andreswd

Funding motion

I advisable a purchase score for Well being Catalyst (NASDAQ:HCAT) after I wrote about it the final time (14 Nov 2023), as I anticipated, HCAT to come back out as a stronger enterprise with a greater profitability profile as administration executes on their progress methods. Primarily based on my present outlook and evaluation of HCAT, I like to recommend a purchase score. I’m assured that HCAT can meet administration’s FY28 steering, producing >$100 million in EBITDA. As HCAT reveals proof of reaching that through the years (e.g., increasing margins), valuation ought to begin to rerate upwards to friends’ ranges.

Assessment

HCAT reported 4Q23 income progress (on 23 Feb 2024) of 9% to $75.1 million, coming in on the high finish of the guided vary of $70.1 to $75.1 million. By phase, know-how income grew 5% to $47.1 million, {and professional} companies income grew 14% to $27.9 million. Adj gross revenue got here in at $34.7 million, translating to margins of 46.2%, which was down 450 bps as a result of gross margin contraction at Expertise (down 215 bps to 66.6%) and Skilled Providers (down 584 bps to 11.8%). As for adj. EBITDA, it got here in at $1.4 million, according to steering of $0.3 to $2.3 million.

I imagine the outcomes have been nice, and the outlook for HCAT stays constructive. The drop in share worth represents one other probability for traders to purchase the inventory at an affordable valuation once more. The macro backdrop has actually improved in comparison with 2023, particularly with the Fed reiterating its view to chop charges this 12 months. This could result in a greater spending atmosphere for the healthcare trade, which interprets to raised bookings for HCAT. On the micro degree, I proceed to be constructive about HCAT’s progress initiatives, particularly its TEMS providing and next-generation knowledge platform.

Concerning TEMS, I’m very constructive about this driving progress and margin growth. At its core, TEMS addresses plenty of vital points that purchasers face, reminiscent of outsourcing, monetary constraints and bills, and recruitment and retention. In the course of the investor day, chart abstraction was emphasised as one of many key options. Lowered time to extract knowledge per use case, in addition to prices and burdens related to knowledge assortment, are all advantages of HCAT’s resolution. By doing so, purchasers are free to deal with their sufferers and different stakeholders moderately than handbook extraction. The addition of AI makes this product even higher as a result of it has the potential to evolve into an much more environment friendly model. Administration claims that they anticipate a 24% discount in abstracting time on account of Chart Abstraction AI, which might result in financial savings in labor prices. Translating these again to monetary phrases, it means increased progress and margins. Concerning progress, since HCAT may also help prospects cut back the entire value of possession and enhance effectivity, I count on the adoption price to speed up. On margins, as a result of a bunch of handbook work is completed by way of AI, which suggests decrease labor prices per use case and human error, HCAT has develop into extra cost-efficient, and this makes the 25% margin run price goal much more believable. Lastly, with the tip market’s monetary scenario anticipated to enhance (as the price of capital comes down from price cuts), the adoption price of TEMS choices must also enhance.

The subsequent-gen knowledge platform is anticipated to bridge the hole between DOS and non-DOS buyer spending with its extra adaptable design. At current, HCAT counts over 500 non-DOS purchasers along with 100 DOS purchasers. Administration famous a big disparity within the amount of cash spent by the 2 teams, with DOS purchasers sometimes spending multimillions of {dollars} and HCAT and non-DOS purchasers spending just a few hundred thousand {dollars}. With this new platform’s elevated modularity and adaptability, HCAT can higher meet shopper wants; in different phrases, HCAT is ready to provide options that meet the wants of purchasers in the course of the spending capability spectrum. The subsequent-gen platform additionally makes it simpler for HCAT to include new capabilities as key efficiency indicators and functions are developed. Which means that HCAT can launch extra merchandise that can be utilized for cross-selling to its present buyer base, which will increase DBR.

Trying forward, I’m assured that HCAT can meet administration’s long-term steering of >$500 million in income by 2028 and $100 million in EBITDA, which equates to a 11% income progress CAGR over 5 years with 20% EBITDA margins. This successfully implies EBITDA progress of ~34% over the subsequent 5 years.

Valuation

Writer’s work

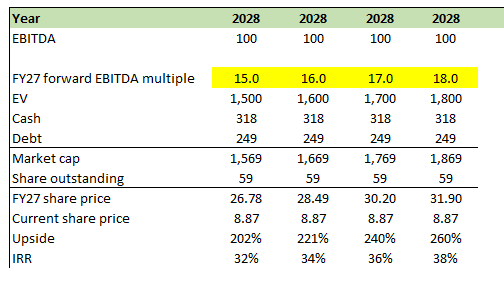

As I imagine HCAT is ready to obtain administration long-term (FY28) steering, the query is: what a number of ought to HCAT commerce at? To determine this out, I checked out different software software program corporations within the healthcare trade to get a way of the attainable vary of multiples. There are two key components to concentrate to right here: (1) anticipated income progress charges; and (2) margin profile. Primarily based on administration’s long-term steering, HCAT goes to develop to low teenagers for the subsequent 5 years and obtain an EBITDA margin of 20%. Utilizing these components, I zoomed down to three friends for HCAT due to their related focused viewers (healthcare corporations) and progress profile within the medium time period (2nd 12 months progress): Simulations Plus (SLP), Doximity (DOCS), and Evolent Well being (EVH). You’d discover that EVH trades at a decrease a number of regardless of increased progress, and that’s due to a decrease margin profile. I imagine it is a key motive for the present HCAT a number of as properly. Because it reveals that EBITDA margin can broaden, valuation ought to enhance to SLP and DOCS ranges. I’ve specified by my mannequin 4 multiples eventualities, and all of them present enticing IRR over the subsequent 4 years.

Observe that it is a completely different valuation methodology vs. my earlier mannequin that focuses on income progress. Now that we’ve got a EBITDA goal, I feel it makes extra sense to worth it base on earnings than income.

Writer’s work

Danger and ultimate ideas

A restoration in macro circumstances is kind of vital for HCAT FY24 efficiency. If the macro scenario worsens, spending within the healthcare trade goes to get additional pushed out to FY25/26. That is undoubtedly attainable, because the housing scenario within the US stays in an undersupply scenario. If the Fed cuts charges and inflation begins to surge once more, we might see one other spherical of price hikes.

I am reiterating a purchase score for HCAT regardless of the latest drop in share worth. I imagine HCAT’s TEMS providing and next-generation knowledge platform place them properly for future progress and margin growth. As such, administration’s long-term steering of exceeding $100 million in EBITDA by FY28 is achievable. A near-term catalyst is a possible price minimize by the Fed, which ought to drive an bettering healthcare spending atmosphere. As HCAT demonstrates its capacity to execute on its progress methods and broaden margins, its valuation ought to enhance to replicate its friends’ multiples.

{kind=link}