RiverNorthPhotography

Below CEO Ryan Cohen’s management, GameStop Corp. (NYSE:GME) is trying to show across the unprofitable merchandise. Whereas I feel Ryan Cohen has achieved a fantastic job lowering prices and bettering profitability, the gaming {hardware} and software program retail market is prone to face sturdy competitors from each sport publishers and massive retailers akin to Walmart Inc. (WMT) and Amazon.com, Inc. (AMZN). As a retailer, GameStop is unlikely to efficiently flip round their core enterprise sooner or later, for my part. I’m initiating a “Sturdy Promote” ranking with a one-year goal worth of $14 per share.

Difficult Market For Gaming Distribution

GameStop’s enterprise decline was primarily pushed by the difficult retailer market. Extra particularly, the challenges may be summarized as follows:

- On-line Shops Operated by Recreation Publishers: To maximise income, sport publishers have been investing of their on-line channels to encourage clients to buy video games instantly. As an example, Sony operates the PlayStation Community, the place players can buy consoles, video games, and equipment instantly. Equally, Microsoft Company (MSFT) has Xbox Reside and Nintendo owns Nintendo Change On-line. With these on-line shops, there’s little worth proposition for bodily retailers. As well as, Amazon and Walmart have been increasing their distribution community for gaming {hardware} and software program, which has additional challenged the bodily retail enterprise.

- Sooner or later, players will have the ability to obtain particular person digital actuality video games instantly onto their digital actuality {hardware}, akin to headsets or glasses. With the rising reputation of digital actuality, bodily retailers for pc video games will turn out to be more and more irrelevant.

As such, I do not anticipate GameStop can flip round their core enterprise sooner or later, and the corporate is extra prone to enter a virtuous cycle: declining income, retailer closures, and fewer clients.

Management Below Ryan Cohen

Ryan Cohen, the previous activist and CEO of Chewy, Inc. (CHWY), took a 12% place at GameStop and have become CEO in September 2023. I gave him credit for the next:

- Since taking the helm, he has tried to scale back prices and enhance money move and profitability. He acknowledged that many staff and leaders have been making little effort to save lots of the corporate and have been merely ready for retirement. He eliminated a lot of the senior administration workforce on the finish. The SG&A price as a proportion of whole income has been decreased from 28.4% in FY22 to 25.1% in FY23. I feel it’s important for GameStop to cease the monetary bleeding first.

- Ryan Cohen takes no wage, no bonus and different incentives at GameStop, demonstrating his full dedication to turning the corporate round.

GameStop 2023 Proxy GameStop 2023 Proxy

- Ryan Cohen is making an attempt to deal with sport resell enterprise, Omnichannel, in addition to sport equipment. He terminated GameStop’s NFT market in February 2024 and determined to close down the cryptocurrency pockets. I’d be very involved if GameStop grew to become concerned in any cryptocurrency-related enterprise, given the growing regulatory uncertainties. In spite of everything, GameStop is a bodily retailer firm, not a high-tech enterprise.

I feel these initiatives above make strategic sense in trying to show across the enterprise. Nevertheless, the query stays: how can GameStop begin rising their enterprise sooner or later? The income shall be prone to decline over time, and the most effective the administration can do is to scale back prices to enhance margins. Value discount can’t be realized indefinitely, and finally, GameStop will want topline development/stability to generate profitability.

Final December, GameStop’s Board of Administrators authorised a brand new funding coverage, permitting the corporate to put money into fairness securities, amongst different investments. The Board of Administrators designated Ryan Cohen with the authority to handle the funding portfolio. In different phrases, GameStop appears extra prone to flip into an funding firm, with Ryan Cohen because the portfolio supervisor. I feel Ryan Cohen could also be trying to copy his success along with his funding firm, RC Ventures LLC. Nevertheless, I do not assume it is sensible for a retailer to remodel into an funding firm.

Capital and Liquidity

GameStop exited their Q2 FY24 with $4.204 billion in money and money equivalents. GameStop took the benefit of excessive inventory worth to challenge equities:

- On Could seventeenth, 2024, GameStop issued 45 million shares for $933.4 million.

- On June eleventh, 2024, GameStop issued its 75 million shares for $2.137 billion.

As well as, as a consequence of chapter considerations, suppliers have been tightening their credit score requirements with GameStop. Notably, GameStop’s account payable has triggered $398 million money outflow, indicating GameStop has to pay their suppliers in a shorter timeframe.

On the optimistic aspect, the free money move place is probably going to enhance over time as the corporate continues actively controlling their working bills. GameStop generated $68.6 million in working money move in Q2 FY24, a giant enchancment from the $109 million outflow in Q2 FY23.

Moreover, GameStop is closing some unprofitable shops, with 287 retailer closures in FY23. The shop closures may assist the corporate cut back their capital expenditures within the close to future. As such, I do not assume GameStop goes to face any capital liquidity points anytime quickly. Their present money stability of $4.204 billion and free money move must be enough for his or her working capital and capital expenditures over the approaching years.

Current Consequence, Outlook, and Valuation

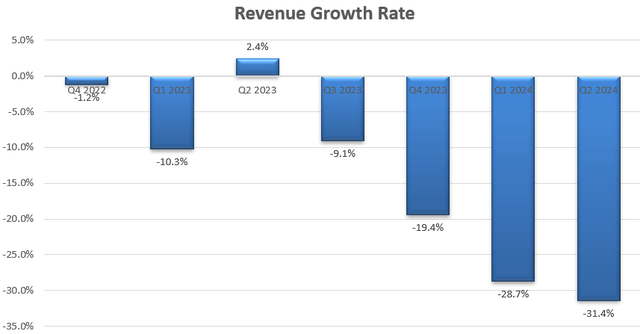

GameStop launched its Q2 consequence on September tenth after the market shut, reporting a 31.4% year-over-year decline in whole income, as depicted within the chart under. The quarterly consequence displays an extra deterioration of GameStop’s core enterprise.

GameStop Quarterly Earnings

I’m contemplating the next components for GameStop’s near-term development:

- I anticipate will proceed closing their unprofitable shops. Mattress Bathtub & Past faces comparable development points, with a structural decline in a difficult bodily retail market. Mattress Bathtub & Past has been closing their shops over the previous few years, now working round 1,000 shops. On the finish of FY23, GameStop operated 4,169 shops in whole. Assuming the corporate will shut 200 shops per yr, it could take round 15 years to scale back to roughly 1,100 shops. I calculate that the shop closure will negatively impression whole income development by 5%-6% within the close to future.

- As mentioned beforehand, Ryan Cohen has been shifting the company technique in direction of used video games, omnichannel and sport equipment. Nevertheless, GameStop is going through vital challenges within the rising competitors from sport builders in addition to huge retailers. As such, I do not assume Ryan Cohen’s technique will help GameStop generate optimistic same-store gross sales development. I assume GameStop’s same-store gross sales will decline by 3% yearly.

- GameStop’s margin enchancment shall be pushed by a number of components. These embrace the closure of unprofitable shops, which is able to enhance the general working margin for bodily areas, and Ryan Cohen’s efforts to regulate SG&A bills by lowering center administration and consolidating some nonfunctional divisions. I calculate GameStop will obtain 50bps annual margin enlargement, assuming 20bps from retailer closures and 30bps from SG&A optimization.

With these parameters, the DCF may be summarized as follows:

GameStop DCF

I calculate the free money move from fairness (FCFE) as follows:

GameStop DCF

The price of fairness is estimated to be 16% assuming: danger free price 3.8%; fairness danger premium 7%; beta 1.88.

Discounting all of the FCFE, the one-year goal worth is calculated to be $14 per share.

Key Upside Dangers

As I assign a “Promote” ranking, I’m contemplating the upside dangers as follows:

- GameStop is a meme inventory with a big base of particular person buyers. These buyers could accumulate a sure measurement of Purchase orders to set off a brief squeeze for brief sellers. It has already occurred prior to now, and it’s potential to occur once more sooner or later.

- Ryan Cohen has been fairly profitable along with his funding agency, RC Ventures LLC. Because the Board of Administrators has already licensed him the ability to put money into a broad vary of investments, he may have the ability to make some worthwhile investments, whether or not in public fairness or non-public fairness. In that case, GameStop may turn out to be worthwhile via these investments.

- Lastly, Ryan Cohen may flip GameStop into a non-public firm by buying shares at a premium from current shareholders. In that state of affairs, the inventory worth may transfer greater sooner or later.

Finish Notes

I feel GameStop’s core retail enterprise will proceed to face structural challenges from sport builders and massive retailers. It appears extra doubtless that Ryan Cohen will steer GameStop towards changing into an funding firm, as a turnaround of their core enterprise seems not possible. I’m initiating a “Sturdy Promote” ranking for GameStop Corp. inventory with a one-year goal worth of $14 per share.

{kind=link}