sefa ozel

Vitality Earnings Efficiency

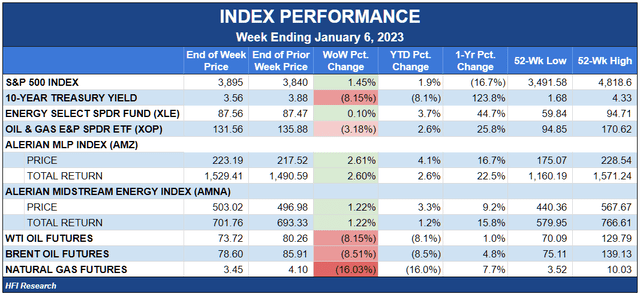

Vitality shares purchased for revenue rose this week, as WTI dropped 8.2% because of a weakening bodily oil market and pure fuel plunged 16.0% in response to forecasts for heat climate in North America and Europe. Regardless of these headwinds, the Alerian Midstream Vitality Index gained 1.2%, and the Alerian MLP Index rose 2.6%. Not surprisingly, E&Ps couldn’t keep away from the commodity value carnage, sending the SPDR S&P Oil & Gasoline Exploration & Manufacturing ETF (XOP) down 3.2%.

HFI Analysis

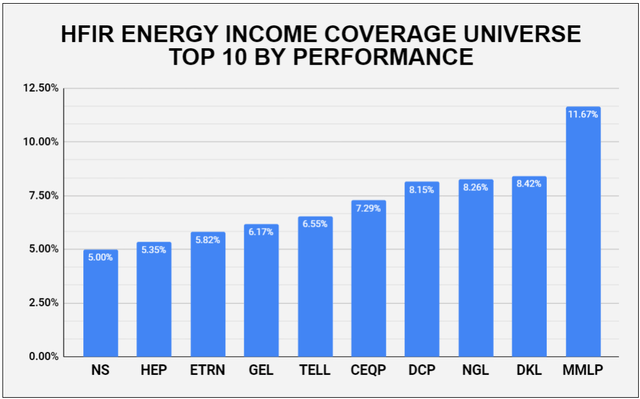

The week’s value motion was uncommon. The very best performers in our protection universe have been weaker-capitalized operators and many who have publicity to commodity costs. Among the many former, we suspect that a part of the snapback was attributable to the heavy promoting that occurred over the previous few weeks, as worldwide traders disposed of their MLPs to keep away from punitive tax withholding guidelines that went into impact on January 1.

HFI Analysis

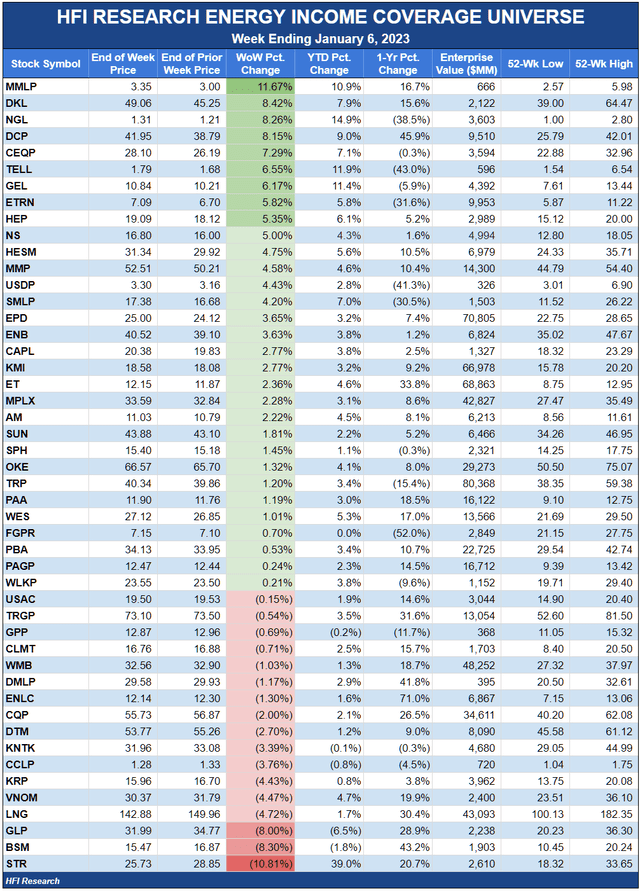

The very best instance of the MLP snapback phenomenon this week was Martin Midstream Companions (MMLP), which was the sector’s finest performer, up 11.7% on no information. The corporate might have additionally gotten a lift from an bettering bond market, which may support its efforts to execute a refinancing.

One other overleveraged title that outperformed was NGL Vitality Companions, LP (NGL). The items gained 8.3% after administration elevated its fiscal 2023 Adjusted EBITDA steerage by 5% and reported that the corporate paid down $227 million of debt, bringing its debt stability all the way down to $3.26 billion. Whereas these developments illustrate NGL’s progress on deleveraging, we estimate they scale back NGL’s leverage ratio from 5.8-times to five.5-times, which is hardly low sufficient for NGL’s fairness to be thought-about secure. NGL must proceed to outperform and pay down debt for not less than one other two years to carry its leverage ratio under 4.5-times, which we take into account the higher certain of an inexpensive leverage ratio.

It was additionally notable that NGL appointed a brand new CFO after the earlier one had been within the place for little greater than a yr.

Given the uncertainty of NGL’s skill to maintain its outperformance and administration’s horrible capital allocation report, we reiterate our Promote score on NGL and advocate that traders keep away from the items.

DCP Midstream (DCP) surged 8.2% after it obtained a sweetened buyout supply from Phillips 66 (PSX). PSX will purchase DCP shares for $41.75, above our expectation that PSX would purchase the shares at $40. The deal is truthful in that it offers DCP unitholders with a sexy exit whereas it additionally leaves meat on the bone for PSX, because the decrease finish of our price vary for DCP is $43. We don’t consider one other supply will likely be forthcoming. With DCP items buying and selling above the sweetened value, unitholders ought to use the chance to promote.

Tellurian (TELL) shares had a dead-cat bounce that despatched them 6.6% greater throughout the week on no information. The bounce got here after the shares had misplaced half their market capitalization since November. We fee TELL as a Promote and advocate that traders keep away from the shares. Nevertheless, there could also be a chance right here for essentially the most speculative traders. If TELL can survive for the subsequent few months, which is probably going, and if Europe’s structural pure fuel scarcity turns into a problem subsequent winter, which seems possible, the shares may soar several-fold from present costs.

Genesis Vitality (GEL), which we flagged for a possible bounce-back after its items bought hammered starting in November, additionally positioned among the many high 10 gainers, rising 6.2%.

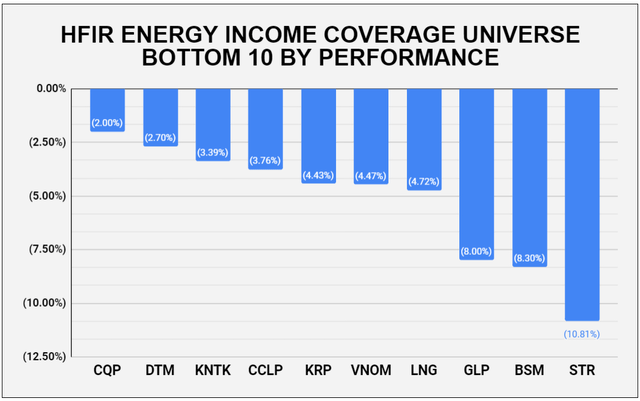

As for the losers throughout the week, royalty trusts dominated the checklist, which is comprehensible given their dependence on commodity costs. Sitio Royalties was the biggest decliner, falling 10.8% throughout the first week of buying and selling because it closed on its acquisition of Brigham Minerals.

HFI Analysis

Black Stone Minerals (BSM) and Viper Vitality Companions (VNOM) have been different royalty trusts that traded decrease on no company-specific information.

The opposite poor performers have been pure gas-weighted operators equivalent to Kinetik Holdings (KNTK) and Cheniere Vitality (LNG), which can also be to be anticipated in per week that noticed pure fuel costs plunge in North America and Europe.

Weekly HFI Analysis Vitality Earnings Portfolio Recap

Our portfolio underperformed its benchmark, the Alerian MLP Index, by 1.5%, giving again a few of its 3.5% outperformance from the earlier week. Our giant holdings of BSM and Cheniere drove the underperformance.

Regardless of the poor efficiency relative to its benchmark, we’re happy with our holdings’ exhibiting. Our giant MLPs outperformed throughout the commodity selloff, and our G&Ps held up surprisingly properly. We consider the week’s largest losers, Cheniere and BSM, are undervalued at present costs and fee every a Purchase. For BSM, we’d level out that commodity costs have inflected to some extent that makes its hedges considerably extra worthwhile.

The largest information amongst our holdings was Targa Assets’ (TRGP) announcement that it could buy the 25% curiosity within the Grand Prix NGL Pipeline it didn’t already personal from Blackstone Vitality Companions for $1.05 billion. TRGP administration estimates the acquisition represents a sexy 8.75-times Grand Prix’s 2023 Adjusted EBITDA

The Grand Prix NGL pipeline transports 1 million barrels per day of NGLs from the Permian Basin to Mont Belvieu, the place TRGP has been rising its fractionation and export capabilities. The acquisition provides stability to TRGP’s money flows whereas fortifying its vertical integration via the NGL provide chain.

We just like the deal and commend TRGP’s administration on a few of the finest capital allocation expertise within the midstream sector.

Information of the Week

Jan. 4. Colonial Pipeline Co. halted flows to the Northeastern U.S. after a 60-barrel leak of diesel on its Line 3 in Virginia. The diesel flowed right into a stormwater assortment basin, which minimized its environmental influence. The pipeline was again up and operating on Friday, January 6. The outage had little influence on refined product provides at New York Harbor, given its common imports from different provide sources, together with Canada, Europe, India, and South America.

Jan. 4. Antero Midstream (AM) disclosed in an SEC submitting that it was awarded $242 million in damages after it prevailed in court docket on its claims of breach of contract and fraud in opposition to Veolia Water Applied sciences (OTCPK:VEOEY). The court docket additionally present in Antero’s favor on all of Veolia’s affirmative claims. AM is prone to put the money to good use in accelerating its deleveraging.

Capital Markets Exercise

Jan 3. Targa Assets introduced the pricing of $900 million of 6.125% senior notes due 2033 and $850 million of its 6.500% senior notes due 2053 at 99.858% and 97.843% of face worth, respectively. The observe providing is being made to fund TRGP’s acquisition of the 25% of its Grand Prix NGL Pipeline that it didn’t already personal.

Jan. 4. Enterprise Merchandise Companions, LP (EPD) introduced the pricing of $750 million of senior notes due 2026, which can have a fixed-rate curiosity coupon of 5.05%, and $1.0 billion of senior notes due 2033, which can pay a fixed-rate curiosity coupon of 5.35%. The corporate intends to make use of the proceeds to fund development capital investments and to repay debt.

HFI Analysis

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}