Guido Mieth

Co-produced with “Hidden Alternatives”

Seeing cussed inflation and rising rates of interest, Mr. Market is panic-stricken. Buyers are afraid, and worry results in choices which will seem prudent within the quick time period however are very poor for the long run.

Peter Lynch, one of the vital profitable and effectively know buyers of all time, has a variety of timeless recommendation that can assist you by means of your fears.

1. Market Timing Is Futile

Individuals spend all this time attempting to determine “What time of the yr ought to I make an funding? When ought to I make investments?” And it is such a waste of time. It is so futile. I did an incredible examine, it is an incredible train. Within the 30 years, 1965 to 1995, for those who had invested a thousand {dollars}, you had unbelievable good luck, you invested on the low of the yr, you picked the low day of the yr, you set your thousand {dollars} in, your return would have been 11.7 compounded. Now some poor unfortunate soul, the Jackie Gleason of the world, put within the excessive of the yr. She or he picked the excessive of the yr, put their thousand {dollars} in on the peak each single time, depressing document, 30 years in a row, picked the excessive of the yr. Their return was 10.6 – Peter Lynch at a PBS Interview

2. Make investments In Companies That Pay Sustainable Dividends

The legendary supervisor of Constancy’s Magellan Fund additionally expressed a need for dividends, emphasizing companies with the flexibility to pay throughout recessions and people with an extended document of often elevating dividends to shareholders.

3. Spend money on firms with inelastic demand by means of financial cycles

There are a number of business sectors the place demand stays sturdy by means of bull and bear markets. These are boring firms that usually carry out bizarre and ignored capabilities in our lives.

Mr. Lynch talks about alternatives in these industries that Wall Avenue finds much less glamorous, comparable to funeral properties and waste disposal companies. Such firms delivering services that folks are inclined to maintain shopping for throughout good instances and unhealthy are a few of the greatest long-term investments.

There are a number of takeaways from Mr. Lynch’s knowledge and observe document. As revenue buyers, we undertake a number of of his rules, emphasizing revenue constructing. In that spirit, we’ve two very boring picks with inelastic companies yielding as much as 8% with many years of dividend progress.

Decide #1: ENB, Yield 6.6%

In case you are seeing considerably larger heating payments this winter, you aren’t alone. The U.S. Vitality Info Administration (‘EIA’) predicts heating payments in winter 2022-2023 will probably be about 11-25% dearer than final yr.

This bounce in heating prices is because of a number of elements, together with:

-

Under-normal winter temperatures in some areas

-

Above-average Inflation

-

The battle in Ukraine and the related power disaster

-

Rising demand for electrical energy

In November, the typical American’s power price was up 13% YoY, and the scenario is comparable for our shut neighbor, Canada. Dwelling heating prices are projected to spike ~30% in Ontario as a result of above elements.

Utility firms are extremely defensive investments since you do not cease heating your own home in a recession. Furthermore, it isn’t like the opposite utility suppliers in your space supply severe incentives so that you can change. Payments will rise over time and be paid by (annoyed) prospects.

Let us take a look at North America’s largest midstream firm by market cap – Enbridge, Inc. (ENB).

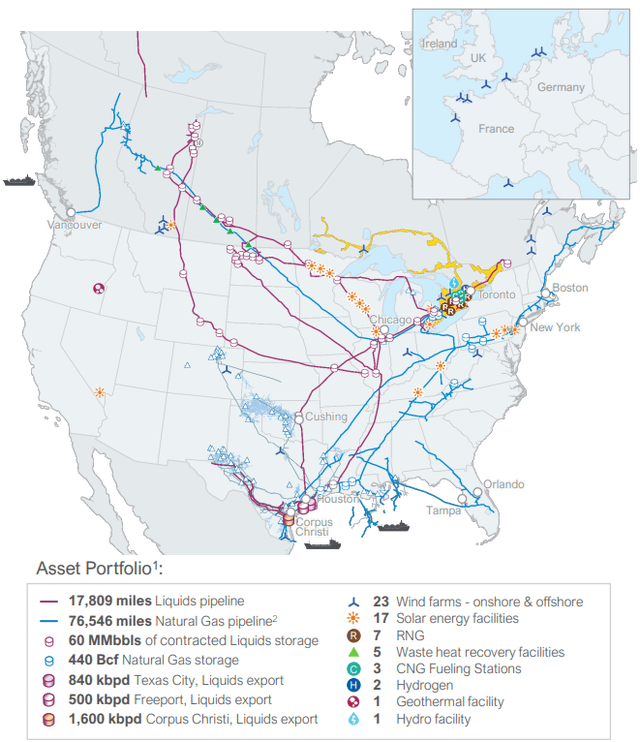

Enbridge maintains an intensive pipeline community to move and retailer pure gasoline and hydrocarbon liquids. ENB strikes ~30% of the crude oil produced in North America, transports practically 20% of the pure gasoline consumed within the U.S., and operates North America’s largest pure gasoline utility by quantity (third-largest pure gasoline utility by shopper depend). (Supply: December 2022 Investor Presentation )

December 2022 Investor Presentation

Enbridge Fuel serves roughly 75% of Ontario residents, probably the most populated province in Canada. Enbridge Fuel and its associates ship protected, dependable service to about 15 million folks in Ontario and Quebec.

As a utility firm, ENB’s charges are regulated with inflation and commodity value protections. In June, the Ontario Vitality Board (‘OEB’) authorized a ~20% enhance in pure gasoline for utility suppliers. In September, one other fee hike was authorized, and ENB lately disclosed having utilized to the OEB to vary its distribution, transportation, and storage charges beginning January 1, 2024.

This firm is able to passing on rising prices to customers, making it a superb long-term inflation hedge.

In Q3, Enbridge reported a 15% larger YoY Adj. EBITDA and 9% larger Distributable Money Move (‘DCF’). The corporate additionally offered FY 2022 DCF C$5.20 – C$5.50, which places its C$3.44 FY 2022 dividend at a modest 64% payout.

For 2023 the corporate expects the next DCF of C$5.25-C$5.65/share.

ENB additionally forecasts full-year EBITDA of C$15.9B-C$16.5B, which displays ~6% progress from the midpoint of its 2022 steering vary. Attributed to rising DCF, ENB raised its dividend by 3% for FY2023 (65% payout at midpoint DCF steering).

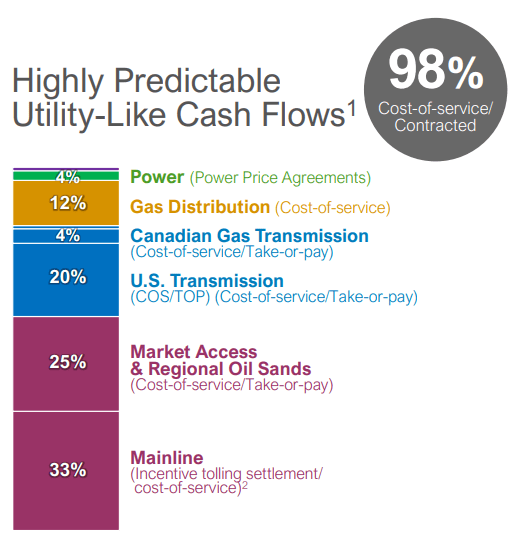

ENB is a recession-resistant midstream company with an investment-grade steadiness sheet. 90% of the corporate’s debt carries mounted rates of interest, immunizing the midstream large from these inflation-focused fee hikes. Furthermore, 98% of ENB’s money flows are underpinned by Price-of-Service or contractual agreements, bringing excessive predictability to the corporate’s earnings.

December 2022 Investor Presentation

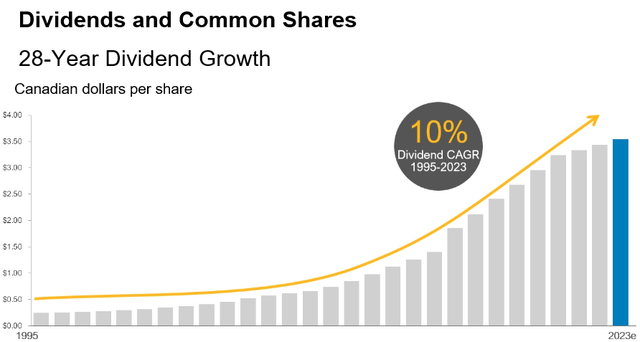

ENB is a Canadian dividend aristocrat with 28 years of consecutive annual dividend raises. (Supply: Enbridge.com)

Enbridge.com

ENB’s C$3.55 ahead annual dividend cost calculates to a 6.6% yield. As well as, ENB has a C$1.5B buyback program, out of which the corporate has solely 10% utilized. Wanting on the firm’s deal with dividends and buybacks, it’s clear that it’s a excessive precedence for administration to carry worth to shareholders.

*Be aware: ENB declares and pays dividends in Canadian {Dollars}. The dividend revenue obtained by U.S. buyers is variable as a result of fluctuating USD-CAD conversion charges.

U.S. buyers holding ENB in a taxable account might expertise a 15% tax withholding. Nevertheless, tax-advantaged accounts comparable to IRAs are excluded from Canadian dividend withholding tax.

As a big midstream-utility combo, Enbridge offers the tasty mixture of dividend progress and recession resistance to your portfolio. This is a superb power firm to put money into and acquire immunity from unstable power costs. Who stated boring companies could not be enjoyable? 6.6% (and rising) yields that may make you’re feeling heat and fuzzy on this chilly winter.

Decide #2: MMP, Yield 8.2%

Magellan Midstream Companions (MMP) owns and operates probably the most in depth refined petroleum merchandise pipeline system within the U.S., with entry to just about 50% of the nation’s refining capability. The agency has the capability to retailer greater than 100 million barrels of petroleum merchandise, comparable to gasoline, diesel gasoline, and crude oil.

MMP is a Grasp Restricted Partnership (‘MLP’) that points a schedule Ok-1 for tax functions.

MMP Operates two core enterprise segments, break up by % of the web working margin – refined merchandise (72%) and crude oil phase (18%). Each are glorious money cows with highly effective multi-year asset monetization capabilities.

Crude Oil – 70%+ of MMP’s long-haul pipe capability is supported by take-or-pay commitments from creditworthy counterparties for the following 3-6 years. This improves the predictability of this phase’s money flows.

Refined Merchandise – This can be a extra important phase for MMP and offers a stable protection towards long-term inflation as a result of tariff adjustments are tied intently to the Producer Worth Index in addition to different market elements. MMP can simply cross on inflation pressures to its prospects by means of contractual assist.

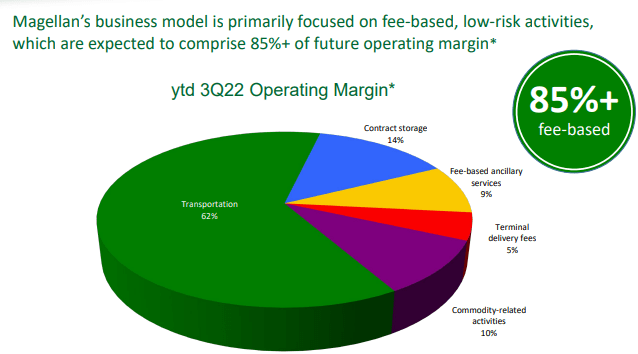

In brief, MMP’s enterprise mannequin could be very low-risk actions (comparable to transportation and storage of power commodities) supported by long-term, fee-based contracts. 85% of MMP’s working margin is fee-based, thereby defending the partnership’s profitability amidst unstable power costs. (Supply: December 2022 Investor Presentation)

December 2022 Investor Presentation

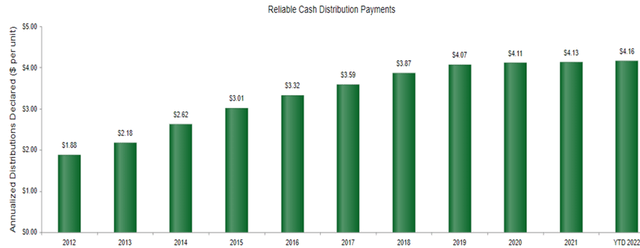

MMP maintains a top quality partnership construction with no Incentive Distribution Rights (‘IDR’). Because of this shareholders may have most entry to the corporate’s DCF. MMP has been a superb distribution steward with 21 years of annual distribution raises. (Supply)

Magellanlp.com

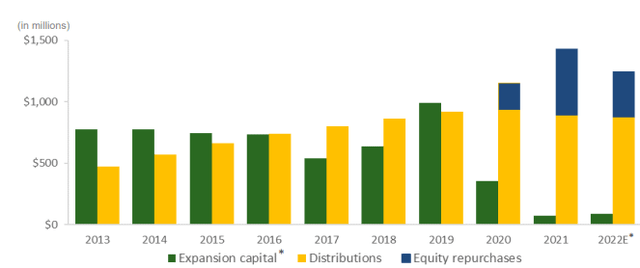

In October, the MMP introduced a 1% elevate to the quarterly distribution, and the brand new distribution calculates to an 8.2% annualized yield. Together with distributions, MMP has been aggressively shopping for again shares. Throughout Q3, the partnership spent $138 million to repurchase 2.7 million items at a mean value of ~$50/unit. YTD, MMP has spent $377 million on buybacks (a complete of $1.2 billion for the reason that graduation of the repurchase program).

These repurchases have been so important that MMP has been spending much less on distributions. YTD, the partnership has paid 5% much less YoY in the direction of distributions (discover the smaller yellow bars for 2021 and 2022 within the under chart). MLP buybacks are a internet optimistic for an revenue investor because it will increase shareholder entry to a rising DCF.

December 2022 Investor Presentation

In Q3, MMP’s Adjusted Earnings/unit was $1.29 (12% YoY enhance), and DCF grew to $290 million (12% YoY enhance). The partnership reported a free money stream of $273 million, leading to free money stream after distributions of $58 million. MMP is utilizing extra money after distributions in the direction of growth tasks to broaden the corporate’s general belongings. The partnership tasks a Capex of ~$90 million in 2022, $100 million in 2023, and $40 million in 2024 in the direction of dedicated growth tasks and expects them to be obtainable for achievement in 2024.

MMP maintains an investment-grade steadiness sheet with a 3.7x leverage. That is among the many lowest leverage ratios within the midstream business, and the partnership has no debt due till 2025. On the finish of Q3, MMP’s debt excellent was $5.2 billion, and its weighted common rate of interest was 4.3% YTD (a ten bps discount from the identical interval final yr).

MMP presents a gentle 8.2% yield from a low-risk enterprise with regular demand and inflation-defying pricing energy, making it vital for revenue buyers.

Dreamstime

Conclusion

Peter Lynch is a profitable fund supervisor with many years of above-average returns by means of quite simple funding rules. Most significantly, he does not imagine in market timing and strongly recommends towards this for the typical investor. Enterprise efficiency and the motion of their shares can usually be uncorrelated; profitable buyers combat the worry and cargo up on such alternatives.

No one can predict rates of interest, the long run course of the economic system or the inventory market. Dismiss all such forecasts and focus on what’s truly occurring to the businesses by which you’ve got invested – Peter Lynch

Peter Lynch strongly advocates diversifying investments throughout a number of classes of shares to cut back draw back threat. Most significantly, Mr. Lynch is a giant fan of firms with many years of dividend progress. Each rules we maintain shut in our investing technique.

The dividend is such an necessary issue within the success of many shares that you can hardly go mistaken by making a whole portfolio of firms which have raised their dividends for 10 or 20 years in a row. – Peter Lynch

At HDO, we keep a core portfolio of over 45 securities to diversify and defend our revenue. 2022 might have been a rocky yr for the markets, however our portfolio revenue is rising robust. Fortify your revenue with inelastic companies paying rising dividends. Now we have two picks with as much as 8% yields to get you began.

{kind=link}