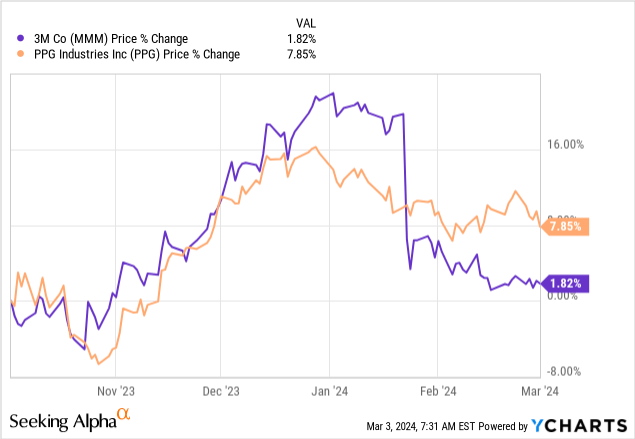

Solely time will inform. I proceed to carry my MMM place, however I diminished it final yr. I swapped out the place in favor of including a unique dividend king, which was PPG Industries (PPG). Since that point, PPG has carried out higher by way of share worth, nevertheless it did take MMM’s post-earnings plunge to get it there.

YCharts

Maybe I swapped on the unsuitable time, simply when MMM was on the mend, however my aim is to generate rising money stream over time. I really feel the overall returns will work themselves out in the long run. With that, I simply did not really feel so comfy with MMM having the ability to preserve its dividend going ahead. Whereas PPG can be a cyclical firm, they’re on firmer footing on the dividend entrance, for my part.

Philip Morris Worldwide 5.79% Yield

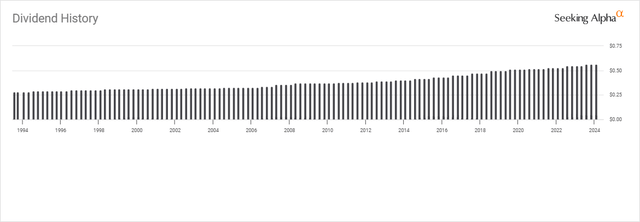

Apparently, however maybe not surprisingly, we see PM present up once more this month together with MO, which we touched on above. Just like MO, we additionally touched on PM final December, as that is one other title that has been delivering a strong and rising yield.

It does not fairly have 50+ years of dividend development itself, however that is as a result of the corporate was spun out of Altria in 2008. Although some nonetheless depend the previous firms’ dividend streak if the spin-off retains up with the will increase.

PM has been ready to try this, delivering common dividend development, nevertheless it continues to face the identical headwinds that MO does in declining smoking charges.

PM Dividend Historical past (Looking for Alpha)

With PM’s worldwide enterprise, they have been in a position to preserve the enterprise a bit extra steady. Earnings development for PM is predicted to outpace MO by a reasonably giant issue, seeing earnings development between 6.5% and 9.6% over the subsequent 4 years.

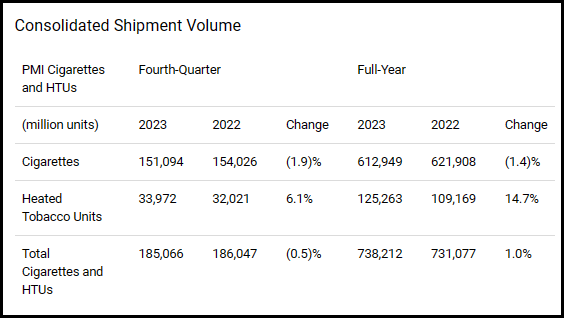

Cigarette quantity was solely barely down for the corporate in This autumn and the total yr, holding up considerably higher than MO. They’ve additionally seen vital development in cargo quantity for his or her heated tobacco product. That development was sufficient to offset the declines in cigarette shipments and enhance the corporate’s complete cargo quantity.

PM Cargo Quantity (Philip Morris)

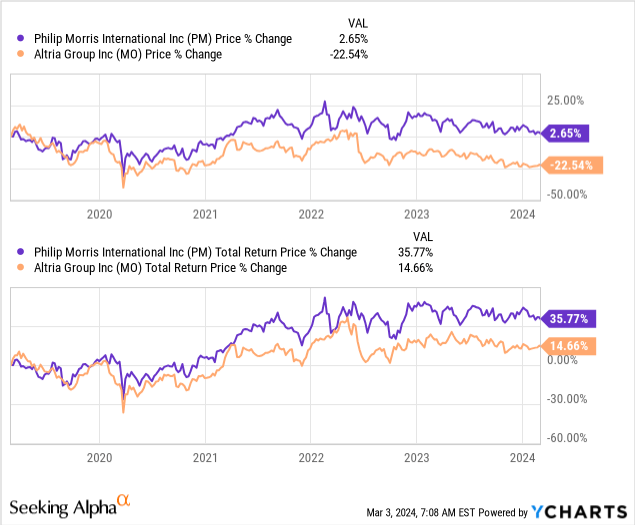

This has all been mirrored within the firm’s share worth and complete return efficiency. Over the past 5 years, neither has executed significantly properly, however comparatively talking, PM has executed a lot better.

YCharts

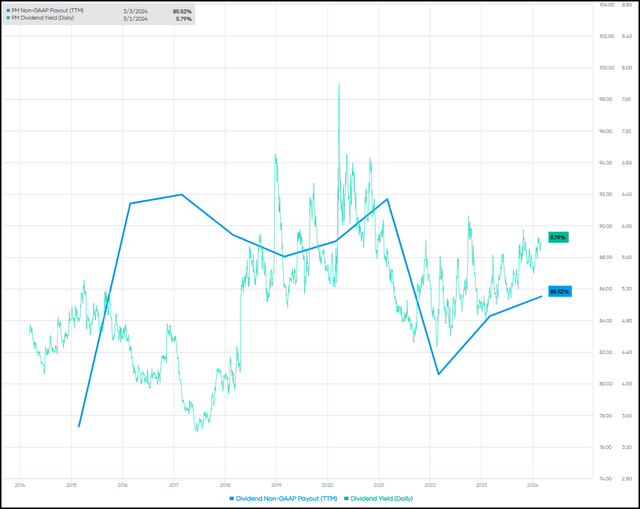

That mentioned, PM’s dividend payout ratio is greater than MO’s, nevertheless it additionally has been trending that method for the final decade. On the identical time, PM’s yield is meaningfully decrease, and that is one other reflection of the share worth holding up higher on a relative foundation.

PM Yield Vs. Payout Ratio (Portfolio Perception)

NNN REIT 5.48% Yield

Lastly, a brand new title to make it to the dialogue portion of this month-to-month screening article is NNN. Nonetheless, the REIT is much from new to me, as I maintain this as a place in what I think about my Core Portfolio. This can be a retail-focused REIT and, together with most REITs, has seen its share worth get wrecked as a result of greater rates of interest.

Larger charges imply the next value of capital when seeking to develop by way of borrowing and utilizing these borrowings to place to work shopping for extra properties. Additional, a decrease share worth signifies that issuing new shares to boost capital that method additionally now turns into much less engaging.

As REITs usually are related to a extra income-oriented kind of instrument as a result of their requirement to payout 90% of their taxable earnings, it is not simply greater borrowing prices impacting them negatively. It’s the charges rising on risk-free Treasuries that additionally make REITs a bit much less interesting to some earnings buyers.

That mentioned, one of many predominant appeals is a rising dividend that Treasuries simply do not present. NNN has been in a position to ship a rising dividend for over 30 years now. With an FFO payout ratio of 68.7% primarily based on subsequent yr’s estimates, protection appears greater than ample. The corporate additionally offered AFFO estimates of $3.29 to $3.35, which additionally bodes properly for protection.

NNN Dividend Historical past (Looking for Alpha)

FFO is predicted to develop going ahead, albeit at a really sluggish fee, however that would rapidly change when the Fed begins slicing rates of interest. We’re anticipated to see fee cuts later in 2024 and 2025, which ought to assist NNN and all REITs. After all, inflation additionally stays one of many key dangers for this area, which is that inflation will reverse and begin trending greater. That will see greater charges for even longer.

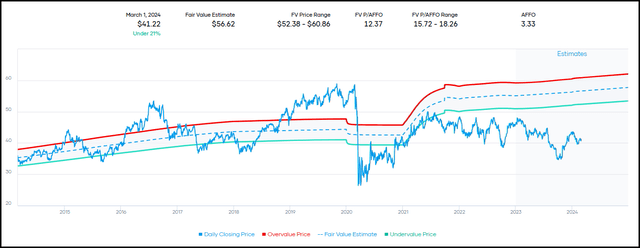

When it comes to valuation, NNN is wanting fairly beatdown and buying and selling properly beneath its truthful worth worth vary. Nonetheless, that is as a result of it’s reflecting these dangers of now greater charges and the truth that charges may have to remain greater for for much longer.

NNN Truthful Worth Vary (Portfolio Perception)

I am prepared to take that danger and think about NNN as a horny funding alternative on this market.

{kind=link}