Daniel Grizelj/DigitalVision through Getty Photographs

Introduction

Again in 2022, Enviva (NYSE:EVA) discovered themselves within the crosshairs of short-sellers who raised a number of points and while administration was fast to defend themselves, they have been but to fully show the short-sellers improper, as my earlier article defined. Quick ahead to the current day and sadly for shareholders, their newest outcomes and accompanying fairness issuance have been successfully alike to a present for the short-sellers as they despatched their share worth plunging over 10% in a single session and thus right down to recent 52-week lows.

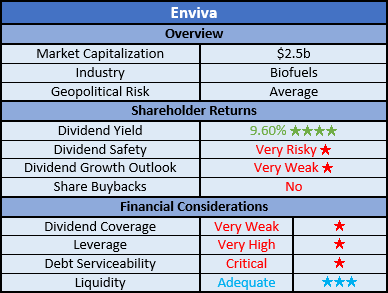

Protection Abstract & Scores

Since many readers are probably brief on time, the desk under offers a quick abstract and scores for the first standards assessed. If , this Google Doc offers data relating to my score system and importantly, hyperlinks to my library of equal analyses that share a comparable strategy to reinforce cross-investment comparability.

Creator

Detailed Evaluation

Creator

Following the short-seller report by Blue Orca Capital again throughout 2022, their full-year outcomes have been extremely anticipated with shareholders hoping to lastly show the bears improper. While there have been many considerations raised by Blue Orca, I however noticed their money technology to be essentially the most urgent, as my earlier article mentioned.

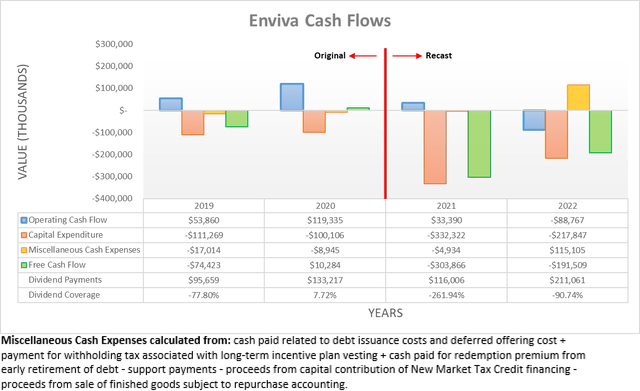

Sadly on this entrance, their working money stream not solely failed to enhance in the course of the fourth quarter of 2022 however quite, it really worsened with the full-year now seeing a results of damaging $88.8m versus their earlier results of damaging $51.6m in the course of the first 9 months. Sure that’s right, they actually endured a money burn to function the corporate, not to mention make investments or make shareholder returns, each of which proved to be hefty payments themselves. Within the case of the previous, their capital expenditure ended the yr at $217.8m and within the case of the latter, their dividend funds required one other $211.1m of money.

Fairly apparently, the fourth quarter of 2022 additionally noticed a brand new line merchandise hitting their money stream assertion for the primary time ever, as they acquired $102.3m pertaining to “proceeds from sale of completed items topic to repurchase accounting”, as their 2022 10-Okay. When establishing my graph above, this was included inside miscellaneous money bills, thereby offsetting their different routine and comparatively insignificant objects, that are famous beneath. While some traders could really feel this gives a decision to their money burn, it ought to be famous these items are topic to repurchase, as the road merchandise aptly states. When having a look at their stability sheet, they now see a $111.9m present legal responsibility pertaining to “monetary legal responsibility pursuant to repurchase accounting” and thus, regardless of boosting their money inflows throughout 2022, it might reverse throughout 2023.

Creator

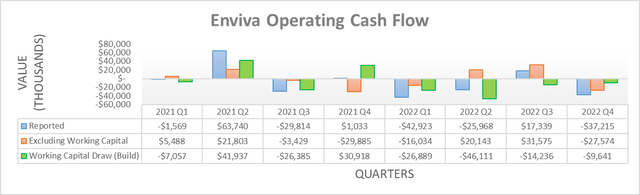

When wanting into their quarterly working money stream, it’s regarding to see no tangible indicators of enhancements, nor a optimistic general route. As for the reported working money stream, the fourth quarter of 2022 noticed a damaging results of $37.2m, therefore their full-year end result going backwards versus the primary 9 months.

Much more worryingly, their underlying outcomes that exclude working capital actions don’t see any enhancements. When conducting the earlier evaluation, it was no less than optimistic to see these bettering sequentially earlier in 2022 with their respective outcomes of $20.1m and $31.6m in the course of the second and third quarters displaying quarter-on-quarter enhancements. Though, this ended with the fourth quarter and its results of damaging $27.6m and thus their money burn can’t merely be blamed on the timing of funds. If their working capital actions are excluded throughout the full-year, it sees an insignificant underlying results of $8m and thus, nowhere close to sufficient to cowl their dividend funds. Curiously, they anticipate this in any other case dire scenario to out of the blue change throughout 2023, as per the commentary from administration included under.

“For 2023, once you have a look at our money stream from operations, what we anticipate is that our regular course of enterprise fulfilling our contracted backlog in 2023 will generate working money stream that won’t solely cowl our dividend that we have guided to, however in truth, exceed that dividend.”

-Enviva This fall 2022 Convention Name.

While shareholders are clearly hoping for such a dramatic and really optimistic change, it however is tough to see how their working money stream might see such a dramatic change. Resulting from their fairness issuances all through 2022, reaching this objective would require extra working money stream than the $211.1m their dividend funds value throughout 2022. Even when ignoring their subsequently mentioned fairness issuance that’s but to be fully finalized, their newest excellent share rely is 67,610,102, which implies their quarterly dividends of $0.905 per share will value no less than a staggering $244.7m throughout 2023. In actuality, the associated fee to fund their dividend funds throughout 2023 goes to blow out nearer to circa $270m given their subsequently mentioned fairness issuance. Regardless of their very robust earnings steering, it’s tough to see this objective being achieved given they didn’t generate any materials working money stream throughout 2022 nor even 2021, ever since restructuring with their former dad or mum firm and thus altering from a Grasp Restricted Partnership into an organization.

Enviva Fourth Quarter Of 2022 Outcomes Announcement

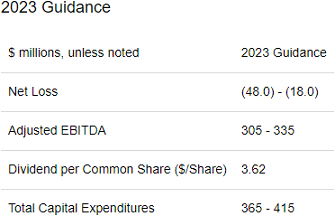

When taking a look at their steering for 2023, they’re forecasting adjusted EBITDA of $320m on the midpoint, which is roughly double their results of $155.2m throughout 2022, as per their fourth quarter of 2022 outcomes announcement. Whether or not this results in a sudden change of their money technology stays to be seen however prefer it or not, they’re nonetheless but to fully show the short-sellers improper on this entrance.

Creator

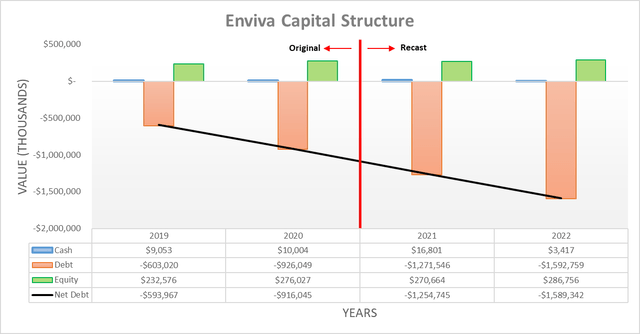

Because of the aforementioned $102.3m money influx from the sale of completed items which might be topic to repurchase agreements, their money burn in the course of the fourth quarter of 2022 solely had a small impression on their internet debt. That mentioned, it nonetheless was inadequate to cease any will increase with it climbing to $1.589b versus its earlier degree of $1.526b following the third quarter.

Even when they handle to show their working money stream round and canopy their dividend funds throughout 2023, their capital expenditure steering for $390m means they are going to stay dependent upon exterior capital. On this entrance, they’ve additionally lately introduced a $250m fairness issuance that can assist plug a few of this hole however comes at a hefty value given it represents about 10% of their present market capitalization of roughly $2.5b. The very last thing their firm wants is pushing the invoice to fund their already burdensome dividend funds one other circa 10% greater, which solely makes their aforementioned working money stream objective much more tough to realize. Elsewhere, financial coverage is anticipated to stay tight all through all the yr and presumably into 2024 and thus the price of debt will stay elevated, as evidenced by their bonds buying and selling with a excessive near-9% yield.

Finra Markets Through Morningstar

Just like when conducting the earlier evaluation, their damaging working money stream throughout 2022 makes it pointless to evaluate their leverage intimately, because it renders such ratios ineffective with logically invalid damaging outcomes. As an alternative, their gearing ratio can function a backup measure and given their internet debt of $1.589b and fairness of solely $286.8m, it presently stands at 84.72%. Unsurprisingly, this as soon as once more represents one other enhance versus its earlier results of 80.00% following the third quarter and due to this fact, pushing it additional previous the brink of fifty.01% for the very excessive territory. This similar logic additionally applies elsewhere to their debt serviceability as a result of their damaging money stream efficiency clearly leaves it vital with curiosity expense requiring a continued combination of debt and fairness issuances.

Creator

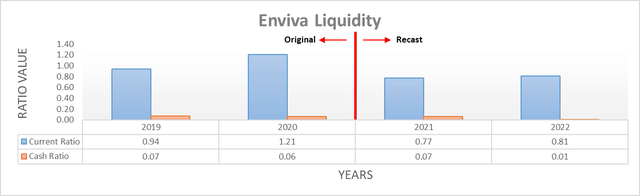

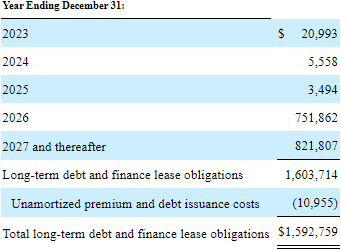

Following the fourth quarter of 2022, their liquidity stays enough regardless of their present and money ratios seeing their respective outcomes lower to 0.81 and 0.01 versus their earlier respective outcomes of 1.09 and 0.04 following the third quarter. Extra importantly, their credit score facility didn’t see its availability endure and actually, it really elevated barely to $133m versus its earlier quantity of solely $97.9m following the third quarter, largely as a result of issuance of an extra $98m of tax-exempt inexperienced bonds, which have been mentioned when conducting the earlier evaluation. It will likely be necessary to watch this throughout 2023 however no less than one shiny spot is their debt maturity profile, which solely sees minor maturities till 2026 and thus offers a level of respiration room.

Enviva 2022 10-Okay

Conclusion

Until they flip a metaphorical swap throughout 2023 and activate their money technology, it’s tough to see how an organization with no historical past of producing materials working money stream can presumably flip a deep damaging end result into a powerful optimistic end result inside one yr. If this objective is achieved, it might be extraordinarily spectacular however even when forthcoming, their leverage remains to be very excessive and thus proceed to hinder the attraction of their shares. To make issues even worse, their upcoming fairness issuance is successfully a present to the short-sellers by pushing down their share worth through dilution while concurrently making their dividend funds much more burdensome. Since I really feel their dividends are very dangerous and more likely to be reduce, I imagine that sustaining my promote score is suitable and look ahead to publishing a follow-up evaluation later within the yr as soon as subsequent outcomes land.

Notes: Until specified in any other case, all figures on this article have been taken from Enviva’s SEC filings, all calculated figures have been carried out by the writer.

{kind=link}