Anthony Bradshaw

Flying excessive in August

Following a robust month-to-month enhance in July, gold posted one other wholesome acquire in August to complete 3.6% increased at US$2,513/oz. It additionally reached a brand new all-time on 20 August earlier than a really marginal decline into month finish (Desk 1).

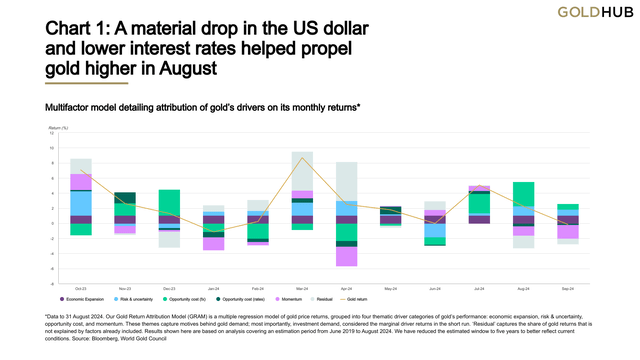

In response to our Gold Return Attribution Mannequin (GRAM), gold was pulled increased by a cloth drop within the US greenback and, to a lesser extent, decrease 10-year Treasury yields because the Fed signalled the time had come for charge cuts (Chart 1). The primary identifiable damaging contribution got here from a momentum issue, the gold return within the earlier month, i.e. when excessive, the next month usually sees a decrease return and vice versa.

Additionally of be aware in August, the numerous reduce in import responsibility on gold in India, which passed off in late July, has been a shot within the arm for gold demand within the nation. Anecdotal experiences counsel the responsibility discount was adopted by sturdy shopping for curiosity from jewelry retailers in addition to shoppers. In the meantime, world bodily backed gold ETFs prolonged their influx streak to 4 months. Western funds as soon as once more contributed the lion’s share of flows.

Chart 1: A fabric drop within the US greenback and decrease rates of interest helped propel gold increased in August

Multifactor mannequin detailing attribution of gold’s drivers on its month-to-month returns*

*Information to 31 August 2024. Our Gold Return Attribution Mannequin (GRAM) is a a number of regression mannequin of gold value returns, grouped into 4 thematic driver classes of gold’s efficiency: financial growth, danger & uncertainty, alternative value, and momentum. These themes seize motives behind gold demand; most significantly, funding demand, thought-about the marginal driver returns within the quick run. ‘Residual’ captures the share of gold returns that isn’t defined by components already included. Outcomes proven listed here are based mostly on evaluation overlaying an estimation interval from June 2019 to August 2024. We now have decreased the estimated window to 5 years to higher mirror present situations. (Sources: Bloomberg, World Gold Council)

Desk 1: Gold’s posted good points in nearly all main currencies in August, regardless of a materially weaker US greenback

Efficiency of gold in numerous currencies*

| USD (oz) | EUR (oz) | JPY (g) | GBP (oz) | CAD (oz) | CHF (oz) | INR (10g) | RMB (g) | TRY (oz) | AUD (oz) | |

| August value | 2,513 | 2,275 | 11,811 | 1,915 | 3,391 | 2,135 | 67,774 | 573 | 85,644 | 3,715 |

| August return | 3.6% | 1.3% | 0.6% | 1.3% | 1.2% | 0.0% | 3.8% | 1.6% | 6.6% | 0.0% |

| Y-t-d return | 20.9% | 20.8% | 25.3% | 17.3% | 23.2% | 22.1% | 21.9% | 20.8% | 39.6% | 21.8% |

|

*Information to 31 August 2024. Based mostly on the LBMA Gold Value PM in USD, expressed in native currencies. Supply: Bloomberg, ICE Benchmark Administration, World Gold Council |

Trying forward

- The present macro setting is hard to learn as a result of swirl of contradictory financial knowledge releases

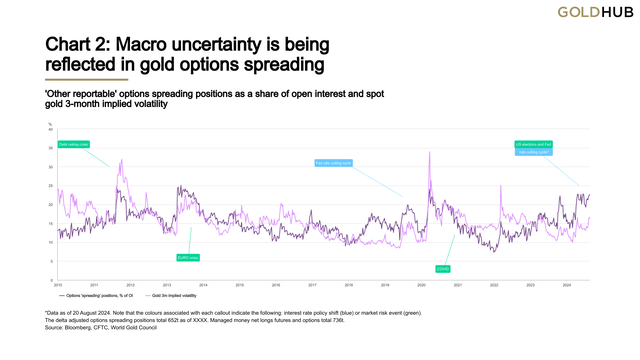

- Arguably the pivotal US election is including to the uncertainty and has doubtless fostered a rise in buyers expressing their view by means of choices markets

- Gold ‘spreading’ positions in choices,1 a usually quieter nook of the gold market, are at a multi-year excessive, suggesting that buyers are both hedging or speculating on each a rate-cutting cycle and the result of the US election.

Globally, high line knowledge nonetheless appears fairly good. GDP development is ticking alongside at 2.5% and composite PMIs stay optimistic. However providers, which account for the lion’s share of output, are supporting these numbers and disguising the truth that manufacturing stays in a little bit of a hunch, significantly in Europe and China.

Zooming in on the US, the scenario additionally seems to be in flux. Composite PMIs are mildly in growth, mirroring the worldwide image. Retail gross sales have been upbeat, the inventory market – following a mini lurch – retains powering forward, and client sentiment perked up just lately.

On the flipside, unemployment jumped to 4.3% in July, a large enough leap to invoke the Sahm Rule,2 whereas mortgage delinquencies are rising quick, and main indicators, in addition to the yield curve, maintain screaming recession.

A gentle touchdown nonetheless appears the almost certainly end result, significantly as Fed Chair Jerome Powell set the stage for a sequence of rate of interest cuts in his annual tackle at Jackson Gap.

Brief-term charge markets, for his or her half, have been little modified after Powell’s remarks, having priced in almost 100 foundation factors in cuts earlier than the top of the 12 months, suggesting they anticipate additional weakening within the labour market. What is evident, as said by Powell, is that the timing and tempo of charge cuts will rely upon incoming knowledge, the evolving outlook and the stability of dangers.

In different phrases, the Fed should navigate between pre-emptively avoiding a recession and the chance of inflation choosing up once more. The latter would arguably be much more damaging.

On this unsure setting, it’s no shock that buyers have taken to the choices market to hedge towards, or speculate on, these seemingly binary outcomes, significantly given the tensions surrounding the US election in November. For example, we proceed to see elevated flows into fairness choices, which have now surpassed the earlier all-time excessive again in This autumn 2023.

This shift in investor behaviour is clear within the gold choices market too. A usually benign and infrequently missed nook of gold knowledge is stirring.

Choices spreading positions (OSP) throughout the CFTC’s Dedication of Merchants report have been steadily rising, nearing ranges not seen since 2019-2020, and earlier than that, 2013 and 2011 (Chart 2). These positions are dominated by the “different reportable” class, which anecdotally is almost certainly to mirror the exercise of Commodity Buying and selling Advisors (CTAs), companies that focus totally on value developments.

Chart 2: Macro uncertainty is being mirrored in gold choices spreading

‘Different reportable’ choices spreading positions as a share of open curiosity and spot gold 3-month implied volatility

*Information as of 20 August 2024. Observe that the colors related to every callout point out the next: rate of interest coverage shift (blue) or market danger occasion (inexperienced). The delta adjusted choices spreading positions whole 652t. Managed cash internet longs futures and choices whole 736t. (Sources: Bloomberg, U.S. Commodity Futures Buying and selling Fee, World Gold Council)

Trying again at these intervals, it appears the triggers for an increase in OSP exercise have been linked to one in every of two situations: both an rate of interest coverage shift (blue) or a market danger occasion (inexperienced).

- The summer time of 2011 was notable for the debt ceiling disaster, which on the time had attracted bets that there could be a first-ever default by the US authorities

- 2019 noticed a spike in OSP as buyers speculated on the beginning of a Fed chopping cycle, which materialised in July of that 12 months. COVID, which appeared a couple of months later, gave rise to a different spike alongside an increase in implied volatility

- An additional and newer spike, in December 2023, got here amidst a dovish ‘language’ pivot by the Fed however didn’t end in charge cuts.

We infer from these historic episodes that market occasion dangers and coverage charge shifts are doubtless drivers of an increase in OSPs.

As we speak, we face each. Markets count on the Fed to embark on a surprisingly aggressive rate-cutting path in September, and we now have a systemically crucial US election in early November.

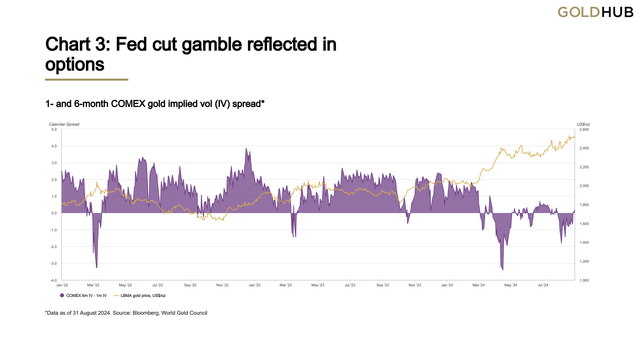

Whereas the OSP knowledge does not reveal the character of the unfold positions, the distinction in implied volatility (IV) at totally different maturities gives clues (Chart 3). This exhibits that short-term IV stays unusually excessive relative to longer-term IV plausibly reflecting the gravity of financial coverage and election developments of late.

Chart 3: Fed reduce gamble mirrored in choices

1- and 6-month COMEX gold implied vol (IV) unfold*

*Information as of 31 August 2024 (Sources: Bloomberg, World Gold Council)

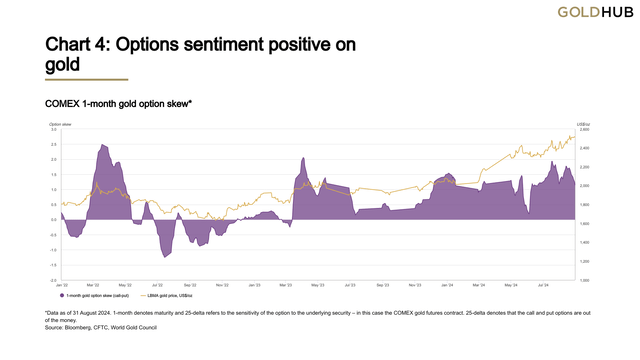

We are able to additionally observe that this preoccupation seems predominantly bullish when taking a look at skew3 – measuring the distinction in demand for calls relative to places (Chart 4). Expectations of value rises seem to dominate hedging wants.

Chart 4: Choices sentiment optimistic on gold

COMEX 1-month gold choice skew*

*Information as of 31 August 2024. 1-month denotes maturity, whereas skew relies on 25-delta which refers back to the sensitivity of the choice to the underlying safety – on this case the COMEX gold futures contract. (Sources: Bloomberg, U.S. Commodity Futures Buying and selling Fee, World Gold Council)

It’s doubtless that the calendar unfold reverts to its regular optimistic stage if and when coverage charge uncertainty wanes – doubtless following the September Fed assembly. Then election outcomes would possibly begin to dominate. However this, in our view, ought to preserve optimistic sentiment as situations for gold stay optimistic no matter which social gathering wins, as we mentioned final month.

In abstract

We are able to solely speculate on how broader macro knowledge would possibly affect market reactions, but it surely appears doubtless that each election dynamics and expectations of charge cuts have elevated exercise in gold, as seen in choices ‘spreading’ positioning. Beneath these circumstances, it’s affordable that buyers are extra targeted on the near-term outlook. Their behaviour means that they view gold as a hedge towards rapid occasion dangers whereas additionally positioning it as a beneficiary of decrease rates of interest.

Outdoors of the US, the persevering with slowdown in China is prone to impression shoppers’ capability and willingness to purchase gold – actually relating to jewelry. However even China’s gold ETFs noticed outflows final month in distinction to the pickup in Indian ETF demand and welcome return of Western ETF inflows.

Footnotes

1A spreading place explanatory be aware might be discovered right here.

2Sahm rule description might be discovered right here

3Skew refers back to the distinction in how choices are priced based mostly on their strike costs. Put merely, it’s the market’s method of exhibiting whether or not individuals are extra fearful in regards to the value going up or taking place. Extra data might be discovered right here.

Authentic Submit

Editor’s Observe: The abstract bullets for this text have been chosen by Searching for Alpha editors.

{kind=link}