tadamichi

On this article, we make amends for the newest quarterly outcomes of the Golub Capital BDC (NASDAQ:GBDC). The corporate delivered a robust quarterly end result with a 4.8% complete NAV return. It trades at an 11.3% complete dividend yield and a 3 low cost to e-book. Its internet revenue yield is 12.5% – in keeping with the sector median however, arguably, overstated because of the one-off incentive price waiver.

Now we have maintained a Maintain ranking on the inventory – our earlier evaluation is linked right here. The valuation of the inventory has improved since then, which makes it marginally extra engaging.

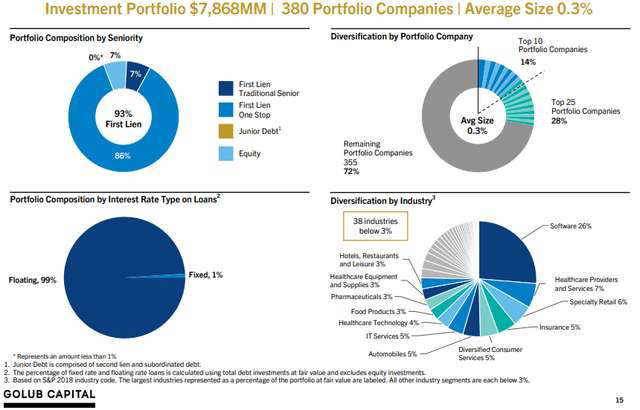

The corporate’s mortgage portfolio targets primarily floating-rate first-lien loans and may be very nicely diversified with 380 positions – greater than double the sector common. High sectors embrace software program and healthcare.

GBDC

Quarter Replace

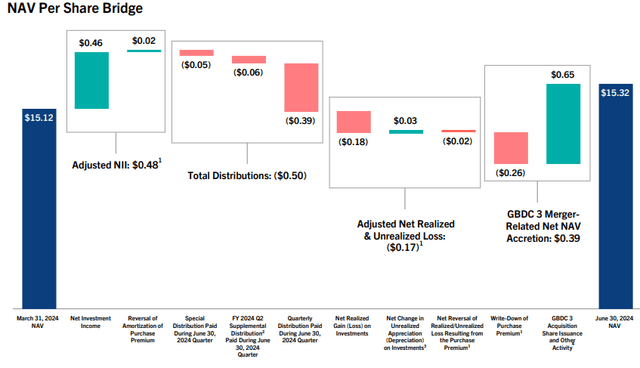

Adjusted internet funding revenue got here in at $0.48 – a 6% drop from the earlier quarter, primarily from the drop in leverage. As we additionally spotlight under, there was a one-off $0.07 enhance to revenue as the corporate made a one-off incentive price waiver as a consequence of two challenged investments. Absent the waiver, NII would have are available in practically 20% decrease from the earlier quarter.

Systematic Earnings BDC Device

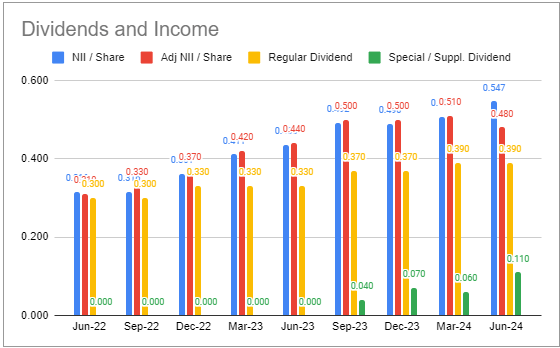

The corporate’s dividend construction is pretty difficult. It consists of a $0.39 base dividend, a supplemental of $0.05 in addition to a merger-related particular dividend of $0.05 (two remaining particular dividends can be paid 13-Sep and 13-Dec).

The NAV rose by 1.3%, nevertheless, 2.6% of that was as a consequence of merger-related accretion. In mild of a few challenged investments (Pluralsight and Imperial Optical) GBDC additionally made a one-time discretionary incentive price waiver which had a +$0.07 affect on internet funding revenue. Altogether, these components add as much as a 3% optimistic uplift on the NAV. Absent these one-off components, GBDC would have underperformed the median BDC in our protection for the quarter.

GBDC

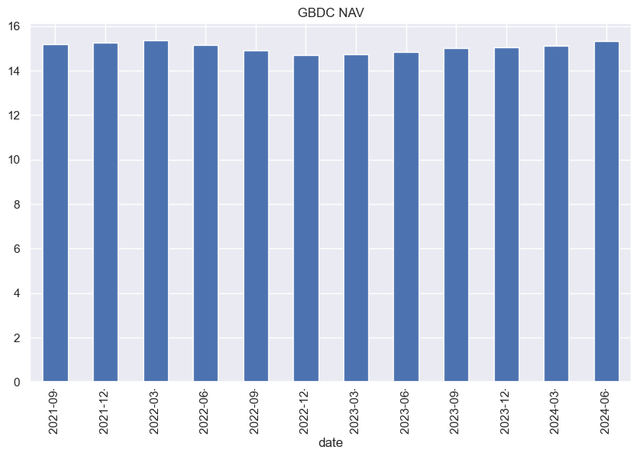

The NAV has risen for the sixth quarter in a row and has been secure over the past couple of years.

Systematic Earnings

Earnings Dynamics

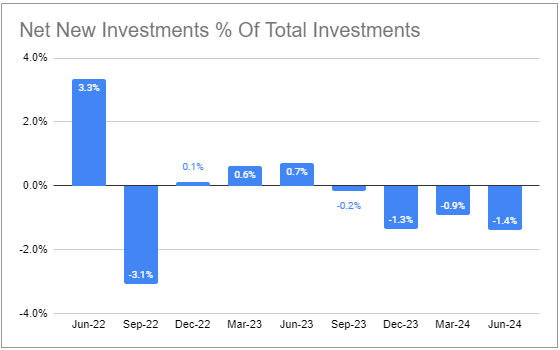

Web new investments had been down on the quarter.

Systematic Earnings BDC Device

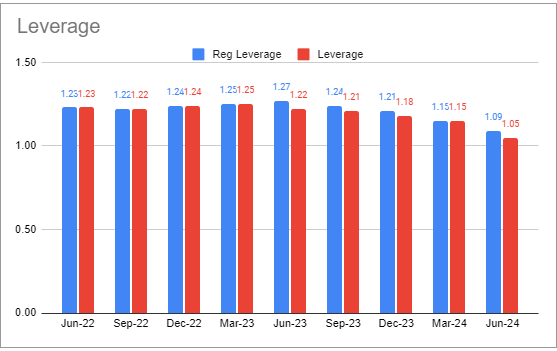

Leverage continued to fall – now standing under the sector common stage.

Systematic Earnings BDC Device

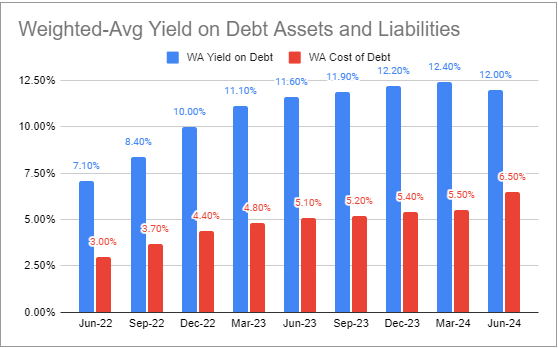

The weighted-average portfolio yield has been falling whereas curiosity expense has been rising, squeezing the yield unfold. That is just about what we’re seeing throughout the remainder of the sector, notably on the curiosity expense aspect.

Systematic Earnings BDC Device

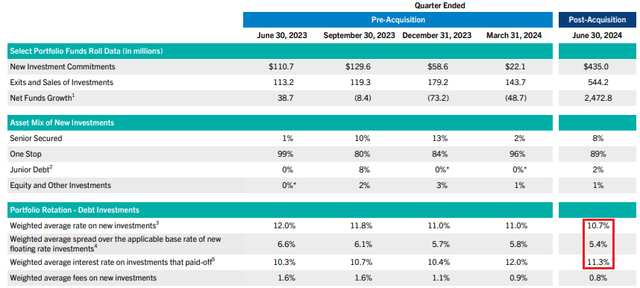

A part of the rationale for the drop in portfolio yield was the truth that new investments are coming into the portfolio at a decrease yield than repaid investments.

GBDC

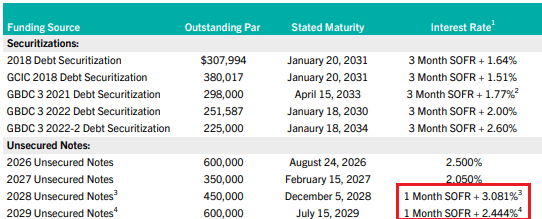

On the curiosity expense aspect, bonds that had been issued within the post-COVID low rate of interest interval are coming due. As an illustration, in April, the corporate redeemed its 3.375% bond. Its most just lately issued 2029 bond carries a swapped price of SOFR + 2.444% or a coupon of round 7.74% at at this time’s SOFR. Its mounted coupon was 6% at issuance.

GBDC has been swapping its just lately issued bonds – a development we’re seeing throughout the remainder of the sector as nicely. The swaps have raised at this time’s stage of curiosity expense because of the inverted yield curve, however the swapped bond curiosity expense will transfer decrease alongside short-term charges. The swaps will solely lower the lifetime curiosity expense on the bonds if short-term charges fall greater than what’s presently priced in by the market. With the swaps, BDCs are both taking the view that short-term charges will fall greater than anticipated, or they’re keen to commerce away at this time’s larger stage of curiosity expense for tomorrow’s extra secure internet funding revenue (as floating-rate liabilities higher match floating-rate property).

GBDC

The merger with GBDC made everlasting the inducement price discount to fifteen%, which is on the decrease finish of the BDC sector (incentive charges are likely to vary from 15-20%). All 4 parts of the corporate’s price construction are finest at school – the administration price, incentive charges, the hurdle price for the inducement price and the whole return lookback interval. This, together with its occasional shareholder-friendly price waivers, permits the corporate to generate a aggressive stage of internet funding revenue whereas holding lower-yielding property at a decrease stage of leverage. For instance, the corporate’s weighted-average portfolio yield is 12% vs the 12.4% median and its leverage is 1.05x – barely under the median stage, nevertheless its trailing-twelve month NAV yield is 13.3% vs. the 12.7% median in our protection.

Portfolio High quality

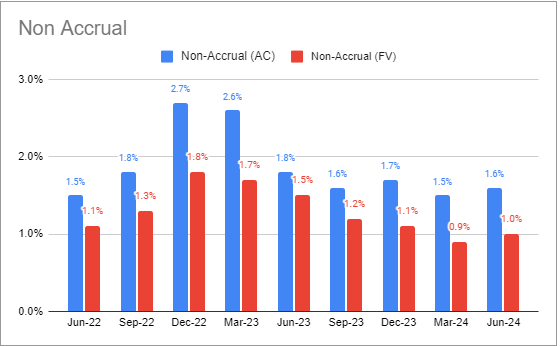

Non-accruals rose to 1% however stay under the median stage of 1.4% in our protection.

Systematic Earnings BDC Device

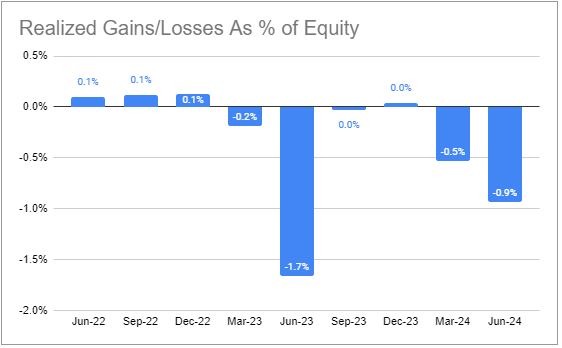

There was a large internet realized loss. The cumulative internet lack of 3% over the past 5 quarters bears watching.

Systematic Earnings BDC Device

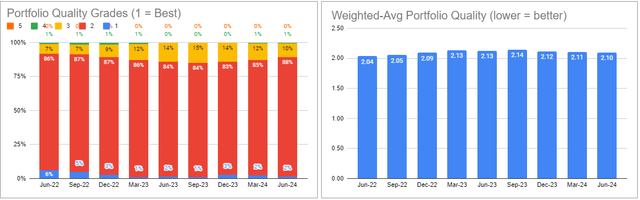

Portfolio high quality as gauged by inside scores improved barely.

Systematic Earnings BDC Device

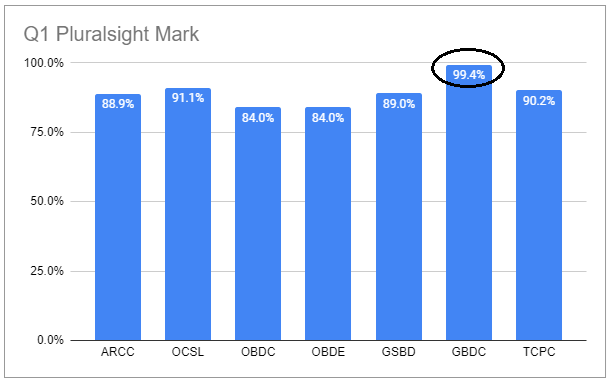

Pluralsight was one of many firm’s challenged positions within the quarter. Extra curiously, the scale of the mortgage grew in Q2 by about 30%. It’s attainable GBDC took over another person’s place. GBDC had probably the most aggressive mark for the Pluralsight mortgage in Q1 – a stage, which, frankly, places its marking methodology in query and one thing to control.

Systematic Earnings BDC Device

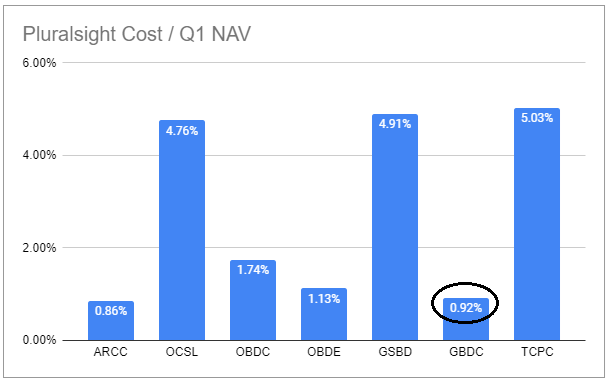

The place GBDC will get factors is in having a small allocation to the Pluralsight mortgage.

Systematic Earnings BDC Device

Valuation And Return Profile

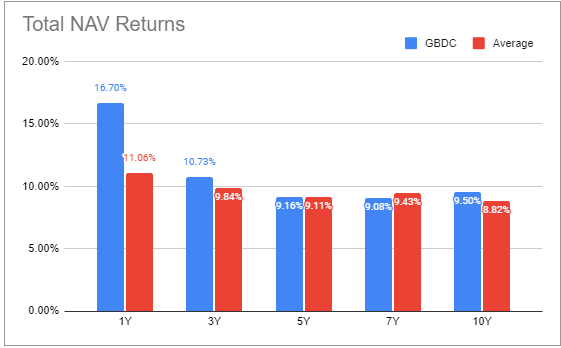

General, the corporate has been performing very nicely, notably over the past 1-2 years.

Systematic Earnings BDC Device

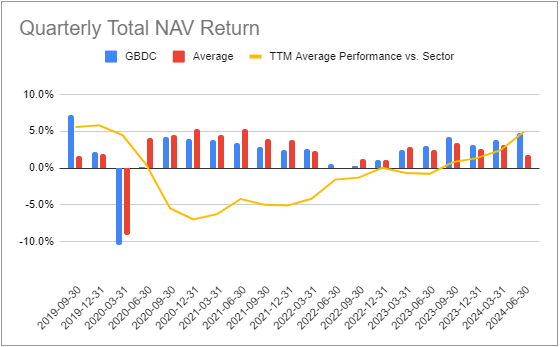

The underperforming streak got here to an finish round mid-2022.

Systematic Earnings BDC Device

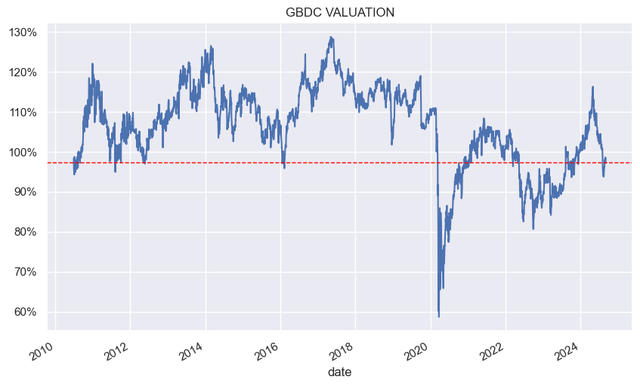

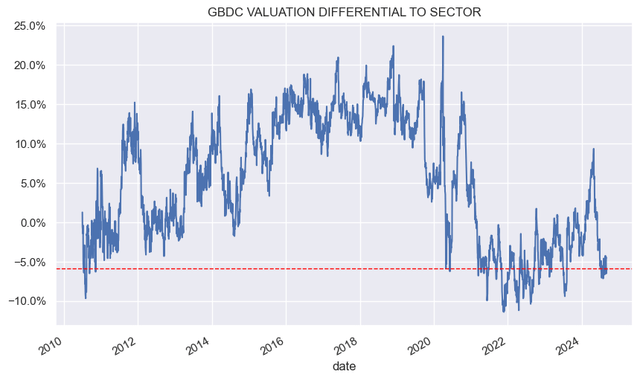

The corporate’s valuation has moved to a decrease plateau after COVID. This may increasingly have been because of the rights providing which had dangerous return optics with the massive NAV drop given the uplift from the train of the rights isn’t included within the NAV.

Systematic Earnings

The inventory continues to commerce at a reduction to the common valuation in our protection, although in keeping with the median BDC.

Systematic Earnings

Stance and Takeaways

GBDC stays a robust performer within the sector whereas buying and selling at a below-average valuation – a mix that we hunt down. Portfolio high quality has held up nicely, and its diversification and shareholder-friendly price construction are very engaging qualities. We preserve a place within the inventory in our Earnings Portfolios.

{kind=link}