JHVEPhoto

Mondelez Worldwide, Inc., (NASDAQ:MDLZ) by means of its subsidiaries, manufactures, markets, and sells snack meals and beverage merchandise within the Latin America, North America, Asia, the Center East, Africa, and Europe.

Now we have began protection on the agency in March 2023, with an preliminary “maintain” ranking. The first causes again then for our impartial view have been:

- Deteriorating profitability, together with declining return on fairness and declining web revenue margin

- Bettering asset turnover, pushed by income development

- Rising leverage within the capital construction

- Overvaluation based mostly on a set of conventional worth multiples

Since our earlier writing the inventory worth has elevated by 8%, underperforming the broader market, which has gained 15% in the identical interval.

Evaluation historical past (Writer)

At the moment we will likely be trying on the agency’s Q2 outcomes and focus on whether or not the latest numbers are displaying any enchancment in phrases of profitability and effectivity and whether or not it may very well be sufficient to justify the present worth ranges.

Q2 outcomes

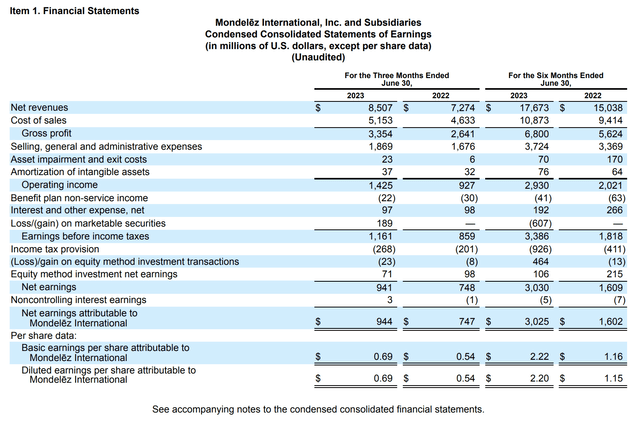

The next desk reveals MDLZ’s most up-to-date earnings assertion.

Earnings assertion (MDLZ)

It’s clearly seen that the agency has achieved vital development each when it comes to income and EPS. This 17% enchancment in web revenues will be attributed to a number of elements:

- the upper demand for MDLZ’s merchandise, which can be pushed by the bettering macroeconomic setting

- acquisitions of Clif Bar and Ricolino in 2022

- beneficial quantity/combine

These optimistic impacts have been partially offset by the unfavorable FX setting and the influence of divestitures in 2022.

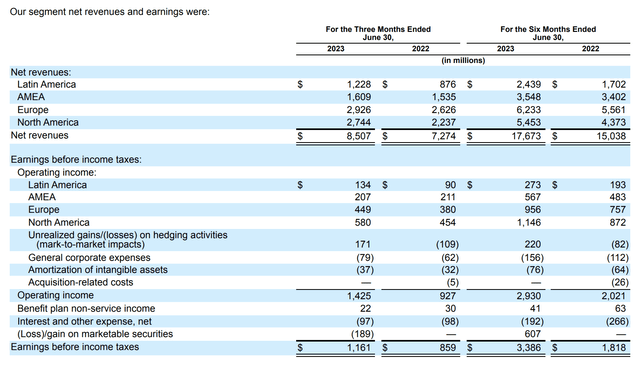

Additionally vital to notice, that every one segments (areas) have been contributing to the income development.

Phase outcomes (MDLZ)

In our opinion, the demand for MDLZ’s merchandise is prone to stay robust within the coming quarters, because the macroeconomic setting, together with shopper confidence and inflation price have been bettering step by step throughout the globe prior to now months. The agency’s up to date outlook on 2023 additionally confirms our thesis:

For 2023, the corporate is updating its 2023 fiscal outlook and now expects 12+ p.c Natural Internet Income development versus the prior outlook of 10+ p.c, which displays the power of its year-to-date efficiency.

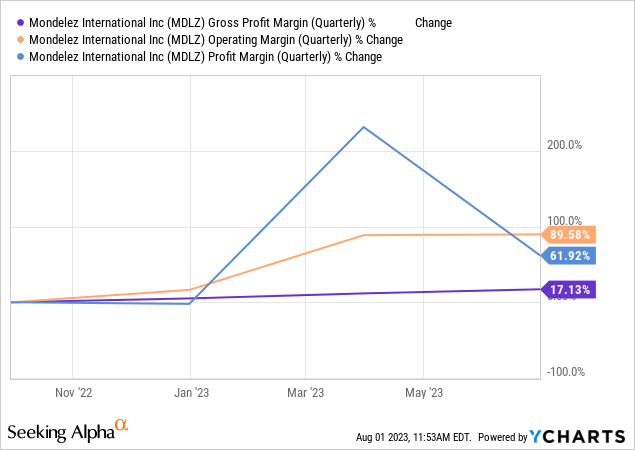

The upper income has not been the one optimistic for MDLZ within the earlier quarter. The agency’s profitability has considerably improved in comparison with the prior yr. The next chart reveals, how the three key margins have developed prior to now 12 months.

Whereas enter prices have improved as a consequence of a number of elements, the speed of improve has been slower than the speed of income development. The primary contributors to the price will increase have been the upper uncooked materials prices, together with power, sugar, dairy, grains, packaging, cocoa, edible oils and different substances prices.

These have been nonetheless, partially offset by decrease manufacturing prices pushed by productiveness.

SG&A bills have additionally elevated, however once more at a slower tempo than the income development. This results in an working margin enlargement from 12.7% to 16.8% YoY.

Complete promoting, normal and administrative bills elevated $193 million from the second quarter of 2022, as a consequence of plenty of elements famous within the desk above, together with partially, the influence of acquisitions, greater divestiture-related prices, greater remeasurement lack of web financial place and lapping prior-year lower in estimated allowances and reserves related to incremental prices incurred because of the warfare in Ukraine, which had been partially offset by a good foreign money influence associated to bills, decrease acquisition integration prices and contingent consideration changes, lapping prior-year acquisition-related prices and decrease implementation prices incurred for the Simplify to Develop program.

All in all, we consider that the agency’s Q2 monetary efficiency represents a big enchancment to the earlier quarters. Wanting ahead, we want to see the margins additional increasing, together with income and EPS development, which might be pushed by the bettering macroeconomic setting.

The monetary efficiency nonetheless, has not been the one pleasing information for buyers within the second quarter.

Return to shareholders

The agency within the first half of the yr has returned as a lot as $1.7 billion to its shareholders. They’ve additionally managed to extend their dividends by as a lot as 10%. As of now, the agency pays a quarterly widespread dividend of $0.43 per share, equal to an annual yield of two.3%.

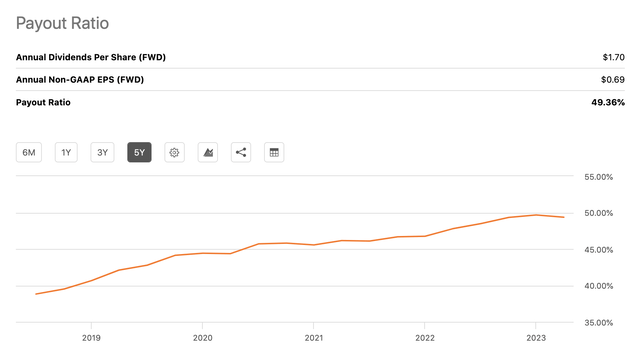

By trying on the payout ratio we will see that the dividend stays effectively coated and prone to stay sustainable within the coming months because of the stronger demand for MDLZ’s merchandise.

Payout ratio (Searching for Alpha)

Conclusions

Double digit income and EPS development within the second quarter, beating each top- and backside line estimates of analysts.

The bettering macroeconomic setting, together with bettering shopper confidence, moderating inflation ranges and falling power costs, is prone to create additional tailwinds to MDLZ’s enterprise. The margins might preserve increasing additional within the coming months.

The agency has been additionally rewarding its shareholders with engaging returns within the first half of the yr, together with a ten% dividend improve.

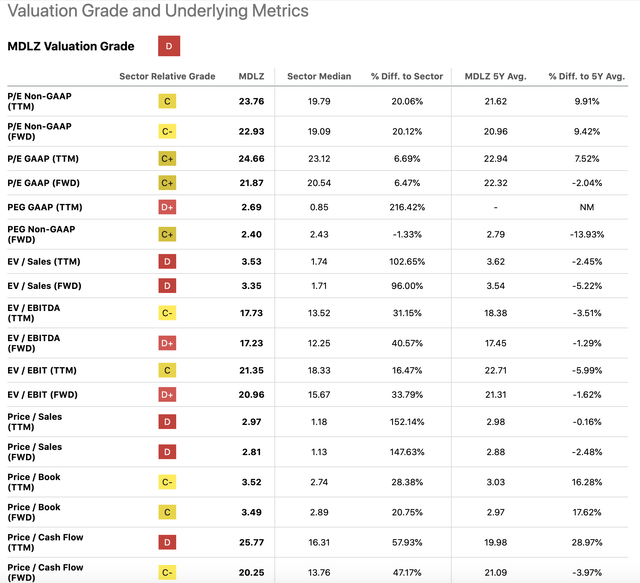

Whereas the valuation of the agency has not improved since our final writing in line with the identical set of worth multiples, we consider that the premium is rather more justified now because it was earlier than, pushed by the robust Q2 development.

Valuation (Searching for Alpha)

For these causes, we improve Mondelez to “purchase”.

{kind=link}