Printed on November 4th, 2025 by Felix Martinez

Excessive-yield shares pay out dividends which can be considerably larger than the market common. For instance, the S&P 500’s present yield is just ~1.2%.

Excessive-yield shares may be notably useful in supplementing revenue after retirement. A $120,000 funding in shares with a median dividend yield of 5% creates a median of $500 a month in dividends.

Hess Midstream LP (HESM) is a part of our ‘Excessive Dividend 50’ collection, which covers the 50 highest-yielding shares within the Positive Evaluation Analysis Database.

Now we have created a spreadsheet of shares (and intently associated REITs, MLPs, and so on.) with dividend yields of 5% or extra.

You possibly can obtain your free full listing of all securities with 5%+ yields (together with vital monetary metrics resembling dividend yield and payout ratio) by clicking on the hyperlink under:

Subsequent on our listing of high-dividend shares to overview is Hess Midstream LP (HESM).

Enterprise Overview

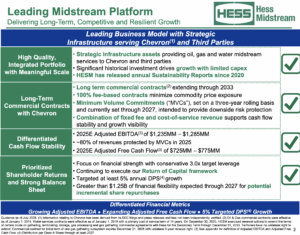

Hess Midstream LP is a growth-oriented midstream vitality firm that owns, operates, and develops infrastructure for crude oil, pure fuel, and produced water within the Williston Basin, together with the Bakken and Three Forks shale performs.

The corporate gives providers to Hess Company and third-party clients by way of three predominant segments: gathering pipelines, processing and storage services, and terminaling and export logistics. Its operations are primarily fee-based, offering comparatively steady income streams whereas supporting manufacturing in a key U.S. oil area.

Strategically, Hess Midstream leverages its built-in infrastructure footprint to seize regular money flows and pursue progress alternatives, together with acquisitions and expansions. The corporate additionally focuses on returning capital to shareholders by way of unit repurchases and distributions.

Nonetheless, it stays uncovered to commodity value fluctuations, regulatory pressures, and the capital-intensive nature of midstream tasks, which require cautious administration to take care of profitability and long-term progress.

Supply: Investor Relations

The corporate reported robust third-quarter 2025 outcomes, with internet revenue of $175.5 million and internet money offered by working actions of $258.9 million. Web revenue attributable to Hess Midstream LP was $97.7 million, or $0.75 per Class A share, up from $0.63 per share in the identical quarter of 2024. Adjusted EBITDA reached $320.7 million, and Adjusted Free Money Circulate totaled $186.8 million.

The corporate accomplished accretive repurchases of $70 million in Class A shares and $30 million in Class B items, whereas growing the quarterly money distribution to $0.7548 per Class A share, reflecting larger throughput volumes throughout fuel processing, oil terminaling, and water gathering.

Operationally, Hess Midstream expanded capability with a brand new compressor station offering 35 MMcf/d, and throughput volumes grew 10% for fuel processing and seven% for each oil terminaling and water gathering in comparison with the prior-year quarter. Income for the quarter rose to $420.9 million from $378.5 million, pushed by larger bodily volumes and tariff charges.

Working prices elevated modestly to $162.0 million, primarily resulting from larger worker prices, depreciation, and pass-through bills. The corporate’s revolving credit score facility had a drawn stability of $356 million, and its senior unsecured debt was upgraded by S&P to BBB-.

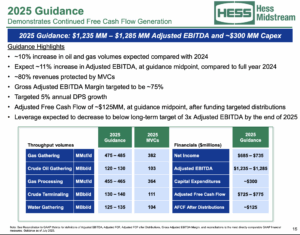

Wanting forward, Hess Midstream expects fourth-quarter 2025 internet revenue of $170–180 million and Adjusted EBITDA of $315–325 million, with full-year internet revenue steering of $685–695 million and Adjusted EBITDA of $1,245–1,255 million. Capital expenditures for the yr are revised to roughly $270 million, reflecting the suspension of the Capa fuel plant undertaking.

The corporate stays centered on fee-based progress, operational effectivity, and returning capital to shareholders whereas managing the capital-intensive nature of midstream operations and publicity to commodity value fluctuations.

Supply: Investor Relations

Progress Prospects

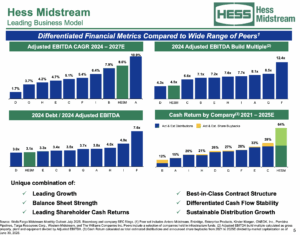

Hess Midstream has robust progress potential pushed by secular growth in pure fuel seize and regular manufacturing will increase from Hess’s upstream operations. The corporate expects fuel and oil volumes to develop about 10% yearly by way of 2026 and over 5% in 2027.

Mixed with annual payment hikes linked to inflation, this helps projected EBITDA and free money stream progress of greater than 10% per yr, positioning the corporate for constant operational growth.

Financially, Hess Midstream is bettering leverage, with Web Debt to EBITDA anticipated to fall under 2.5x by the tip of 2026.

This helps a focused annual distribution progress of at the least 5% by way of 2027. Analysts undertaking 6% common annual earnings-per-share progress and practically 5% annual distribution progress over the following 5 years, highlighting the corporate’s potential to ship steady money returns and long-term shareholder worth.

Supply: Investor Relations

Aggressive Benefits & Recession Efficiency

The corporate advantages from a number of aggressive benefits that assist its stability and progress. Its built-in infrastructure within the Bakken and Three Forks shale performs gives important midstream providers—gathering, processing, storage, and terminaling—to Hess and third-party producers, making a fee-based income mannequin that’s much less delicate to commodity value swings.

Lengthy-term contracts, annual payment escalators tied to inflation, and strategic capability expansions, resembling new compressor stations, additional strengthen the corporate’s market place and operational reliability.

The corporate has demonstrated resilience throughout financial downturns and intervals of commodity volatility. Its predominantly fee-based construction, coupled with regular throughput progress and diversified service choices, permits Hess Midstream to take care of money stream and distributions even throughout recessions.

Analysts view the corporate’s constant earnings progress, conservative leverage profile, and disciplined capital administration as key components that assist it maintain efficiency and shareholder returns below difficult market situations.

Dividend Evaluation

The corporate’s annual dividend is $3.02 per share. At its current share value, the inventory has a excessive yield of 8.8%.

Given the corporate’s 2025 earnings outlook, EPS is predicted to be $3.10 per share. In consequence, the corporate is predicted to pay out 97% of its EPS to shareholders in dividends.

Remaining Ideas

Hess Midstream usually goes unnoticed by buyers resulting from its comparatively typical enterprise mannequin, however it’s well-suited for income-focused and value-oriented buyers.

The inventory is projected to ship a median annual return of 18% over the following 5 years, supported by an 8.8% distribution yield, 6% earnings-per-share progress, and a 3.3% valuation tailwind. Total, the inventory is assigned a maintain ranking.

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}