pidjoe

Funding Thesis

I needed to check out First Photo voltaic (NASDAQ:FSLR) and the way it has improved its financials since FY22. It looks as if the corporate has improved rather a lot and is projected to make first rate margins and income development going ahead, nonetheless, even with such an enchancment, I imagine the corporate is barely overvalued and assign a maintain ranking till we see some extra numbers sooner or later to substantiate the constructive trajectory.

Outlook

Solar energy has been experiencing a growth within the final decade, going from complete vitality era of round 95TWh in 2012, to over 1,200TWh by 2022. We will see that it’s gaining in recognition as increasingly international locations turn into extra environmentally aware. Renewable vitality has turn into a giant matter lately with ESG elements taking part in a a lot greater function. Millennials and Gen Z are going to be the primary generations that will likely be investing their financial savings for retirement within the subsequent decade or so, and these generations are extra environmentally aware than any earlier era. So, this naturally is a constructive for First Photo voltaic. There’ll at all times be individuals who will need to put money into the betterment of the earth by renewable vitality like photo voltaic.

Many international locations are additionally offering authorities subsidies within the type of tax breaks/credit for corporations like First Photo voltaic, and it relies upon rather a lot on these subsidies to generate revenues. In my view, these subsidies all all over the world won’t go away anytime quickly and can most definitely speed up due to the present generations which can be extra environmentally aware. The demand for renewable vitality is there and governments usually are not going to squander that. Only recently, the Biden-Harris administration introduced a $7B “Photo voltaic for All Grant competitors” that goals to fund prices for households and “advance environmental justice by investing in America”.

India, which nonetheless will get most of its vitality, round 80%, from coal, oil, and different non-renewable vitality will likely be a fantastic future alternative for First Photo voltaic, because the Indian authorities is beginning to heat to the concept of renewable vitality and it desires to have photo voltaic vitality to be the chief within the nation with round 60% of vitality to return from photo voltaic, which will likely be round 280GWh by 2030. India doesn’t symbolize a really huge marketplace for FSLR but, nonetheless, with many of the nation getting round 300 days of clear and sunny days, coupled with authorities incentives, I might see this changing into a a lot greater income generator sooner or later, particularly now that the development of the manufacturing facility is accomplished there and can start manufacturing shortly.

It additionally looks as if the expansion of photo voltaic vitality goes to proceed on a powerful constructive trajectory, as it’s predicted to develop at a really respectable 25.9% CAGR till ’28. This already coincides with what FSLR can attain when it comes to income era, with the newest 10-Q report exhibiting revenues elevated by round 30% from the identical quarter final yr.

Financials

All of the graphs under will likely be as of FY22; nonetheless, I’ll embody a number of the newest figures for additional shade whether it is mandatory.

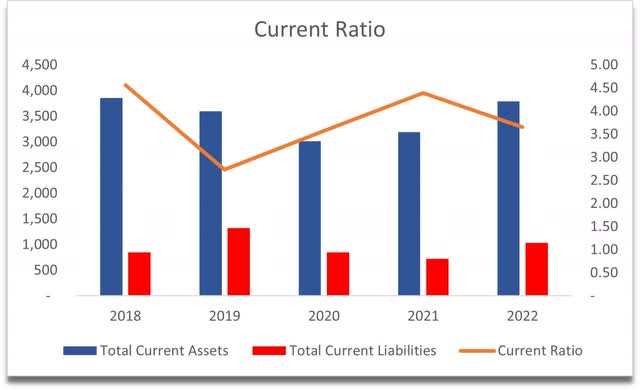

As of Q2 ’23, the corporate had round $1.9B in money and marketable securities, towards $437m in long-term debt. This can be a very robust place to be in, which offers flexibility in how the corporate goes to broaden its world footprint and different initiatives. The corporate’s present ratio has been just a little too excessive in my view, which is an effective and a foul factor. A superb factor as a result of it has no issues paying off its short-term obligations and a foul factor as a result of this tells me that the corporate is not being very environment friendly in utilizing its belongings for additional enlargement. I wish to see the corporate being extra aggressive in future enlargement. As of Q2 ’23, the ratio stood at over 3.3. My splendid vary is anyplace between 1.5-2.0. That is the vary I imagine tells us that the corporate is being environment friendly with its accessible liquidity and nonetheless in a position to repay its short-term obligation with ease.

Present Ratio (Writer)

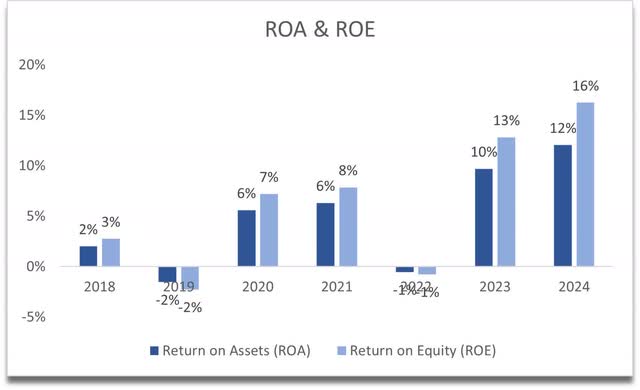

The corporate’s historic ROA and ROE haven’t been very spectacular to say the least, nonetheless, for the reason that firm has turn into fairly a bit extra worthwhile if we have a look at the analyst’s estimates, the graphs under will embody years ’23 and ’24 which present how these metrics would possibly evolve and so they look a lot more healthy than earlier than.

ROA and ROE (Writer)

If the numbers in ’23 and ’24 are near the place the corporate would possibly find yourself, then it’s a superb return on each metrics.

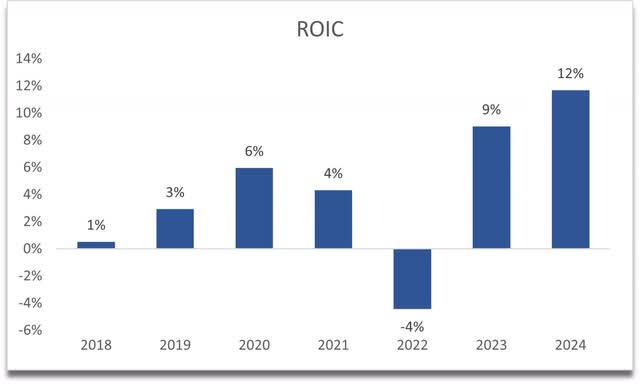

The identical may be stated in regards to the firm’s return on invested capital. The historic numbers have been fairly disappointing, nonetheless, for the reason that firm appears to be having a turnaround, ROIC would possibly develop like this sooner or later:

ROIC (Writer)

This could inform me that the corporate has a good moat and a aggressive benefit.

Total, if we simply have a look at the historic figures, it’s going to present fairly a combined bag of outcomes, and definitely not the perfect, but when we make some assumptions, the profitability and effectivity will enhance fairly significantly within the upcoming years. Take the estimates with a grain of salt as a result of these are simply my estimates, and rather a lot can occur over the subsequent couple of years. Costs could fluctuate, and manufacturing prices improve as soon as once more, which is able to convey down these metrics as they did up to now.

Valuation

It looks as if the previous income development would not apply to FSRL as a result of, up to now decade, the corporate managed to lose 21% of revenues. FY15 to FY16 and FY17 to FY18 drops may be defined by divestitures. Now, with the current efficiency within the newest quarter, analysts are estimating round 33% development in FY23 and round 30% in FY24. As an example the time has come for FSLR to shine, so for my base case, I went with an 18.8% CAGR over the subsequent decade, 22.5% for my optimistic case, and 16.8% CAGR for an optimistic case.

I admit these figures are extra than simply optimistic, however analysts see numerous enchancment over the subsequent decade when it comes to revenues and margins, so I’ll persist with these estimates.

Talking of margins, FY22 was a really unhealthy yr for FSLR. Price of gross sales accounted for 97.3% of internet gross sales. The largest price got here in from freight, demurrage, and detention fees, which accounted for $167m. Within the newest quarter, gross margins got here in at round 38%, which tells us that the prices have stabilized, and the corporate goes to carry out significantly better sooner or later.

I made a decision to enhance gross margins from round 35% in FY23 to round 45% by FY32, which I imagine is barely optimistic additionally.

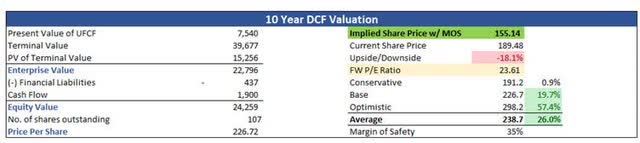

As a result of I made a decision to go along with such optimistic assumptions and since the monetary estimates additionally look nice on assumptions, I’ll add a 35% margin of security to the intrinsic worth calculation. With that stated, First Photo voltaic’s intrinsic worth is $155.14 a share, implying that at the moment the corporate is barely overvalued.

Intrinsic Worth (Writer)

Closing Feedback

The corporate has numerous potential to carry out very properly, with many international locations subsidizing the way forward for vitality consumption, FSLR goes to be one of many leaders to seize numerous development on this section, nonetheless, does this imply that the corporate goes to be a lot extra worthwhile going ahead than it was up to now? Is the income development that I assumed for the mannequin attainable? It’s laborious to inform given the previous income development, or lack thereof.

Nonetheless, if the share worth retreats barely to my implied share worth, the chance/reward could be rather more engaging than now, and I’d severely look into opening a place and see the way it goes within the subsequent couple of years.

Presently, the corporate is buying and selling at 15.6x ’24 earnings in line with my mannequin, and at my PT it might be buying and selling at round 12x, which I would like to be sincere, so I will likely be ready patiently for a pullback if one occurs. If not, then I am going to hold on the lookout for an organization that’s nearer to my danger/reward profile.

{kind=link}