FatCamera/E+ by way of Getty Photos

Co-produced with Treading Softly.

Once I exit and about, I like to look at how the world works. I like to soak up all of the accessible data and stay observant. Younger youngsters think about that the meals makes it to the cabinets of their native retailer from some magical or ethereal location. They do not perceive how meals goes from farm to retailer.

Likewise, we see branded fuel stations, however hardly ever think about how gasoline makes it from floor to the pump.

Nothing makes me happier than being paid for each the thrilling and mundane elements of life. I’d spend money on rain clouds if it meant I’d receives a commission anytime it rains! So long as they’d optimistic cashflow and regular dividend protection!

So, after I go to the grocery retailer or fill my automotive’s tank with gasoline, I would really like nothing greater than for it to pay me again for my efforts.

Immediately, I wish to cowl two alternatives to make that occur for you.

Let’s dive in!

Decide #1: BGS Bond – 10% YTM

Inflation has hit the grocery retailer aisles exceptionally exhausting. Customers are combating the rising costs, however few notice that the prices of getting those self same objects to the cabinets have additionally turn out to be dearer.

After we final coated B&G Meals, Inc. (BGS), we defined why we side-stepped the frequent shares and their enticing yield in favor of transferring larger into the capital stack.

We outlined two vital dangers – inflation prices and the probability of a typical dividend lower. As we anticipated, BGS lower their frequent dividend closely in November of 2022 to regulate their capital spending to extra simply service debt. An unsustainable dividend proved to be unsustainable.

Their 4th quarter earnings, nonetheless, offered a number of glimmers of hope for a greater future from our perspective.

The primary vital optimistic was that their inflation-related worth changes are beginning to attain their backside line and assist restore BGS’s much-needed margins.

This autumn 2022 generated $0.40 in adjusted diluted earnings per share vs. $0.39 in This autumn of 2021. It is a optimistic growth from BGS’s worth changes.

We don’t maintain the frequent shares, however we elected to climb larger into the capital stack and purchase the BGS bond maturing in 2025 – the primary debt demanded to be dealt with by administration.

Finra – Morningstar

Presently, the pricing of this bond is equivalent for essentially the most half to our final replace on BGS, however the YTM is larger now as a result of we’re nearer to that date. The bond’s CUSIP is 05508RAE6.

Administration is concentrated totally on rising the core enterprise of BGS and promoting off decrease margins, much less in-focus property. With this focus, BGS offered off “Again to Nature” snack model. This transaction pressured a $50 million prepayment on their floating price time period mortgage which matures in 2026.

BGS has an curiosity protection ratio of two.4x with their Adjusted EBITDA for the 2022 fiscal 12 months. We’re electing to make use of Adjusted EBITDA for this analysis vs. EBITDA as a result of a big adjustment from a non-cashflow impairment utilized because of the sale of “Again to Nature.”

This ratio ought to proceed to enhance as their debt is decreased total but additionally negatively impacted by rising charges.

We proceed to search out the bond a lovely method to get earnings from on a regular basis grocery purchases whereas sidestepping the drama of the frequent shares. BGS is continuous to guage extra divestitures to cut back its debt. Our bond holdings are callable at any time if BGS decides to deal with them prematurely and the bond presents a lovely earnings for now and a long-term upside in 2025 on the newest.

Decide #2: CAPL – Yield 9.8%

CrossAmerica Companions LP (CAPL) is the smallest of the “huge 3” gasoline distributors and one we have been intently looking forward to some time now.

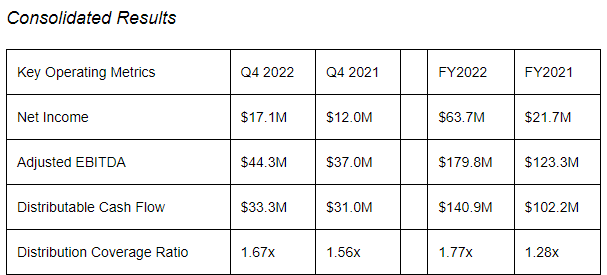

After we take a look at CAPL, we discover its giant and beneficiant yield of 9.7% enticing, so we’re not in search of development however sustainability. Fortunately, this has been CAPL’s main focus all through 2022 as properly. We are able to see that CAPL outperforms 2021 on each key metric, each quarterly and yearly: Supply.

CAPL Incomes Launch

Their protection for This autumn of 2022 improved in comparison with This autumn of 2021 by 0.11x, a formidable achieve, and the full 12 months protection improved by 0.49x – which is much more spectacular. As protection will increase, so ought to one’s confidence within the surety of their distribution.

Gasoline distribution and comfort retailer operation suffers from seasonality. This implies Q2 and Q3 are often exceptionally sturdy, whereas Q1 and This autumn are weaker. This is because of “journey season,” the place customers usually tend to hit the street within the spring and summer season months than they might within the colder months.

CAPL is extra strongly uncovered to this seasonality than their friends Sunoco LP (SUN) and World Companions LP (GLP) as a result of CAPL is strictly centered on gasoline distribution, whereas SUN and GLP have gained publicity to extra “conventional” midstream property.

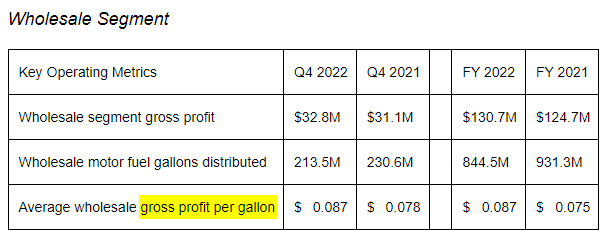

The important thing metric to look at and perceive in 2023 for CAPL can be its cents per gallon revenue margin:

CAPL Incomes Launch

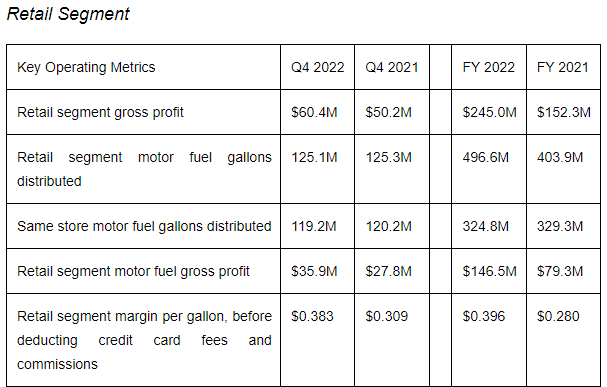

We’re seeing extremely elevated gross revenue margins in comparison with prior years. This is because of all of the financial and world uncertainty all through 2022. GLP’s administration crew highlighted that their revenue margins have moved again to historic developments, which have been final seen in 2021; CAPL won’t be resistant to this pattern. Likewise, of their retail section, CAPL noticed elevated revenue margins as properly:

CAPL Incomes Launch

This can cut back their backside line revenue in 2023 as their quarterly earnings are launched and can cut back their distribution protection ratio.

We don’t foresee a distribution lower in 2023, however year-over-year comparisons will seem unfavourable as evaluating a “regular” 12 months vs. a “report” 12 months.

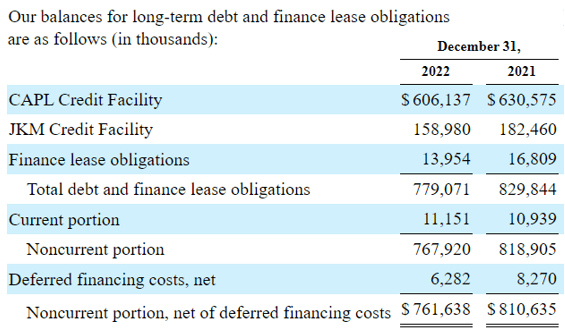

The opposite key metric to check out CAPL is its debt ratio. Taking CAPL’s blended mixture leverage ratio into consideration, after we final coated CAPL, their ratio was sitting at 4.85x, and so they ended 2022 sitting at 3.9x. It is a continued optimistic pattern. CAPL maintains a purpose to have 4x or decrease leverage ratio, so they’re presently on the excessive facet of their goal. Supply.

CAPL 10-Okay This autumn 2022

The important thing to retaining this metric at acceptable targets is the continued discount of their long-term debt. After we final coated CAPL in August 2022, their complete debt stood at round $788 million; presently, it’s all the way down to $761 million. We might wish to see CAPL proceed to cut back their debt as they see pressures on their revenue margins as they normalize. Administration has been very proactive on this space, and we’re happy with this focus.

With CAPL, we will take pleasure in a excessive yield and clear focus by administration on lowering debt whereas enhancing protection of the distribution they’re paying out. I will fortunately accumulate my 9.8% and luxuriate in watching them progress on their targets.

All of us have to drive to work, to the shop, or to go to household. I would just like the pump to pay me again, and with CAPL, it does!

Word: CAPL points a Okay-1 at tax time.

Conclusion

Whereas I can not spend money on rainclouds, I can spend money on CAPL and the 2025 bond supplied by BGS to unlock earnings from on a regular basis life necessities. I receives a commission by the fuel pump, I receives a commission by my frozen veggies and cooking oil.

Each corporations highlighted as we speak are centered on lowering their total debt or leverage profile to the advantage of particular courses of stakeholders. BGS is making an attempt to handle their debt in a approach that advantages their bondholders at the beginning. CAPL is specializing in lowering their debt ratios to take care of their goal ratios which advantages their frequent unitholders.

I like when a administration crew works in direction of my profit, all whereas paying me handsomely for being a stakeholder of their enterprise. That approach, my retirement is one which sees dividends raining into my account regularly and washing away my bills in a deluge of earnings.

Sounds nice, would not it?

{kind=link}