Justin Paget

Entergy Company (NYSE:ETR) is a regulated electrical utility that serves the states of Texas, Arkansas, Louisiana, and Mississippi:

Entergy Company

That is an space of the nation that has been rising at a reasonably speedy tempo, notably Texas. In truth, Texas is among the ten most quickly rising states within the nation for a wide range of causes. Entergy is thus well-positioned to benefit from this case and profit from a rising buyer base in that state. Nonetheless, this isn’t the one factor that this firm has going for it, as Entergy Company is among the most aggressive utilities in relation to the deployment of renewable vitality era and the promotion of other fuels. This may not be what can be anticipated from a utility that operates within the Deep South, notably within the state of Texas, contemplating that Texas is the point of interest of the American hydrocarbon trade. Nonetheless, the geography of Texas makes it very properly suited to the usage of each wind and solar energy and the state has been making the most of that.

As I discussed in my final article on Entergy, the corporate enjoys a outstanding quantity of economic stability and resilience to financial shocks. That is one thing that would show very advantageous proper now contemplating the big quantity of economic pressure that many customers are below as quickly rising costs have precipitated actual wages to say no and depleted the financial savings that had been constructed up throughout the COVID-19 pandemic. Entergy is prone to be resistant to any opposed impacts that this case may need on client spending, which might make it an affordable funding proper now. The truth that the corporate presently trades at a really enticing valuation solely enhances this thesis. Thus, allow us to examine and see if this firm might make sense in your portfolio at this time.

About Entergy Company And Progress Potential

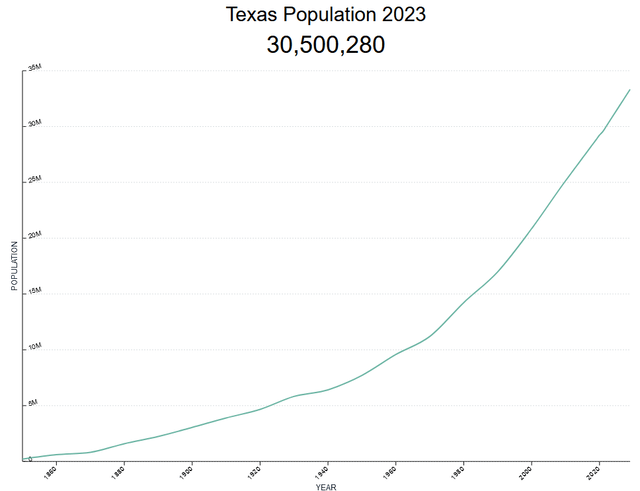

As talked about within the introduction, Entergy is a regulated electrical utility that serves the Deep South states of Texas, Louisiana, Arkansas, and Mississippi. That is an space that has been seeing important inhabitants development over the previous few years, with Texas main the pack. In accordance with the U.S. Census Bureau, the inhabitants of Texas is rising at a 1.57% fee, which ranks it as one of many 5 fastest-growing states within the nation. As of proper now, the state’s inhabitants is estimated at roughly 30.5 million and it’s projected to hit 33.3 million folks by the top of the last decade:

World Inhabitants Evaluation

Arkansas can be rising, positing a present inhabitants development fee of 0.57% year-over-year. Sadly, this robust development is partially offset by Louisiana and Mississippi, that are experiencing inhabitants declines of 0.80% and 0.32% respectively. I defined why this inhabitants development is a constructive factor in my final article on this firm:

The explanation that that is necessary for Entergy is that inhabitants development is among the solely ways in which a utility can develop, and it’s fully out of the utility’s management. It is because Entergy is a monopoly that’s restricted to working in a selected area by regulation and it can’t develop by convincing clients exterior of its service territory to modify suppliers. The very fact, then, that Texas is among the quickest rising states when it comes to inhabitants offers a tailwind to the corporate’s development. The identical is true of Arkansas, nevertheless, each Louisiana and Mississippi have been experiencing inhabitants declines since 2020. Total, although, the development is constructive and Entergy’s buyer base is rising.

Thus, over time Entergy ought to have extra folks in its service space and thus extra folks paying their month-to-month utility payments. This could trigger the corporate’s revenues to extend, all else being equal. That may give the corporate more cash to make use of to cowl its mounted bills and in the end make its approach right down to revenue and money circulate. Thus, the service space demographics are one issue within the firm’s favor.

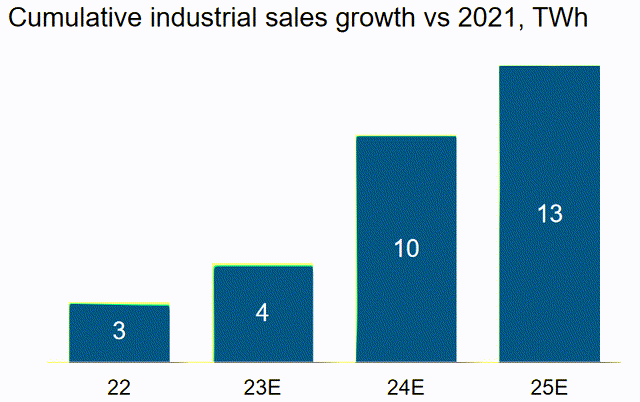

One of many the reason why Texas has been experiencing such robust inhabitants development is due to industrial enlargement within the space. We’re seeing factories being constructed in Texas at a reasonably speedy tempo, for instance. Tesla (TSLA) is a reasonably good instance of this, as the corporate constructed one among its “gigafactories” in Austin, Texas, and even moved its headquarters to the state. This firm was hardly alone on this both, as there are a number of liquefied pure gasoline crops being constructed alongside the Gulf Coast together with supporting infrastructure to maintain this new development. These are only a few examples of the financial development in Texas that’s attracting folks to the state and rising its inhabitants. Entergy stands to learn from this too as a result of factories and different trade require a big quantity of electrical energy. Entergy notes that it presently sells roughly 4 terawatt hours of electrical energy to factories and different industrial services in its service territory. That is anticipated to extend to a whopping 13 terawatt hours by 2025:

Entergy Company

It is a 225% enhance in two years. It must be pretty simple to see how that may have a useful influence on the corporate’s revenues and money circulate. This doesn’t, in fact, embrace the truth that any staff of those industries who’ve to maneuver into the corporate’s service territory will start utilizing electrical energy of their properties. As well as, these industries are usually going to be offering jobs that pay enough wages to permit for some discretionary spending. Thus, we might see eating places, retail shops, and different companies pop as much as present leisure and varied client discretionary gadgets to those folks. All of those companies may even eat electrical energy and pay common payments to Entergy. Total, it is a excellent state of affairs for the corporate to be in.

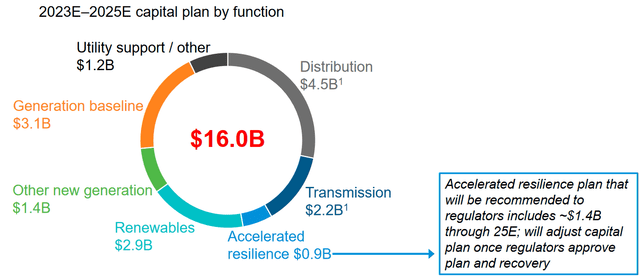

Naturally, although, the corporate might want to develop its infrastructure so as to accommodate this rising demand for electrical energy. In spite of everything, electrical wires, energy substations, era services, and different infrastructure that the corporate may need solely have a restricted capability that it will possibly deal with or ship. The corporate might want to put money into new infrastructure so as to enhance its capability. Thankfully, Entergy is planning on doing precisely that. The corporate lately unveiled a plan to take a position roughly $16.0 billion into this space of its enterprise over the 2023 to 2025 interval:

Entergy Company

This cash is not going to be spent with out acceptable payback for the corporate. In spite of everything, this capital spending will enhance the corporate’s fee base. I outlined the speed base in my earlier article on this firm:

The speed base is the worth of the corporate’s belongings upon which regulators permit the corporate to earn a specified fee of return. As this fee of return is a proportion, any enhance within the fee base permits Entergy to regulate the costs that it fees its clients so as to earn more cash.

This funding program is predicted to extend the corporate’s fee base from $35 billion at this time to roughly $42 billion on the finish of 2025. This works out to a 6.26% compound annual development fee over the three-year interval. That doesn’t essentially imply that the corporate’s earnings per share will develop on the identical fee, though it is going to in all probability be fairly shut. There could also be a discrepancy between the 2 figures although as a result of Entergy Company might want to finance its development program. Ceaselessly, utilities will partially fund capital funding by way of the issuance of recent widespread inventory. This dilutes the prevailing shareholders and leads to earnings per share development being considerably lower than the corporate’s fee base development. Thus, within the absence of steerage from the corporate, we are able to in all probability assume that its earnings per share development will probably be about 5% to 7% over the interval. When mixed with the present 4.47% yield, we get a complete projected return of 10% to 12% yearly, which could be very cheap for a conservative utility inventory. This must be acceptable to most buyers.

Income And Money Circulation Stability

Within the introduction to this text, I discussed that Entergy enjoys remarkably steady revenues and money flows whatever the situation within the broader economic system. We are able to see this fairly clearly by wanting on the firm’s revenues over the previous a number of years. Listed here are the corporate’s figures for every of the previous ten full-year intervals, in addition to the twelve-month interval that ended on June 30, 2023:

Searching for Alpha

As we are able to instantly see, there may be little or no variation from 12 months to 12 months, although the circumstances within the economic system skilled some steep swings over just a few of those intervals. Particularly, the full-year 2020 interval would come with the COVID-19 lockdowns, which additionally included the shutdown of quite a few companies for a number of months. Once we think about the variety of companies that weren’t working throughout that interval, together with many factories and different giant employers, we might count on to see a reasonably important decline in revenues. Nonetheless, what we truly do see was very small in comparison with the prior-year interval. In truth, it’s fairly onerous to consider that many workplaces, factories, retail shops, eating places, and quite a few different giant customers of electrical energy lowered their consumption in any respect.

We see a really related state of affairs once we take a look at the corporate’s working money flows over the identical interval. Right here they’re:

Searching for Alpha

As was the case with income, we see little or no fluctuation within the figures over time, though they’re extra risky than revenues. That’s to be anticipated although since occasions such because the timing of when the corporate paid sure payments, rate of interest adjustments, and varied different one-off occasions can impact money flows. The purpose although is that the corporate’s monetary efficiency must be largely unaffected by the monetary well being of the American client or the American economic system. That time is mainly made by these figures.

I defined the explanations for this in my final article on Entergy Company:

The explanation for this normal money circulate stability is the character of Entergy’s enterprise. The corporate offers a product that’s usually thought-about to be a necessity for contemporary life. In spite of everything, how many individuals do not need electrical service of their properties? Certainly, electrical service is just about vital for absolutely anything else that somebody may need of their properties for leisure or work. As such, most individuals will prioritize paying their electrical invoice forward of creating discretionary bills throughout occasions when cash will get tight. In spite of everything, no one will wish to exit for a meal or two in a restaurant with their final $100 and danger having their electrical energy turned off.

There are indicators that the common American client has been getting weaker over the previous few months. For instance, LendingClub states that roughly 64% of People are presently dwelling paycheck-to-paycheck. Vice President Kamala Harris lately said that “most People are a single $400 expense away from chapter,” in a speech in Iowa again in July. This actually doesn’t sound like an atmosphere that will probably be conducive to a excessive stage of discretionary spending. In truth, the announcement earlier at this time that the inflation fee elevated once more will undoubtedly put much more stress on the common particular person’s means to spend cash. An organization like Entergy ought to be capable of navigate such an atmosphere a lot better than an organization that relies upon closely on discretionary client spending for income. That’s precisely the type of firm that we wish to personal in an atmosphere like this.

Debt And Monetary Construction

As I identified previously, you will need to look at an organization’s monetary construction as a part of our funding analysis:

It’s all the time necessary that we examine the best way that an organization is financing its operations earlier than we make an funding in it. It is because debt is a riskier approach to finance an organization than fairness as a result of debt have to be repaid at maturity. That’s sometimes achieved by issuing new debt and utilizing the proceeds to repay the prevailing debt since only a few firms have enough money readily available to fully repay their debt because it matures. As new debt is issued with an rate of interest that corresponds to the market fee on the time of issuance, this could trigger an organization’s curiosity bills to go up following the rollover.

As of the time of writing, the efficient federal funds fee is at 5.33%, which is significantly increased than it was the final time that we mentioned Entergy Company. In truth, the federal funds fee is now on the identical stage that it was in early 2001 previous to the recession that adopted the popping of the know-how bubble. We actually have to return to the early days of the George W. Bush Administration to discover a time during which rates of interest had been similar to at this time’s ranges. As such, it’s a pretty secure assumption that any debt rollover at this time will trigger an organization’s curiosity bills to extend. I pointed this out in a latest article on one among Entergy’s friends.

As of June 30, 2023, Entergy Company had a internet debt of $26.0848 billion in comparison with $13.5870 billion of shareholders’ fairness. This offers the corporate a internet debt-to-equity ratio of 1.92 at this time. That is solely barely increased than the 1.91 ratio that the corporate had on the finish of the primary quarter, so it seems to be making an attempt to maintain it considerably steady. Right here is how the corporate’s ratio compares to that of its friends:

|

Firm |

Internet Debt-to-Fairness Ratio |

|

Entergy Company |

1.92 |

|

DTE Power (DTE) |

1.89 |

|

Eversource Power (ES) |

1.58 |

|

CMS Power (CMS) |

1.91 |

|

Exelon Company (EXC) |

1.68 |

One factor that we discover right here is that every one of those firms noticed their internet debt-to-equity ratios enhance since we final mentioned Entergy Company. These are, in any case, the identical friends that we used for our comparability beforehand. Entergy noticed the smallest quarter-over-quarter enhance, with its ratio rising by a scant 0.01, whereas all of its friends elevated by way more than that. This might point out a specific amount of economic self-discipline on Entergy’s half, which is unquestionably good to see in at this time’s rate of interest atmosphere. Sadly, Entergy nonetheless continues to rely extra on debt to finance its operations than its friends. As such, its debt load might symbolize increased dangers to shareholders than friends. That is one thing that we wish to proceed to look at, as we wish to see Entergy cut back its internet debt-to-equity ratio over time.

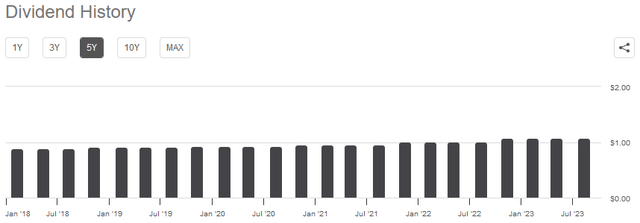

Dividend Evaluation

One of many largest the reason why we buy shares of utilities like Entergy Company is that they normally have the next yield than most different issues available in the market. Entergy is actually no exception to this, as its 4.47% dividend yield is considerably increased than the 1.46% yield of the S&P 500 Index (SPY). The corporate’s dividend yield can be increased than the two.66% yield of the U.S. Utility Index (IDU). Entergy additionally has an extended historical past of accelerating its dividend on an annual foundation:

Searching for Alpha

As I’ve identified earlier than, a rising dividend is good throughout inflationary intervals as a result of it helps preserve the buying energy of the dividend within the face of inflation. As well as, a rising dividend will lead to a inventory’s yield-on-cost being very excessive after just a few years. That’s one thing that would enchantment to anybody who plans to carry a inventory for an prolonged time period.

As is all the time the case although, it will be significant that we make sure that an organization can truly afford the dividends that it pays out. In spite of everything, we don’t wish to be the victims of a dividend lower, since that would scale back our incomes and nearly actually trigger the corporate’s share worth to say no.

The same old approach that we decide an organization’s means to pay its dividends is by its free money circulate. Over the twelve-month interval that ended on June 30, 2023, Entergy reported a unfavourable levered free money circulate of $1.3539 billion. That’s clearly not sufficient to pay any dividends, but Entergy nonetheless paid out $883.7 million to its shareholders over the interval. At first look, that is prone to be regarding as the corporate is unable to cowl all of its monetary obligations and bills solely out of its inside money era functionality.

Nonetheless, it’s fairly widespread for a utility to cowl its capital expenditures by way of the issuance of debt and fairness. I discussed this earlier on this article. The corporate will then pay its dividends out of working money circulate. That is because of the very excessive bills concerned in establishing and sustaining utility-grade infrastructure over a large geographic space. In the course of the twelve-month interval that ended on June 30, 2023, Entergy reported an working money circulate of $3.5955 billion, which was simply sufficient to cowl the $883.7 million that it paid out in dividends over the identical interval and go away the corporate with a considerable sum of money left over. Total, the corporate shouldn’t have any issue sustaining its dividends on the present stage and can in all probability enhance the dividend fee when it publicizes its third quarter 2023 earnings outcomes, identical to it normally does.

Valuation

In accordance with Zacks Funding Analysis, Entergy Company will develop its earnings per share at a 5.65% fee over the subsequent three to 5 years. That is fairly according to what the corporate ought to be capable of accomplish primarily based on its fee base development, so it looks as if a superb estimate. At this development fee, Entergy has a price-to-earnings development ratio of two.53 on the present inventory worth.

Right here is how that compares to the corporate’s friends:

|

Firm |

PEG Ratio |

|

Entergy Company |

2.53 |

|

DTE Power |

2.80 |

|

Eversource Power |

2.51 |

|

CMS Power |

2.31 |

|

Exelon Company |

2.73 |

That is fascinating as just a few of those firms have change into significantly cheaper previously few months since we final mentioned this firm. Entergy, DTE Power, Eversource Power, and CMS Power are all cheaper than they had been again in July. Nonetheless, Exelon Company is way more costly than it was earlier than. For essentially the most half, Entergy Company continues to look pretty valued relative to its friends, however the cheaper valuation may enhance its enchantment considerably within the eyes of extra value-oriented buyers.

Conclusion

In conclusion, Entergy Company has lots to supply an investor proper now. Texas is presently experiencing extra financial development than many different elements of the USA, and Entergy is making the most of this. The consumption of electrical energy by the corporate’s customers continues to develop and the corporate’s revenues are rising consequently. It’s investing a substantial sum of money to assemble the infrastructure wanted to service all of this new demand, which ought to permit the corporate to ship a ten% to 12% whole common annual return over the subsequent few years. That’s barely above what the corporate’s friends are prone to ship over the identical interval. Sadly, the corporate’s leverage stays considerably above the trade common, and this might be a dangerous state of affairs within the present excessive rate of interest atmosphere. The corporate is just not an particularly huge discount at its present worth both, though it’s not notably costly. It might be price selecting up although, particularly if you’re prepared to greenback price common into the shares.

{kind=link}