Printed on December fifteenth, 2022 by Aristofanis Papadatos

Exxon Mobil (XOM) launched its 5-year progress plan final week. This plan is undoubtedly promising, as the corporate expects to develop its manufacturing considerably, cut back its common manufacturing value and double its earnings per share vs. 2019. As well as, the oil large is prospering proper now, as it’s on monitor to publish file earnings per share this yr due to an exceptionally favorable enterprise surroundings. However, traders ought to concentrate on some caveats. On this article, we’ll analyze the promising points of its formidable progress plan of Exxon, however we can even talk about some factors of concern.

We created an inventory of all 66 Dividend Aristocrats. You may obtain the complete spreadsheet of all 66 Dividend Aristocrats, together with a number of vital monetary metrics resembling dividend yields and price-to-earnings ratios, by clicking on the hyperlink under:

Enterprise Overview

Exxon Mobil is the second-largest oil firm on the earth, with a market capitalization of $437 billion, behind solely Saudi Aramco (ARMCO). In 2021, Exxon generated 62% of its whole earnings from its upstream phase, whereas its downstream and chemical segments generated 8% and 30% of its whole earnings, respectively.

Just like the overwhelming majority of oil producers, Exxon incurred materials losses in 2020 as a result of unprecedented lockdowns applied in response to the pandemic. Nevertheless, world oil consumption has now recovered to pre-pandemic ranges.

Even higher for oil producers, the sanctions imposed by the U.S. and Europe on Russia for its invasion of Ukraine have significantly tightened the worldwide vitality market. Earlier than the invasion, Russia produced roughly 10% of world oil output and one-third of the pure fuel consumed in Europe. Thus, it’s simple to know the affect of Western international locations’ sanctions on the worldwide vitality market.

Attributable to these sanctions, oil and fuel costs rallied to 13-year highs earlier this yr and remained above common. That is an exceptionally favorable enterprise panorama for all oil majors, together with Exxon.

Within the second quarter, the oil large posted almost all-time excessive earnings per share of $4.14 due to the rally of oil and fuel costs. Within the third quarter, the worth of oil dipped 12% sequentially, however the value of pure fuel skyrocketed due to a file variety of LNG cargos exported from the U.S. to Europe. These exports helped Europe compensate for the diminished fuel portions acquired from Russia, however they rendered the U.S. fuel market extraordinarily tight. Due to the extraordinarily excessive fuel costs and the almost all-time excessive refining margins, which resulted from the diminished exports of oil merchandise by Russia, Exxon grew its earnings per share 7% sequentially, from $4.14 to an all-time excessive of $4.45, and exceeded the analysts’ estimates by a powerful $0.65. The oil large is on monitor to publish file earnings per share of a minimum of $13.00 this yr.

The Progress Plan

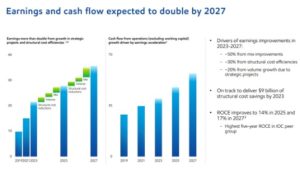

Final week, Exxon analyzed its progress plan for the subsequent 5 years. The corporate expects to spend $20-$25 billion per yr on capital bills and double its earnings by 2027 vs. 2019.

Supply: Investor Presentation

Exxon expects to realize such a terrific efficiency primarily due to a steep discount in its common value of manufacturing, which can consequence from the addition of low-cost barrels to its asset portfolio. The opposite progress contributors can be a discount in structural prices and significant manufacturing progress.

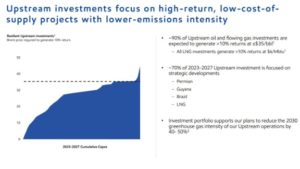

Based on its progress plan, Exxon will allocate about 70% of its investments in areas with low-cost barrels, particularly the Permian Basin, Guyana, and Brazil.

Supply: Investor Presentation

It’s spectacular that about 90% of investments of Exxon can be directed to reserves which can be anticipated to yield an annual return of greater than 10%, even at oil costs of round $35. Which means the oil large will high-grade its asset portfolio drastically within the upcoming years.

Due to its good progress plan, Exxon expects to develop its manufacturing by 3% per yr on common till 2027 and double its earnings potential at a given oil value of $60.

Supply: Investor Presentation

On this manner, the oil main will offset the impact of the exit of its operations from Russia and another divestments. As well as, greater than half of its output will come from reserves with a bonus of $9 per barrel vs. its present asset portfolio.

The strategic plan of Exxon is undoubtedly promising. The corporate expects to develop its manufacturing considerably whereas it can drastically lowering its common value of manufacturing, primarily due to the addition of exceptionally low-cost barrels within the Permian and offshore Guyana. The latter is at the moment essentially the most thrilling progress undertaking in all the oil trade. Over the last 5 years, Exxon has greater than tripled its estimated reserves within the space, from 3.2 billion barrels to about 11.0 billion barrels. Total, due to its funding plan, Exxon expects to scale back its breakeven value of oil from $40 in 2022 to about $30 in 2027.

The expansion plan of the oil main additionally features a share repurchase program of as much as $35 billion in 2023-2024. This quantity is ample on the present inventory value to scale back the share rely by 8%. Nevertheless, it is very important understand that the inventory of Exxon has rallied 74% over the past 12 months to an all-time excessive stage. Given the excessive cyclicality of the oil trade, the share repurchases executed round all-time excessive inventory costs are more likely to harm shareholder worth as an alternative of enhancing it.

Exxon has made the identical mistake up to now. It spent extreme quantities on share repurchases throughout growth years, and thus it got here underneath nice strain in 2020 when the coronavirus disaster struck. Whereas the corporate didn’t face liquidity dangers, it leveraged its stability sheet considerably in that yr, thus main many analysts to foretell a dividend reduce. Luckily, Exxon didn’t reduce its dividend due to the sturdy restoration of the vitality market from the pandemic, however the lesson stays the identical. It’s not prudent to spend extreme quantities on share repurchases close to the height of the cycle of this extremely cyclical trade.

Furthermore, oil exploration and manufacturing have so many parameters that traders shouldn’t take the steerage of Exxon without any consideration. In fact, the strategic plan of Exxon is as exact as it may be proper now, however many components might considerably derail the plan.

To supply a perspective, Exxon issued an analogous 7-year progress plan in early 2018. Based on that progress plan, the oil large anticipated to develop its manufacturing by 25%, from 4.0 million barrels per day in 2018 to five.0 million barrels per day in 2025, primarily due to its hefty investments within the up-and-coming areas of the Permian Basin and Guyana.

Nevertheless, the precise efficiency of Exxon deviated remarkably from the plan. The corporate determined to curtail its investments as a result of pandemic in 2020-2021 to protect funds and thus defend its beneficiant dividend. As well as, the pure decline of its present oil fields, which is inevitable, took its toll on the manufacturing of the oil main. Consequently, the manufacturing of Exxon has decreased by roughly 7% since 2018, a a lot worse final result than the anticipated improve of 25%. As a facet be aware, the pure decline of oil fields, which is sort of at all times materials, is usually underestimated within the progress plans of oil producers.

Additionally it is value noting that Exxon is the one oil main that has didn’t develop its manufacturing over the past 14 years. Throughout this era, the corporate incurred a 7% lower in its manufacturing. That is in sharp distinction to the efficiency of the opposite oil majors, resembling Chevron (CVX), BP (BP), and TotalEnergies (TTE), which have constantly grown their manufacturing over the past 5 years.

Total, the aforementioned 5-year plan of Exxon is actually promising, but it surely stays to be seen whether or not the oil large will obtain the targets of its plan. The uncertainty needs to be attributed to not the efficiency of administration however principally to the components past administration’s management, i.e., the cycles of the oil trade and the pure decline of oil fields.

Lastly, it is very important be aware that the worth of oil has peaked and has in all probability entered it’s subsequent downcycle. Whereas it’s nonetheless above its historic common, it has lately fallen under its stage simply earlier than the invasion of Russia in Ukraine. It is a sturdy bearish sign, which suggests that the vitality market has totally absorbed the affect of the battle in Ukraine, principally due to the worldwide financial slowdown and a file variety of renewable vitality tasks which can be underneath growth proper now. When all these tasks come on-line, they’re more likely to take their toll on the worth of oil.

Aggressive Benefits

The first aggressive benefit of Exxon is its unparalleled scale and admirable experience within the vitality sector. Exxon has written the usual technical procedures adopted by most oil corporations. Additionally it is spectacular that different oil corporations drilled quite a few dry holes in Guyana, whereas Exxon has exhibited a virtually 90% success price on this space.

Furthermore, due to its extremely built-in enterprise mannequin, Exxon is among the most resilient oil majors to recessions and downturns within the vitality market. Exxon’s downstream and chemical divisions have offered a buffer to the entire earnings at any time when oil costs have plunged. This doesn’t imply that Exxon is proof against recessions. It solely implies that Exxon is extra resilient to downturns than most of its friends. As an example, when the worth of oil collapsed from $100 in mid-2014 to $30 in early 2016, Exxon noticed its earnings per share plunge 75%, but it surely remained worthwhile, whereas Chevron and BP incurred losses.

Dividend

As a result of dramatic swings within the value of oil, the oil trade is notorious for its excessive cyclicality. Its boom-and-bust cycles make it virtually unattainable for the sector corporations to take care of multi-year dividend progress streaks. Exxon has proved distinctive on this side. It’s the solely oil firm, together with Chevron, that has turn out to be a Dividend Aristocrat. Exxon has grown its dividend for 40 consecutive years, and thus it could boast of the longest dividend progress streak within the oil trade.

Furthermore, the corporate at the moment has a payout ratio of solely 28%. Moreover, due to its file earnings this yr, it has drastically diminished its debt and has a rock-solid stability sheet. Consequently, Exxon can simply proceed elevating its dividend for a lot of extra years.

The one caveat is the almost 8-year low present dividend yield of three.4% of the inventory, which has resulted from the steep rally of the inventory to an all-time excessive. The low dividend yield of Exxon (in comparison with its historic yields) alerts that the inventory might be considerably richly valued from a long-term viewpoint. Exxon’s dividend progress price has markedly slowed in recent times, from a median annual price of 5.0% within the final decade to a median annual price of three.0% within the final 5 years. Revenue-oriented traders ought to in all probability watch for a extra engaging entry level earlier than buying Exxon.

Remaining Ideas

The lately introduced 5-year progress plan of Exxon is undoubtedly promising. The oil large intends to fireplace on all cylinders. It expects to develop its manufacturing, cut back its common value of manufacturing with the addition of low-cost barrels, and spend extreme quantities on share repurchases. Exxon expects to roughly double its earnings potential at a given oil value in 5 years due to all these progress drivers.

The oil large will definitely do its finest to perform this purpose, however traders ought to concentrate on some caveats. To begin with, the dramatic cycles of the oil trade, that are inevitable, are past the corporate’s management. As well as, the corporate has repeatedly dissatisfied its shareholders with its enterprise execution, because it has didn’t develop its manufacturing over the past 14 years. Furthermore, oil value peaked shortly after Russia’s invasion of Ukraine and has in all probability entered their subsequent downcycle. Subsequently, whereas the strategic plan of Exxon is actually promising, traders shouldn’t be shocked if the outcomes are totally different from the steerage.

In case you are concerned with discovering extra high-quality dividend progress shares appropriate for long-term funding, the next Certain Dividend databases can be helpful:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}