greenbutterfly

Funding thesis

GitLab (NASDAQ:GTLB) went public in late 2021 and since then the inventory value has declined greater than 70%. Some folks is perhaps tempted to purchase the dip, however I want to make readers conscious that the upside potential is insignificant in comparison with the extent of dangers and uncertainties. Furthermore, the present harsh surroundings doesn’t favor shares with no earnings, even when they display immense topline progress. I might not purchase GTLB inventory at present ranges, however the firm will probably be on my radar within the subsequent a number of quarters to observe how the scenario unfolds.

Firm info

GitLab is a expertise firm providing the market its full DevOps platform delivered as a single utility. GitLab empowers groups and organizations to streamline their software program growth lifecycle, improve collaboration, and speed up software program supply. Based on the most recent 10-Okay report, the corporate has over 30 million registered customers and over 50% of the Fortune 100 corporations are GitLab clients. GitLab primarily generates revenues from promoting subscriptions on each self-managed and SaaS fashions.

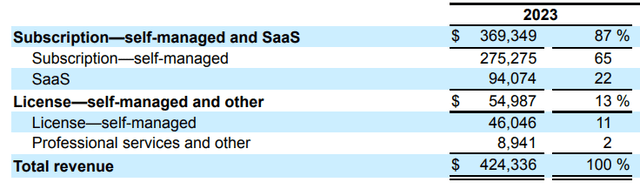

The corporate’s fiscal yr ends on January 31. Self-managed subscriptions comprised virtually two-thirds of the corporate’s whole gross sales in FY 2023.

GitLab’s newest 10-Okay report

Financials

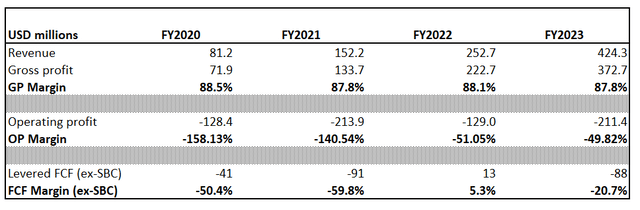

GTLB went public comparatively not too long ago, so the historic monetary efficiency horizon is somewhat quick, with solely 4 full fiscal years out there. The corporate delivered a staggering above 50% income CAGR, although comps have been low and straightforward to beat. The gross margin appears to be like immense, being near 90%. The working margin appears to be like removed from breaking even, nevertheless it improved considerably over the past 4 years.

Writer’s calculations

For me, as a possible investor, the large working loss is a crimson flag, so I want to enter element right here. As you possibly can see within the beneath desk, SG&A bills are large and are increased than income.

Writer’s calculations

I don’t like that R&D bills are a lot decrease than SG&A. Advertising is important for a younger firm like GitLab to create phrase of mouth, however underinvestment in product growth is perhaps pricey in the long run.

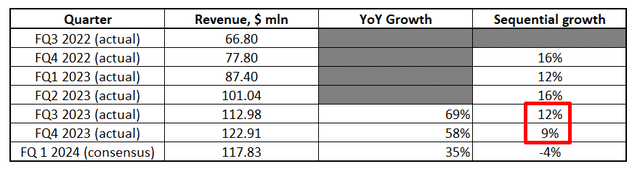

Narrowing right down to the most recent quarterly earnings, the corporate demonstrated a beat in income and EPS in opposition to consensus estimates. The corporate has by no means didn’t beat consensus estimates because it went public, although the pattern is comparatively small to make a assured opinion relating to future quarters.

Searching for Alpha

If we have a look at the income dynamics sequentially, we will see that topline progress is decelerating, and there’s virtually no information to match YoY dynamics. In its newest 10-Okay report, the corporate claims that fiscal quarters 3 and 4 are often stronger than the primary two. Nonetheless, we will see that sequential progress decelerated notably within the final two quarters. YoY progress can also be anticipated to decelerate considerably in Q1 FY2024. The earnings launch is comparatively shut and is deliberate on June 6.

Writer’s calculations

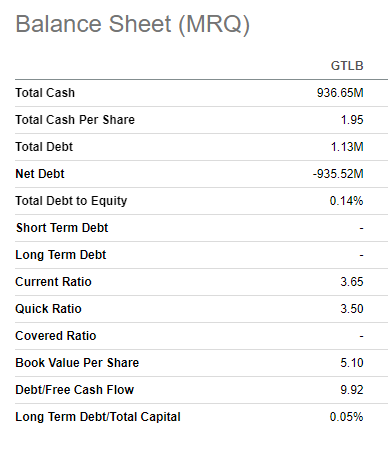

The corporate’s stability sheet appears to be like robust with virtually no debt and excellent money at about $1 billion is considerably increased than the final quarter’s money burn charge of roughly $77 million. Present liquidity is also in fine condition, so I imagine GitLab will not be more likely to face the necessity to elevate further finance within the nearest future, which is an efficient signal given the present tight credit score surroundings.

Searching for Alpha

Valuation

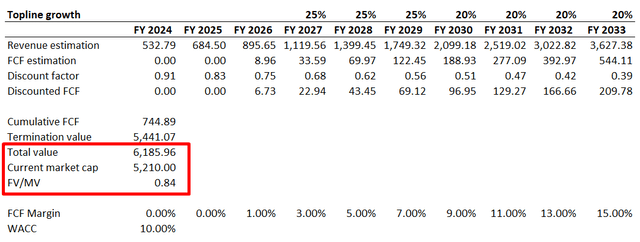

Gitlab is an aggressively rising firm, so I exploit the discounted money stream [DCF] strategy for valuation. I exploit 10% WACC which is a round-up of GuruFocus’ estimate. I’ve income consensus estimates out there for the closest three fiscal years. For years past I undertaking 25% income progress for the subsequent three years after FY2027 after which anticipate it to decelerate to twenty%. I anticipate the corporate to generate constructive FCF in FY 2026 and assume the FCF margin will broaden by two proportion factors yearly.

Writer’s calculations

As we will see, incorporating all assumptions into the DCF mannequin provides us a good worth of the enterprise at about $6.2 billion. It signifies an upside potential between 20% to fifteen%. If GTLB was a worth inventory with sustainable dividends and reliably estimated future money flows, I might have invested instantly given the upside potential. However on account of very excessive uncertainty about underlying assumptions, I think about the upside potential as not engaging.

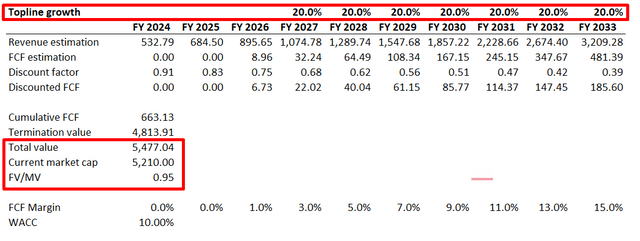

Furthermore, let me additionally simulate much less aggressive however nonetheless very optimistic income CAGR of 20%. Implementing a extra modest income CAGR for years past FY 2027 provides solely a 5% upside potential, which is certainly not adequate for a progress inventory with a excessive uncertainty degree.

Writer’s calculations

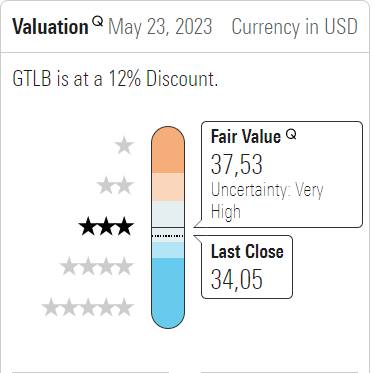

General, I don’t think about the present inventory value engaging. Furthermore, Morningstar Premium estimates GTLB’s share value truthful worth at about $37.5, nearly 10% increased than the precise share value. The uncertainty degree can also be very excessive, in accordance with Morningstar.

Morningstar Premium

Dangers to contemplate

The primary danger that I see within the nearest time period is the general market volatility which an unfavorable macro surroundings could cause. Aside from the AI frenzy fueling the market this yr, there are not any different constructive catalysts for the market. Then again, the conflict in Ukraine continues to be removed from its finish, there’s uncertainty relating to when the Fed will cease its charge hike cycle, and Democrats and Republicans nonetheless can not attain an settlement over the debt ceiling. All these appear vastly unfavorable for the inventory market, and progress shares endure probably the most in general market turmoil. S&P500 is about 10% decrease than all-time highs and I imagine the present harsh macro surroundings will not be priced in.

The corporate’s excessive SG&A prices are additionally an enormous danger. In the course of the newest full-year outcomes, SG&A bills have been nonetheless increased than gross sales. It implies that the corporate has been fueling its aggressive topline progress with aggressive advertising. Thus, there’s excessive uncertainty concerning the capacity to maintain aggressive income progress in case the administration decides to optimize promoting bills. Additionally, I think about the corporate’s SG&A and R&D bills combine, indicating that administration may consider short-term income progress greater than long-term progress. It isn’t good for the long run and dangers the corporate’s capacity to maintain up with technological developments.

Final, GTLB closely depends on open-source options, which might have advantages and dangers. Essentially the most obvious dangers for open-source are safety vulnerabilities, licensing points, and potential conflicts throughout the open-source neighborhood. That is additionally a danger that the administration has to have the ability to handle to mitigate it.

Backside line

General, I imagine the upside potential for GTLB inventory derived from my valuation evaluation will not be price investing in at present ranges. The uncertainty relating to future progress and the break-even timing is imprecise. The corporate continues to be removed from changing into worthwhile, and all progress corporations with no earnings are extremely susceptible to adversarial situations within the macro surroundings. Since 2023 and the few subsequent years are anticipated to be difficult for the worldwide economic system, I additionally don’t see how GTLB inventory will develop below present circumstances. The inventory is a maintain at present ranges, for my part.

{kind=link}