Andres Victorero

Creator’s notice: This text was launched to CEF/ETF Revenue Laboratory members on April twenty sixth.

The Excessive Yield ETF (NYSEARCA:HYLD) affords traders a robust, above-average, fully-covered 7.9% dividend yield, with the potential for reasonable progress. Because the fund focuses on high-yield bonds, dangers are above-average, and losses may mount if a recession happens. The fund is a purchase, however typically inappropriate for extra conservative earnings traders and retirees.

HYLD – Fundamentals

- Funding Supervisor: MacKay Shields

- Expense Ratio: 1.29%

- Dividend Yield: 7.86%

HYLD – Overview

HYLD is an actively-managed ETF, investing in U.S. high-yield company bonds. It’s administered by MacKay Shields, an funding agency specializing in personal credit score and fairness. HYLD appears to be their solely retail product.

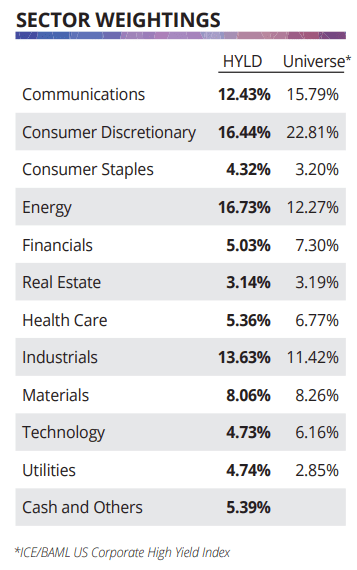

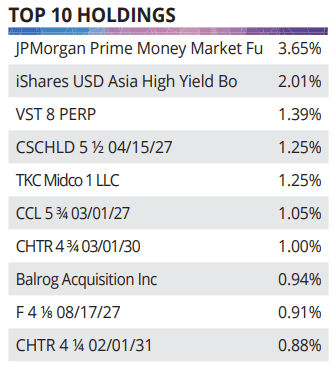

HYLD invests in 285 totally different securities, specializing in particular person bonds, however with small funding in bond funds and money. Holdings are diversified throughout industries and issuers.

HYLD HYLD

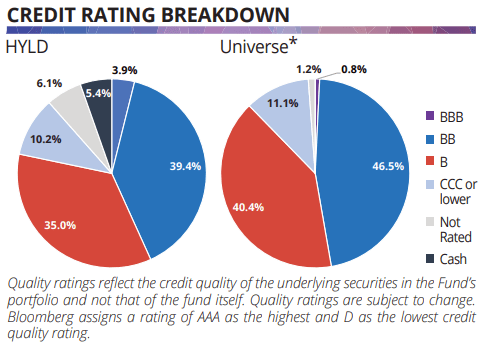

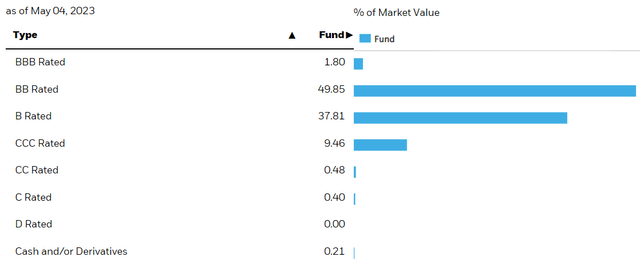

HYLD focuses on high-yield company bonds, with these accounting for nearly all the fund’s property. Securities rated BB – B predominate, with a mean credit standing of B. These are comparatively dangerous, high-yield securities.

HYLD

HYLD is an actively-managed fund, and so fund technique, holdings, and efficiency, are all considerably depending on administration selections, capabilities, and execution. These are all notably necessary within the high-yield area, as these securities are dangerous, and avoiding, or lowering, defaults is usually fairly impactful.

HYLD’s technique and holdings have a number of necessary advantages and downsides. Let’s take a look at these, beginning with the advantages.

HYDL – Advantages

Sturdy 7.9% Dividend Yield

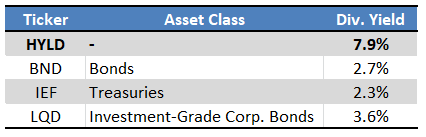

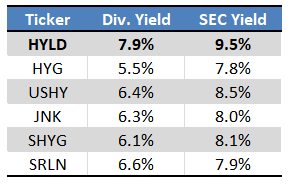

HYLD’s holdings are comparatively dangerous, but additionally comparatively high-yielding, with the fund itself sporting a 7.9% dividend yield. It’s a sturdy yield on an absolute foundation, and far greater than that of different bond sub-asset lessons.

Fund Filings – Chart by Creator

Extra importantly, HYLD’s dividend yield is greater than 2.0% greater than that of the business benchmark, the iShares iBoxx $ Excessive Yield Company Bond ETF (HYG), and round 1.5% greater than that of its friends. The identical is true for the fund’s SEC yield, which measures its short-term era of earnings.

Fund Filings – Chart by Creator

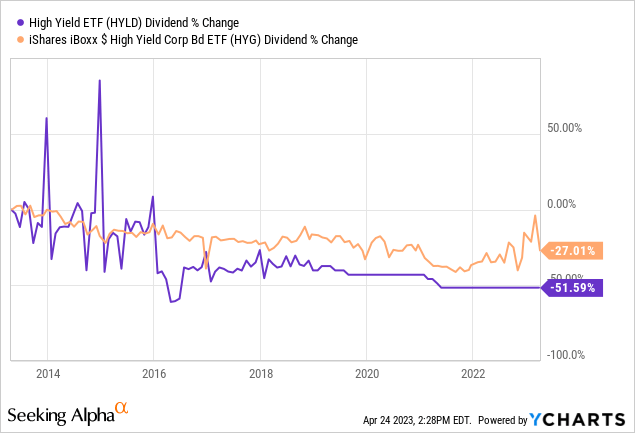

HYLD’s dividends are additionally greater than fully-covered by its underlying era of earnings, as evidenced by its SEC yield. As HYLD is actively-managed, the fund’s dividends are at greater danger than implied by these figures, as administration may all the time mismanage the portfolio, or change it in order to cut back its earnings / yield. This was considerably the case in prior years, as evidenced by the fund’s constant, important, above-average dividend cuts.

Knowledge by YCharts

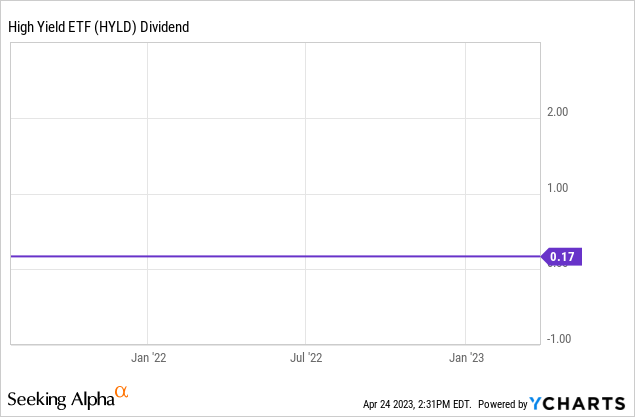

However the above, I imagine that HYLD’s dividends are protected proper now, as SEC’s yield do not lie, and as dividends have remained secure since mid-2021. The long-term dividend track-record is sort of mediocre, however the state of affairs does appear materially improved.

Knowledge by YCharts

HYLD’s sturdy, above-average, fully-covered 7.9% dividend yield is the fund’s most important profit, and its core funding thesis.

Dividend Development Potential

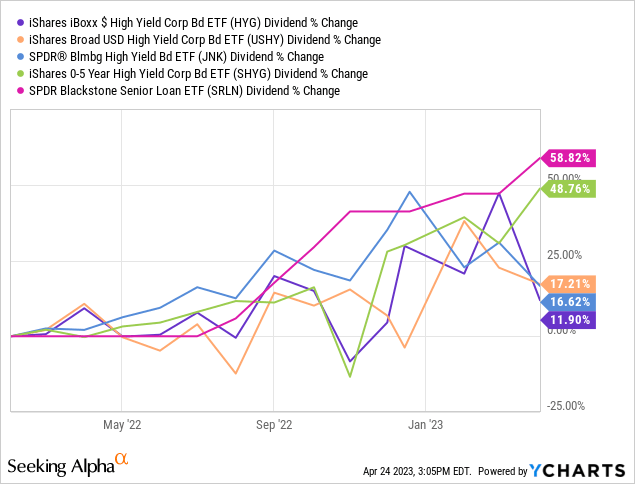

Rates of interest have risen since at the very least early 2022, resulting in greater charges on most bonds, and better dividend yields on most bond sub-asset lessons. Excessive-yield company bond fund dividends have grown too, within the overwhelming majority of circumstances.

Knowledge by YCharts

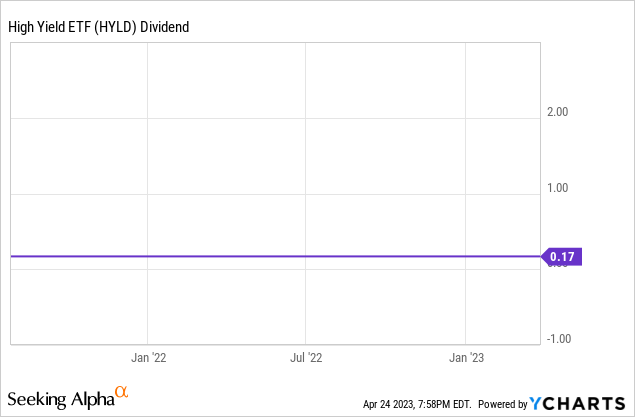

One exception to the above is HYLD, which has paid the identical in dividends since mid-2021.

Knowledge by YCharts

Though HYLD’s dividends haven’t elevated, the fund’s underlying era of earnings virtually actually has. Rates of interest have risen throughout the board, and the fund’s SEC yield itself is sort of excessive, so greater earnings is sort of sure, though dividends haven’t elevated. Beneath these situations, I imagine that dividends will see sturdy progress shifting ahead, though that is, after all, depending on future market situations, and future Fed coverage. Nonetheless, optimistic dividend progress appears fairly doubtless, for my part at the very least.

HYLD’s sturdy 7.7% dividend yield, and its potential for optimistic dividend progress, makes for a stable funding thesis.

HYLD – Drawbacks

Excessive Credit score Threat

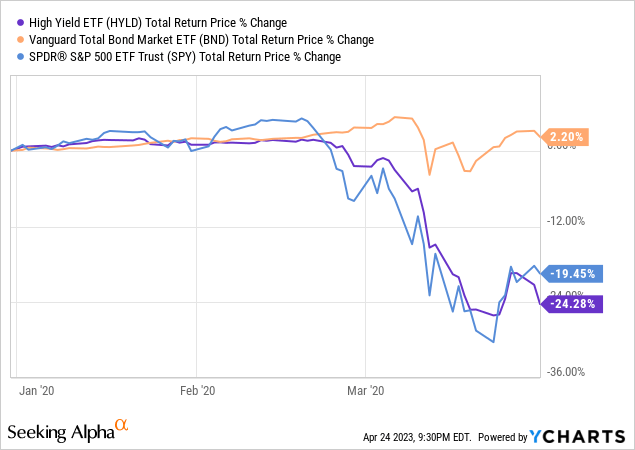

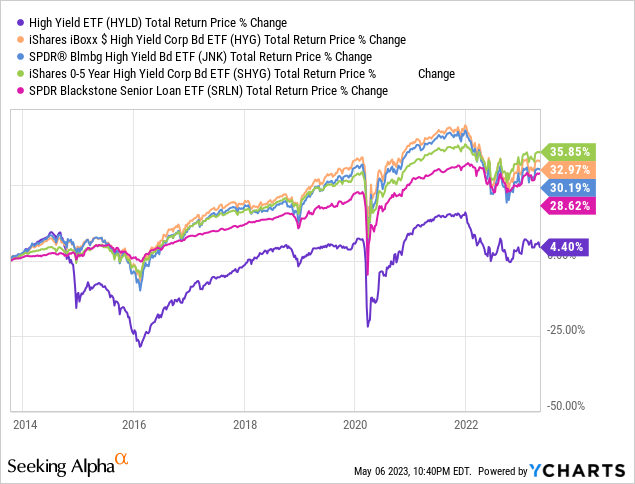

HYLD focuses on high-yield company bonds, securities with very weak credit score scores. Default charges are greater than common, though typically low on an absolute foundation. Defaults are additionally strongly depending on financial situations and have a tendency to spike throughout recessions. Resulting from this, high-yield company bonds are inclined to underperform throughout recessions, as is the case for HYLD. For reference, the fund’s efficiency in 1Q2020, the onset of the coronavirus pandemic.

Knowledge by YCharts

HYLD’s holdings are a bit riskier than these of its friends, with the fund weighting BB-rated securities a bit decrease, B-rated securities a bit greater. A fast desk with HYLD’s and HYG’s credit score scores, to see the variations.

Knowledge by YCharts HYG

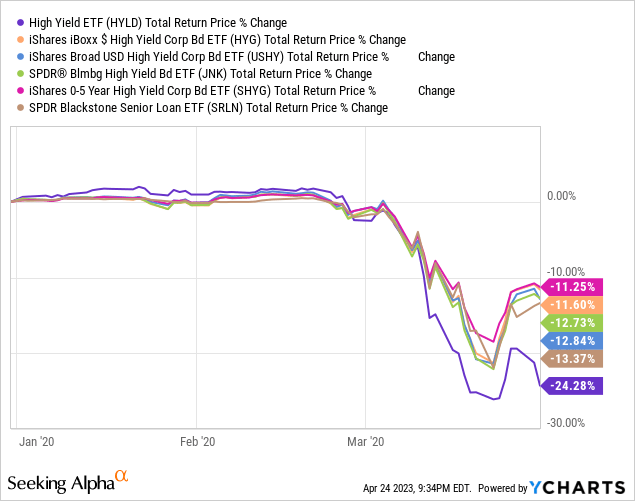

As HYLD’s credit score scores are a bit decrease than common, the fund needs to be a bit riskier, extra unstable than its friends. Anticipate the fund to underperform its friends throughout recessions, was the case in 1Q2020.

Knowledge by YCharts

HYLD’s dangerous holdings are a adverse for the fund and its shareholders, and a key drawback relative to its friends. Conservative, risk-averse traders may favor a few of its much less dangerous friends. Extra aggressive, yield-seeking traders may put up with these points as a result of fund’s sturdy yield.

Under-Common Efficiency Monitor-File

HYLD’s long-term efficiency track-record is sort of mediocre, with the fund considerably underperforming its benchmark, and most of its friends since inception.

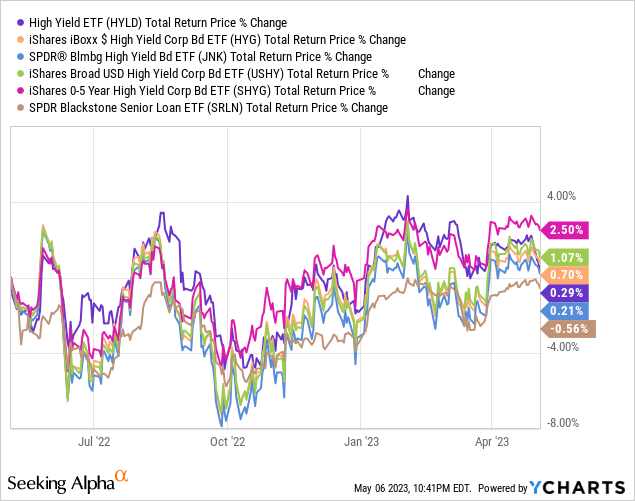

On a extra optimistic notice, HYLD’s underperformance is sort of fully concentrated in 2014 to 2016, with the fund performing in-line with its friends since. For reference, the fund’s efficiency these previous twelve months.

However the above, HYLD’s efficiency track-record stays below-average, at finest. I am keen to miss these points as a result of fund’s enchancment these previous few years, different traders won’t.

Excessive Expense Ratio

HYLD is an costly fund, with an expense ratio of 1.39%, in comparison with a mean of 0.25% – 0.50% for funds on this area. Bills immediately cut back returns and are all the time a adverse for traders.

In my view, and based mostly on HYLD’s holdings and efficiency, the fund is ready to generate a bit of additional yield, returns, and alpha, however a large portion of that is eaten up by charges. HYLD would have outperformed its friends with a decrease expense ratio, extra in-line with its friends.

HYLD – Why the Change in Thoughts

Final time I wrote about HYLD, in early 2022, I used to be a bit extra bearish. On the time, the fund’s complete return track-record was a bit weaker, with newer durations of losses and underperformance. HYLD’s dividend progress track-record was considerably weaker, with the fund seeing a number of latest dividend cuts. The fund’s dividends didn’t appear terribly protected both, as spreads have been narrowing, and earnings appeared weak.

Since then, HYLD’s efficiency has considerably improved, its dividends have stabilized, its underlying era of earnings has risen, and potential returns are greater. HYLD’s improved fundamentals brought about me to re-assess the fund, altering from a impartial to a purchase ranking.

Conclusion

HYLD’s sturdy, above-average, fully-covered 7.9% dividend yield, and potential dividend progress, make the fund a purchase.

{kind=link}