RiverNorthPhotography

I’ve written eight articles on Iron Mountain (NYSE:IRM) courting all the best way again to June of 2017. All eight have been bullish. This will likely be my first bearish piece on IRM.

The corporate has not modified.

The valuation has.

IRM’s market worth appears to be pushed by narratives which have induced mispricing in each instructions.

Altering narratives

From 3-7 years in the past, the overriding narrative on IRM was that it was dangerous as a result of its reliance on bodily paper storage. The concept was that utilization of paper for documentation was going away and since IRM bought most of its income from storage and shredding of paper paperwork its revenues have been in danger.

On account of this narrative, IRM traded at a really low cost a number of. Regardless of its AFFO/share progress, it was considered as a declining asset.

Round three years in the past, the narrative on IRM shifted. Its burgeoning information middle division took middle stage. Speedy growth and lease-up of information facilities started to drive progress for IRM and the market began to cost IRM at a knowledge middle a number of. The value positive factors accelerated as synthetic intelligence grew to become synonymous with information facilities.

S&P International Market Intelligence

Within the final three years, public notion of IRM went from an outdated bodily paper firm, to a cutting-edge AI firm.

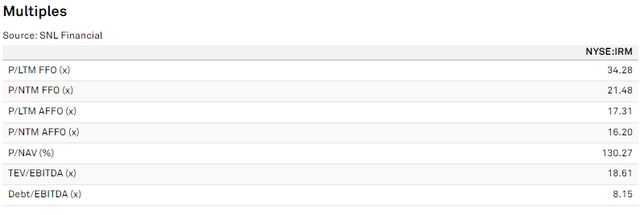

The AFFO a number of went from round 10X to 17X.

S&P International Market Intelligence

Word that there are some improper gadgets within the AFFO calculation and if we appropriate it to true earnings, the a number of is definitely 24X as we speak (extra on this later).

On this article, I intend to exhibit that IRM is neither a paper firm nor a cutting-edge AI play.

The narratives went approach too far in each instructions and resulted in opportunistically low cost pricing 3-7 years in the past and overvaluation as we speak.

Precise Iron Mountain Enterprise

Iron Mountain’s precise enterprise has not modified a lot. It has at all times been an info administration firm. It adapts to no matter type its clients want their info with IRM’s fundamental experience being a unprecedented sense of group and safety.

IRM companions with nearly each giant firm on the planet together with almost all the Fortune 100 to guard and retrieve their information. Clients pay for this service as a result of the velocity and group of IRM’s info retrieval facilitates their workloads.

So far as I can inform, this form of service is equally useful to the client whether or not the info is on paper paperwork saved in an IRM warehouse or digitally saved in an IRM information middle.

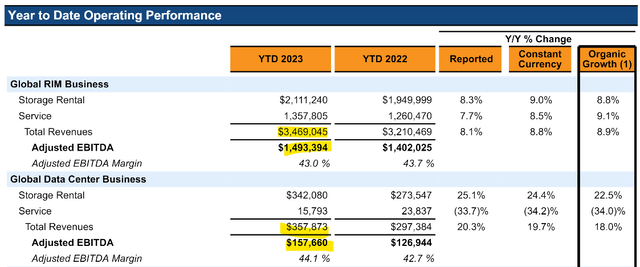

Whereas the info middle enterprise is rising quickly, the corporate remains to be near 90% bodily storage by way of EBIDTA technology. Word the $1.5B of “Information Info Administration” EBITDA which is their time period for the paper and different bodily storage legacy enterprise.

IRM

This compares to $158 million in information middle EBITDA.

Thus, I discover it exhausting to justify pricing IRM as a knowledge middle or AI play when the overwhelming majority of its enterprise remains to be bodily.

That mentioned, I additionally don’t imagine that information middle or AI is essentially higher than the previous tech enterprise. Margins are virtually an identical within the low to mid 40% vary and each companies are rising properly organically.

Iron Mountain’s operations and progress

Over the past seven years, IRM has demonstrated operational excellence. Renewal charges on its present enterprise are extraordinarily excessive indicating completely happy clients and these completely happy clients have gotten information middle clients.

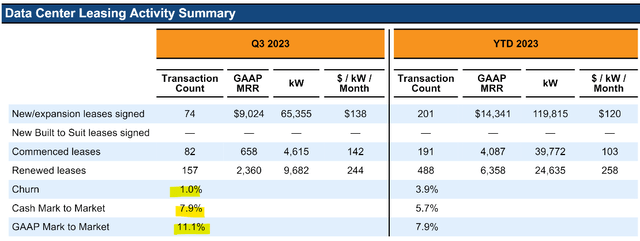

This reveals up in superior lease-up of information middle house at the same time as in comparison with pure-play information middle firms. The tempo of latest lease-up has been spectacular with 65,355 kW of latest leases in 3Q23.

IRM

Additionally spectacular is the low 1% churn and seven.9% money mark to market on renewals. Knowledge facilities have usually struggled with mark downs on renewals so this being a constructive quantity already units it above Digital Realty (DLR).

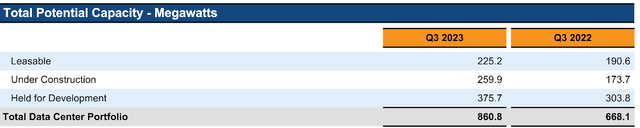

IRM is quickly increasing its information middle footprint with 259.9 megawatts below development and one other 375.7 megawatts able to be developed.

IRM

Word that the pipeline is nearly 200 megawatts bigger than it was only a yr in the past.

Maybe it’s the tempo of this progress that impressed the narrative.

We additionally discover the expansion spectacular and have lengthy thought IRM is a superb firm. Our sticking level as we speak, and why now we have offered our shares, is valuation. To get a greater sense for IRM’s present valuation allow us to start by correcting reported AFFO to get to a more true earnings quantity.

AFFO to true earnings

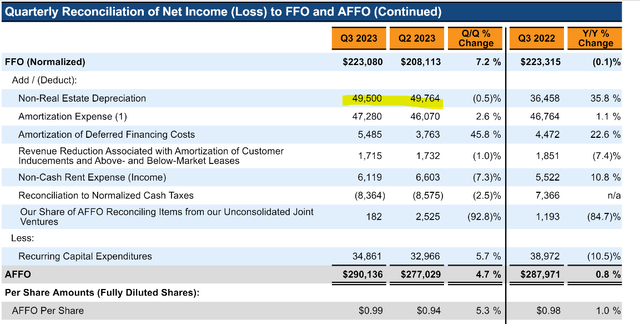

AFFO in 3Q23 was $0.99 per share.

Supplemental

There are a variety of addbacks which we don’t suppose signify true earnings.

In reconciling normalized FFO to AFFO IRM provides again $49.5 million of non-real property depreciation.

As REIT analysts we’re very conversant in including again depreciation and normally such addbacks are kosher. Buildings have a tendency to understand or not less than preserve worth over time so the accounting depreciation is just not an actual expense.

On this case, nevertheless, that is the non-real property portion of depreciation and primarily associated to IRM’s automobile fleet. As everyone knows, autos lose a good portion of their worth the second they’re pushed off the supplier’s lot. Vehicular depreciation is an actual expense.

Thus, I’d subtract $49.5 million from AFFO.

There are additionally some improper addbacks to get to normalized FFO. Share based mostly compensation resurfaces as my perennial gripe.

Supplemental

Share compensation dilutes buyers making it an actual expense on this case to the tune of $18.3 million in 3Q23.

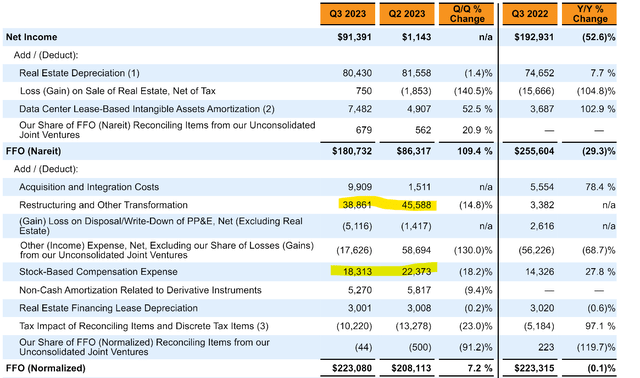

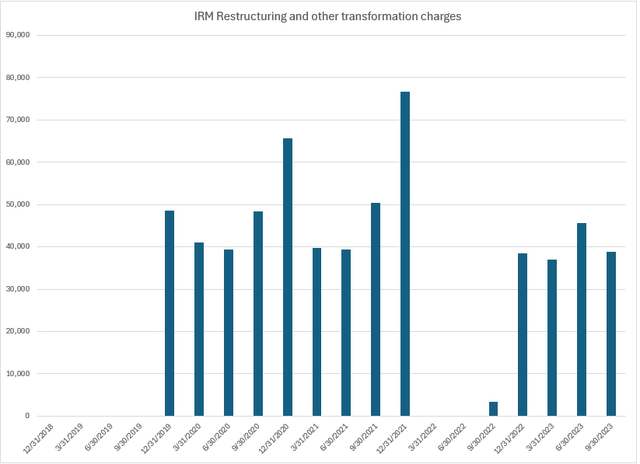

Lastly, we get to the restructuring and transformation prices of $38.8 million. Such prices are sometimes added again as a result of they’re considered as one time in nature. For Iron Mountain they appear a bit extra recurring to me.

S&P International Market Intelligence

This firm likes its transformations going from Undertaking Summit to Undertaking Matterhorn.

These restructurings do certainly make sense in the long run as IRM is leaning its operations, however on condition that this non-recurring expense has appeared in about 15 quarters I’d say it’s not less than partially recurring.

Thus, we are going to deduct $20 million from AFFO to get to true earnings.

In complete, changes are:

- -$18.3 million inventory comp

- -$20 million restructuring

- -$49.5 million non-real property depreciation

That takes AFFO for the quarter from $290 million to $202 million.

True AFFO runrate is about 70% of what’s reported which implies the a number of is considerably increased than 17X.

We calculate AFFO run charge at $2.78 which means a a number of of 24X.

Clear accounting

Please observe that whereas we don’t imagine reported AFFO is consultant of true earnings, there may be nothing improper about it being reported on this vogue. This can be very normal for firms to have their very own AFFO calculations as it’s a non-standardized metric.

Comparable changes would must be made for any firm. IRM absolutely discloses all line gadgets and makes it very clear how it may be reconciled to GAAP numbers. To my data IRM’s accounting is 100% clear.

Iron Mountain’s Inventory Valuation

Presently, the typical REIT trades at 15.9X 2024 AFFO.

Sure traits lend themselves to sure multiples. REITs that commerce above the typical a number of ought to have superior progress, decreased threat or some mixture of the 2.

Thus, to justify IRM’s 24X a number of on true earnings, it might must have these traits.

Its progress charge is certainly above common in my base case state of affairs which is regular reasonable progress within the RIM enterprise together with fast progress from information middle growth.

On the danger aspect, nevertheless, I see IRM as above common threat for 3 causes:

- Knowledge facilities are topic to oversupply given pretty low barrier to entry.

- Whereas not my base case, there’s a materials likelihood that paper may nonetheless go away which might gradual and even trigger unfavorable progress in RIM.

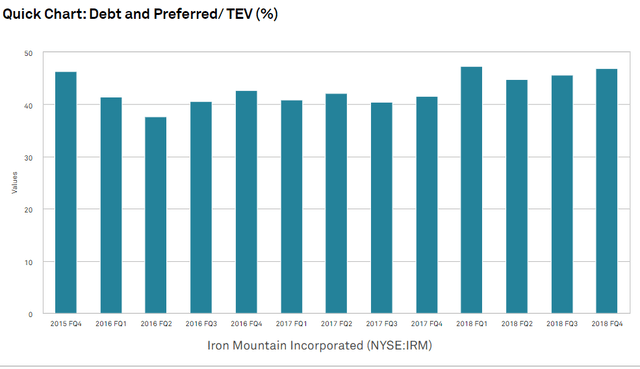

- Excessive leverage

IRM, in contrast to most REITs, doesn’t personal a good portion of its properties. On prime of a standard quantity of REIT leverage, they’ve lease obligations which take total liabilities to almost 50% of enterprise worth.

S&P International Market Intelligence

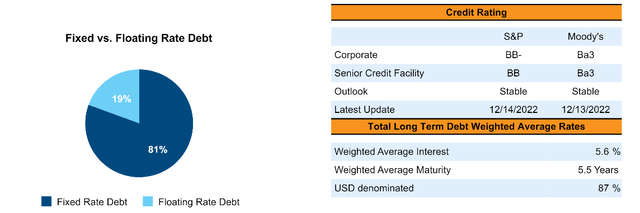

This increased degree of leverage comes with a worse credit standing (BB- on company) and better curiosity expense at 5.6% common price of debt.

IRM

Wanting on the mixture of barely above REIT progress charge and above REIT common threat, I believe IRM ought to commerce roughly in-line with the REIT common a number of.

On the present run-rate, IRM is buying and selling at 24X AFFO which is a bigger premium than I believe is warranted.

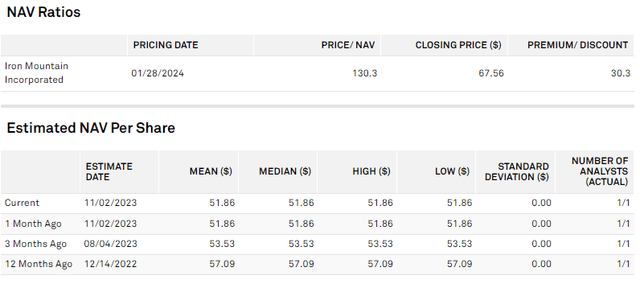

IRM additionally appears overvalued from an NAV perspective. In an setting the place most REITs are buying and selling considerably discounted to web asset worth, IRM is at 130% of NAV.

S&P International Market Intelligence

The bear thesis

Whereas Iron Mountain stays a well-managed firm with important progress potential, the large rise in its market worth has made it overvalued. If and when IRM’s valuation comes again right down to Earth, I’d fortunately think about shopping for again in.

{kind=link}