Jecapix/E+ through Getty Pictures

Mounted-income methods for retirement or life planning functions sometimes must contain investment-grade securities reminiscent of authorities bonds or high-quality company bonds. The plain purpose is that you just need to management danger to the extent attainable, whereas additionally having quantity of visibility into your whole returns. Inside this basket, authorities bonds are sometimes thought of to be the least dangerous, however the returns could also be subdued in comparison with higher-yielding securities that additionally add a modicum of credit score publicity.

One of many methods to supply a rising and ongoing earnings stream is to create bond ladders with U.S. Treasury securities, and one of many constructing blocks for that is the iShares iBonds Dec 2024 Time period Treasury ETF (NASDAQ:IBTE).

Utilizing treasuries is a (comparatively) low-risk choice, and the benefit right here is that quite a lot of the period danger is mitigated by the laddered construction. In different phrases, you’ll be able to management how a lot to put money into what a part of the yield curve, and you’ll commerce these ETFs like shares. Since there’s no rebalancing completed on these ETFs (it’s not an actively managed fund), you may have extra management.

Find out how to Play IBTE with its ‘Rung Siblings’

A bond ladder is an easy however (I feel) sensible strategy to construction the fixed-income element of your portfolio. It includes buying a collection of fixed-income securities from the identical issuer that matures in a calculated cadence over numerous durations, sometimes years however you can even construct a lot shorter ladders relying in your particular projected monetary wants sooner or later. The bottom ‘rung’ is the bond that matures first, the second is the next-longest-duration bond, and so forth.

Graph Created by Creator, Knowledge from U.S. Division of the Treasury

For instance, to construct a 10-year bond ladder, you’d cut up your funding into equal or unequal components and make investments every portion in a single specific period of bonds. It may be bottom-weighted, top-weighed, intermediate-weighted, barbell-weighted, or every other mixture you like, however the concept is to maintain including one rung on prime of one other to create a nearly perpetual ladder that finally helps you meet all of your monetary targets.

At this level, I don’t need you to imagine that IBTE represents short-term bonds as a result of that might be deceptive. Keep in mind that, on the time of the fund’s inception (Feb 25, 2020), we had been in a low rate of interest setting. Which means IBTE now holds bonds that might have had maturity dates 4 to 5 years into the long run, which is the place we’re at now. For this reason you’ll see a a lot decrease lifetime of fund whole return of simply 0.62%. The treasury yield curve was a lot flatter with a extra conventional construction – low short-duration yields and better long-duration yields.

U.S. Division of the Treasury

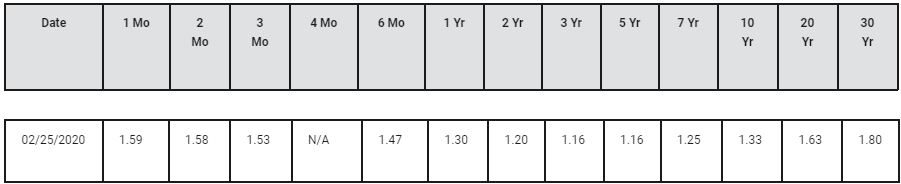

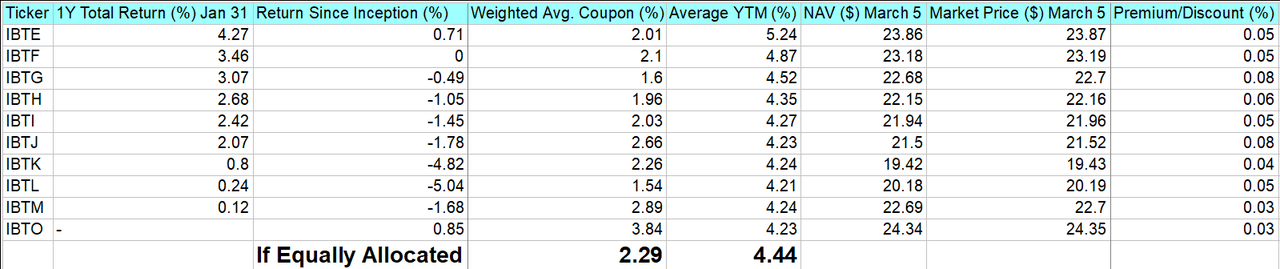

However, IBTE’s efficiency this previous 12 months has been fairly stable, which is why you’ll see a decrease weighted common coupon of two.01% however a better common YTM of 5.42% (as of March 4, 2024.)

Persevering with with our ladder construction, when the primary rung of bonds is liquidated, you’re taking the end-date distribution – or your share of the fund’s absolutely liquid NAV – and create one other rung on the prime of your ladder. Alternatively, you should purchase extra of the best-performing bonds and maximize your return for that exact maturity interval. It’s a good way to plan for a significant life occasion, create a month-to-month money move for private bills, or arrange a gradual earnings stream for whenever you retire. The one caveat is that when you take the common distributions, that YTM goes to be fairly a bit ‘off’. The reason being that yield to maturity, by definition means you not solely maintain the safety till it matures but in addition that you just reinvest all interim coupon funds.

It’s just a little extra difficult if you need to do it your self, which is what makes these sub-families of ETFs a handy strategy to reproduce what a extra seasoned investor may create with the precise underlying bonds.

IBTE Holdings Defined

Since that is the primary rung of your ETF bond ladder, it’s necessary to know that the fund holds bonds with maturity dates between January 1, 2024, and December 31, 2024. As these bonds mature, the fund will see its portfolio being regularly transformed to money and money equivalents that primarily provide you with cash market yields – proper now, that’s about 5.3%, however that’s not the “regular” cash market yield. Extra about that later.

On termination, which is “on or about December 15” per the December 31, 2023 reality sheet, the fund shall be absolutely liquidated and current buyers (ETF shareholders) will every obtain an quantity equal to the NAV per share multiplied by the variety of shares held, web of the fund’s liabilities. The ETF is delisted and ceases buying and selling, and also you get an quantity which may be greater or decrease than your preliminary price foundation. As of March 1, 2024, the fund reported 0.42% of its holding within the BCF Treasury Fund with an SEC (7-day) yield of 5.29%, and of notice right here is that the ETF will incur greater bills and costs as that share will increase by the 12 months earlier than it hits full liquidation at fund termination.

Understanding the Good and the Unhealthy of Bond Laddering Vis-a-Vis Curiosity Charges

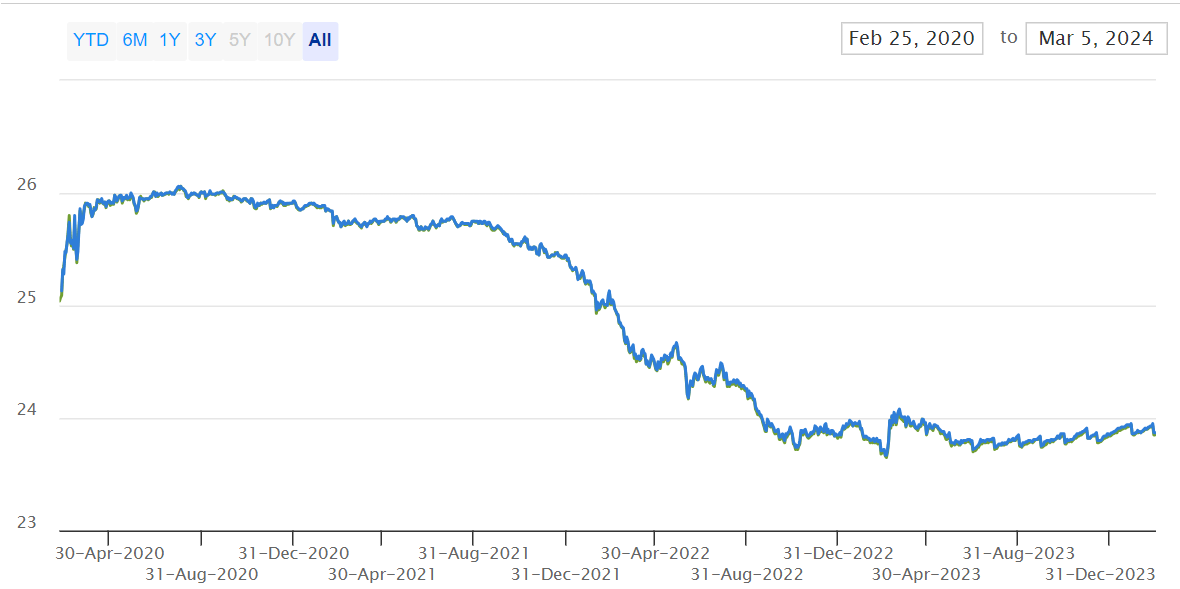

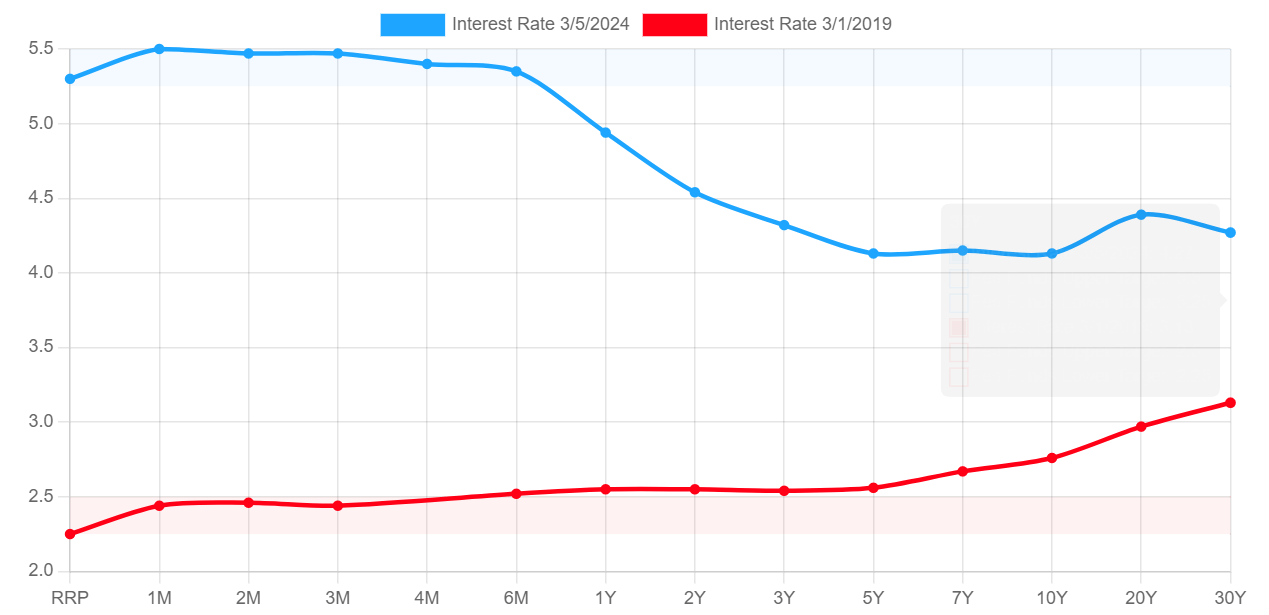

Bond ladders are primarily a approach to make sure a set earnings sooner or later from investments made at this time. Since bond costs have an inverse relationship with prevalent Fed rates of interest, you’ll discover that the majority older bonds shall be buying and selling properly under their unique NAVs proper now, as are IBTE’s holdings. In different phrases, they’d have been dearer within the low-rate state of affairs that has lasted till the Fed began QT in 2022. In truth, the Fed’s cadence of accelerating rates of interest are obviously seen within the NAV per unit of the fund since its inception.

iShares

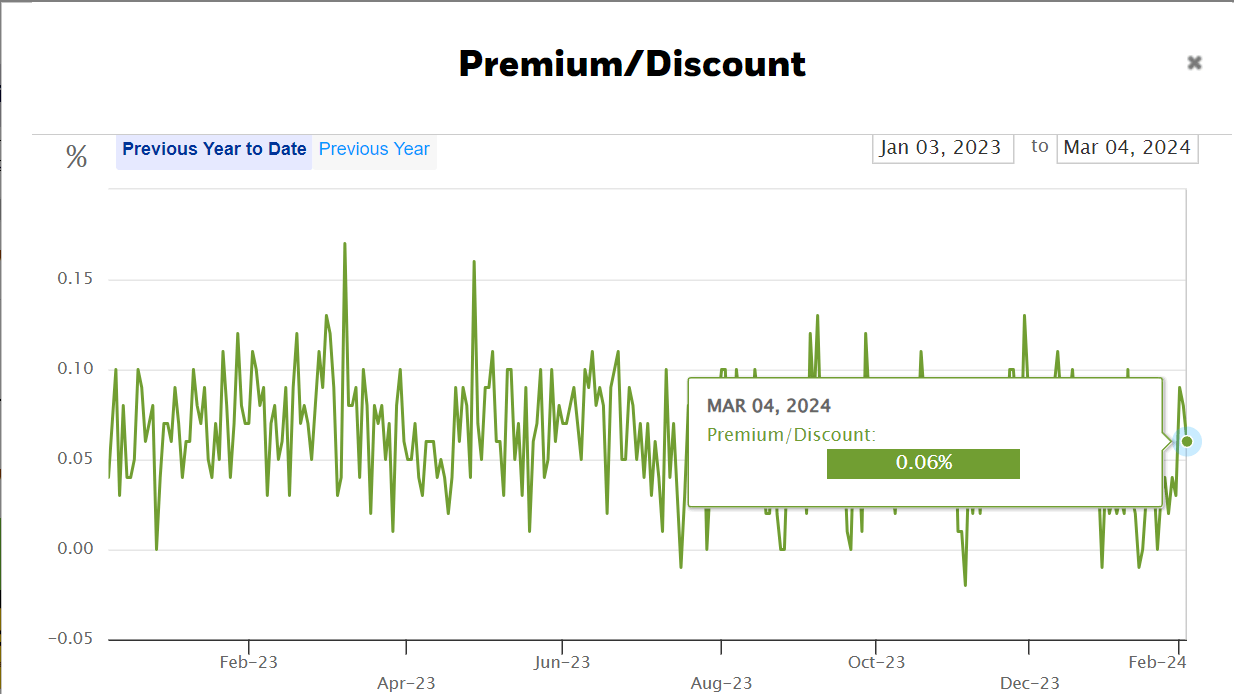

Nevertheless, when you have a look at the graph under, you’ll see that the shares have solely been buying and selling at a slight premium to NAV almost all the time for the reason that starting of 2023.

iShares

The benefit is that you just’ll be paying much less now than buyers within the ETF would have paid in 2020, and that’s primarily as a result of the way in which bond ETF shares are created and redeemed, to not point out arbitrageur exercise, the differential between the underlying NAV and the market value is stored minimal, and you’ll see this from the chart above – the ETF’s premium to NAV has not often been above 0.15%, with the present distinction being a 0.06% premium to NAV. The ancillary advantage of decrease acquisition costs is clearly greater yields, which we noticed from the 1Y efficiency of this ETF.

The second benefit, which can be associated to NAV erosion, is that, due to the still-high rates of interest, the bonds that mature over the 12 months (which are then put into cash market funds just like the BCF Treasury Fund) offers you greater yields, which, once more, is another reason the fund’s current efficiency has been unusually sturdy. If rates of interest persist at these ranges this 12 months, your YTM must be pretty near the 5.42% we noticed earlier. We don’t know this for certain, however that is the probably end result.

Now that we’ve seen the benefits, let’s have a look at the potential draw back.

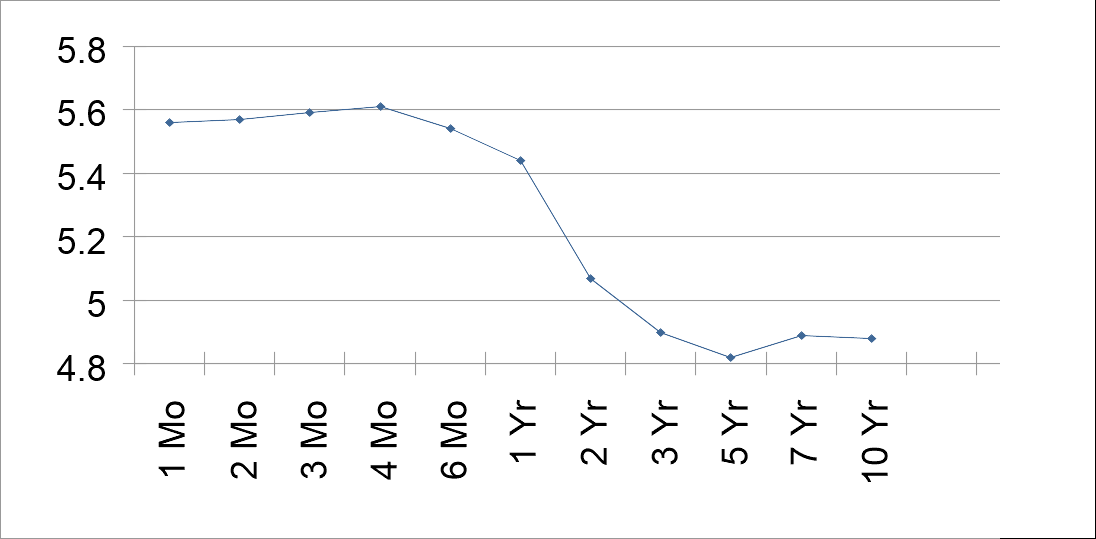

The principle drawback of constructing a bond ladder now could be that the yield curve is closely inverted (blue line). Which means you’ll get greater yields from the shorter-duration bonds in your ladder, however you’ll even be reinvesting your coupon distributions at more and more decrease yields on the prime of the ladder.

TreasuryYieldCurve.com

In different phrases, within the ‘greater for longer’ rate of interest setting that we appear to be caught in for now (blue line within the graph above), your 5Y to 10Y yields will depart quite a lot of returns on the desk.

The opposite danger is that if rates of interest begin dropping quickly this 12 months and the yield curve begins to return to normalcy. Since longer-duration bonds’ costs are extra delicate to price adjustments, the securities with far-dated maturities – or the highest of your ladder – will have a tendency to maneuver down extra aggressively as a result of, as we noticed, bond costs correlate inversely to rate of interest adjustments.

That’s a damaging, however it additionally means you’ll have the ability to lock in higher long-dated NAVs as you add extra rungs to your ladder if that occurs. I don’t suppose that’s probably as a result of the economic system has been sending combined messages for almost a 12 months now, the final opinion appears to be that the Fed received’t be as aggressive in reducing charges because it was in rising them.

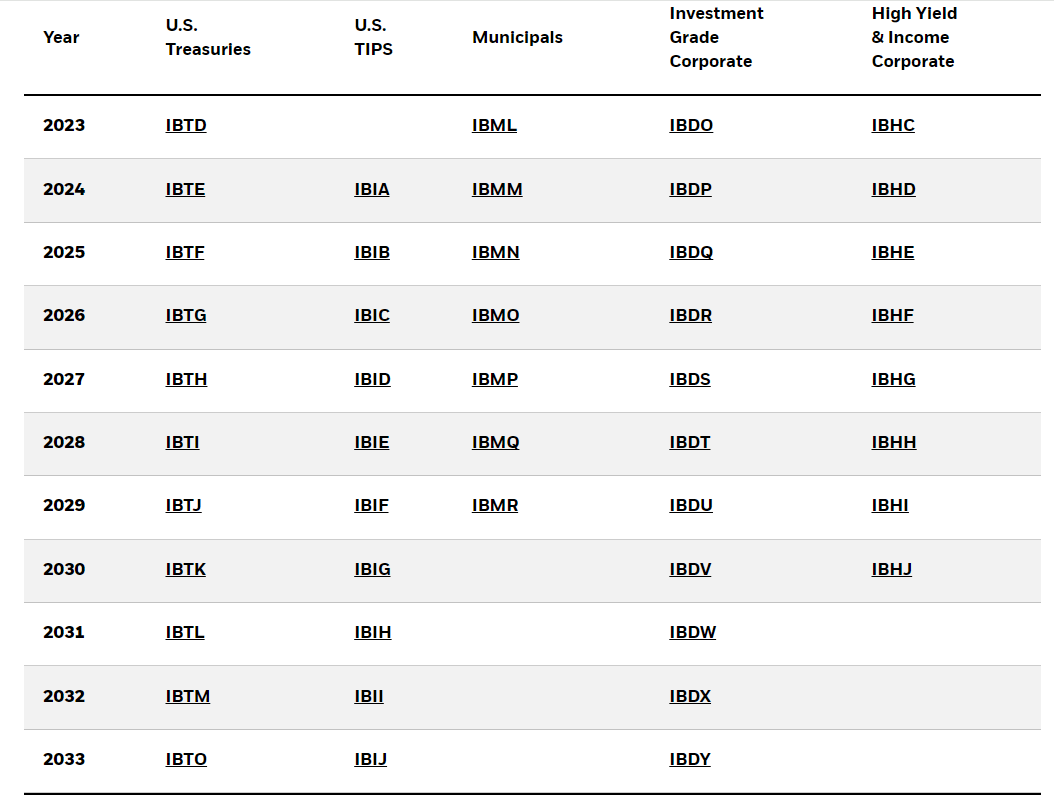

Now, let’s have a look at what a full iShares iBonds ETF ladder would seem like and what common coupon and YTM you’d be locking into when you make investments now in a full 10-year ladder with the rungs maturing yearly.

Implications for Buyers

Wanting on the professionals and cons, what this implies for bond ETF buyers is that they’ll want to maneuver rapidly to lock in to greater yields for all the ladder construction. For those who have a look at the graph above, below low rate of interest circumstances (pink line) your long-dated yields are nonetheless comparatively a lot decrease than they’re now – they’re greater than short-duration bonds can be, however nonetheless rather a lot decrease than what they’re now. That additionally means they’ll be pricier – because of the inverse correlation between a bond’s value and its yield. Briefly, that is the fitting time to construct your bond ETF ladder.

Coming again to IBTE as the primary rung of your ladder, let’s have a look at the typical YTMs throughout all the ladder, which includes all the collection at present being provided by iShares.

iShares iBonds ETFs throughout danger tolerance ranges – iShares Web site

Since we’re solely speaking a couple of bond ladder with the bottom relative dangers related to it because of the treasury holdings, we’ll be concentrating on the second column displaying the IBT collection. Let’s have a look at every of their traits to see how your bond ladder may carry out on common.

Knowledge from In search of Alpha and iShares Web site as of March 5, 2024

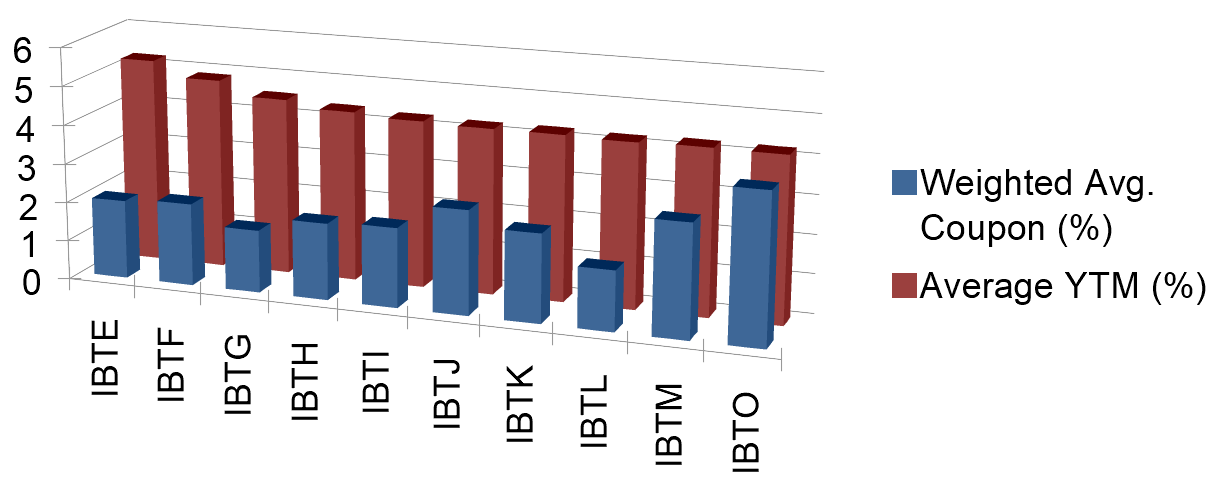

As you’ll be able to see, allocating your funding equally throughout this ETF sub-family ought to provide you with these averages. The YTM common seems enticing, and until you’re including new rungs to the ladder at a lot decrease coupon charges, that ought to maintain regular over time.

Knowledge from In search of Alpha and iShares Web site as of March 5, 2024

To Summarize…

Constructing bond ladders needn’t be a fancy or cumbersome train when you use a ready-to-order construction provided by and managed by a number of the most well-recognized names within the area, which BlackRock, the fund’s supervisor, represents. Which means dependable coupon funds which are essential to optimizing YTM, however you’ll must arrange the reinvestments your self. Nonetheless, it’s rather a lot simpler than having to overview tons of bonds earlier than selecting the most effective ones to populate your ladder with.

The one caveat I’d add right here is that any funding comes with some quantity of danger, even an funding in U.S. treasuries. There are additionally rate of interest dangers we talked about, period dangers ({that a} ladder construction mitigates to a big diploma), and liquidity dangers, which you sometimes shouldn’t face with a well known model like iShares. However, you want to pay attention to the varied sorts of dangers concerned. I’d extremely recommend going by all of the literature that the fund places out so that you’re well-versed in these dangers.

I want you all the most effective as you create a financially safe future for you and your family members!

{kind=link}