Editor’s observe: In search of Alpha is proud to welcome Jerome Davis as a brand new contributor. It is easy to turn into a In search of Alpha contributor and earn cash in your greatest funding concepts. Energetic contributors additionally get free entry to SA Premium. Click on right here to search out out extra »

HT Ganzo

Thesis

Ecora Assets (OTCQX:ECRAF) primarily has lengthy life royalties on copper, nickel and cobalt mines, metals that are important to the inexperienced transition. It has low debt and working prices, and at a $1.75 worth per share, Ecora has a market cap of round $450 million, which is lower than 5 instances medium time period (3-5 years) annual revenues of round $100 million. Usually, royalty firms are inclined to commerce at 10 instances their annual revenues at a minimal, particularly when specializing in lengthy life inexperienced metals property. Subsequently, I believe the inventory ought to commerce at a least $3.50 per share and charge it as a powerful purchase.

Firm Overview

Ecora is non-precious metals royalty firm, which traditionally has primarily been often known as a coal royalty firm. It is two predominant legacy property had been the Kestrel coking coal royalty and the Narrabri thermal coal royalty, each of that are positioned in Australia. But in just a few years’ time, Ecora can have nearly no coal royalty publicity, because it has offered its Narrabri royalty, and the Kestrel operator can have mined out the areas topic to Ecora’s royalty by 2026. As an alternative, Ecora will primarily be a base metals royalty firm with a big publicity to copper, nickel and cobalt.

This transformation within the commodity combine within the Ecora royalty portfolio took place because of a strategic choice by administration to give attention to future-facing metals. They even lately modified their identify from Anglo Pacific Mining to replicate their new inexperienced profile. I believe the choice to rework the commodity composition of the corporate is an effective one, as there’s going to be substantial demand for copper, nickel and cobalt within the inexperienced transition. Moreover, only a few royalty firms are at the moment energetic on this space, which ought to worth this firm’s inventory at a premium, as soon as the market realizes its transformation from coal to inexperienced metals.

It achieved this commodities transformation by utilizing the revenues generated from its coal royalties to finish two main base metals acquisitions:

- In February 2021, it acquired a stream on 22.82% of all cobalt manufacturing from Voisey’s Bay, a world class base metals mine in Canada operated by Vale.

- In July 2022, it acquired a portfolio of royalties over superior growth stage copper and nickel tasks from South32. Notable royalties embody a 2.0% internet smelter return (“NSR”) royalty on the West Musgrave nickel and copper venture in Australia owned by OZ Minerals (which BHP is within the technique of buying), and a 2.0% NSR royalty on the Santo Domingo copper and cobalt venture in Chile owned by Capstone Copper.

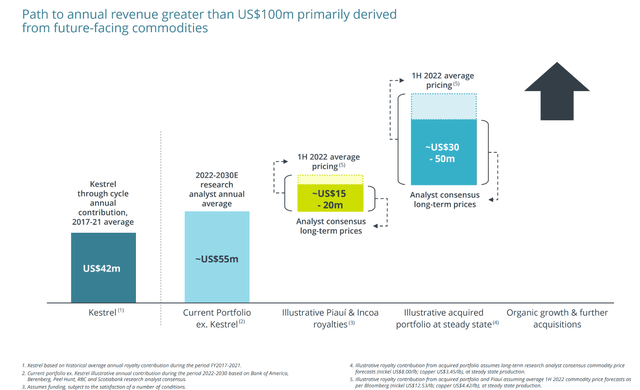

These giant transactions be certain that Ecora is scheduled to generate about $100 million in annual revenues (see chart under) within the medium time period, which exceeds its historic revenues from its largest legacy coal royalty (Kestrel). Notably, as a consequence of terribly excessive revenues from its Kestrel royalty lately, it was capable of obtain this utilizing little or no debt. On the finish of 2022 Ecora had a internet debt of $35 million. Moreover, it retains ~$180 million of liquidity for future progress.

Supply: Ecora Assets February 2023 Investor Presentation

Firm Financials

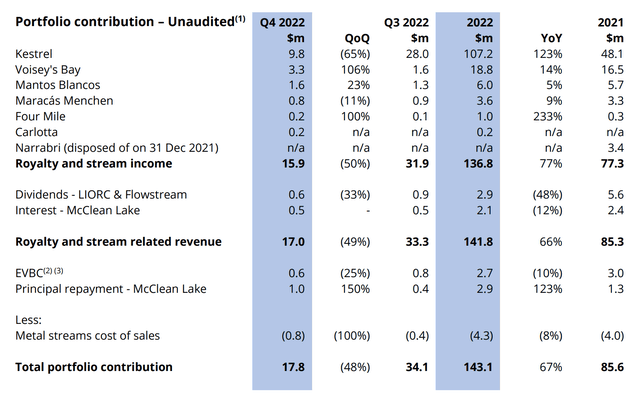

Ecora studies their financials on semiannual foundation, which implies that their most up-to-date monetary report covers the primary half of 2022. Nonetheless, within the interim, they do present buying and selling updates, the newest of which was revealed in January 2023 (see chart under). Ecora has 10 producing royalties, an important of that are the Voisey’s Bay cobalt stream in Canada and the Mantos Blancos copper royalty in Chile together with the legacy Kestrel royalty.

The Kestrel royalty accounted for $107 million of the $143 million in royalty revenues generated in 2022, making it by far an important royalty for that yr. This was as a consequence of a confluence of things together with excessive coking coal costs, giant manufacturing volumes from Ecora’s royalty areas, and will increase within the Queensland royalty charges, that are used to set Ecora’s royalty charges. It’s unclear whether or not excessive coking coal costs will proceed in 2023, and Ecora expects volumes delivered from its royalty areas to lower by 50% from 2022 ranges. Nonetheless, it is going to nonetheless possible contribute a major quantity of royalty revenues in 2023. Revenues from the Kestrel royalty are anticipated to wind down by 2026.

Voisey’s Bay and Mantos Blancos are long-lived mines with wonderful potential for extensions past the present mine life (2035 for Voisey’s Bay and 2038 for Mantos Blancos). Voisey’s Bay accounted for $14.5 million in internet revenues to Ecora in 2022 ($18.8 million in gross sales income minus $4.3 million in manufacturing funds), and Mantos Blancos accounted for $6.0 million in revenues. At the moment, each mines are ramping up: Voisey’s Bay is anticipated to supply 2,600 tons of cobalt by 2025 in comparison with round 1,700 tons produced in 2022; and Mantos Blancos anticipated to supply 52,000 tons of copper yearly over the following 10 years in comparison with round 40,000-45,000 tons of copper at the moment.

Supply: Ecora Assets This autumn 2022 Buying and selling Replace

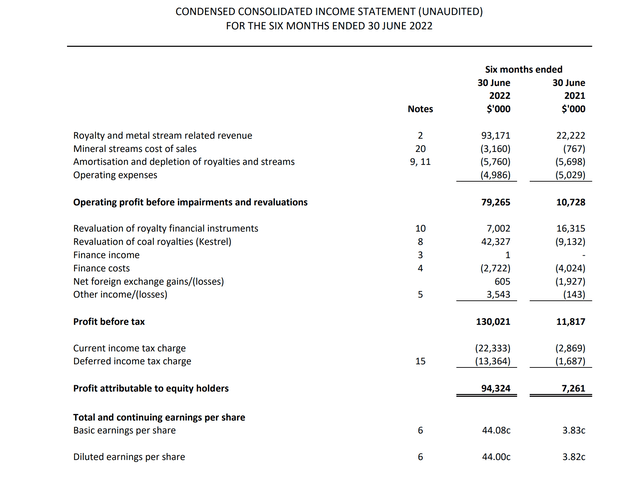

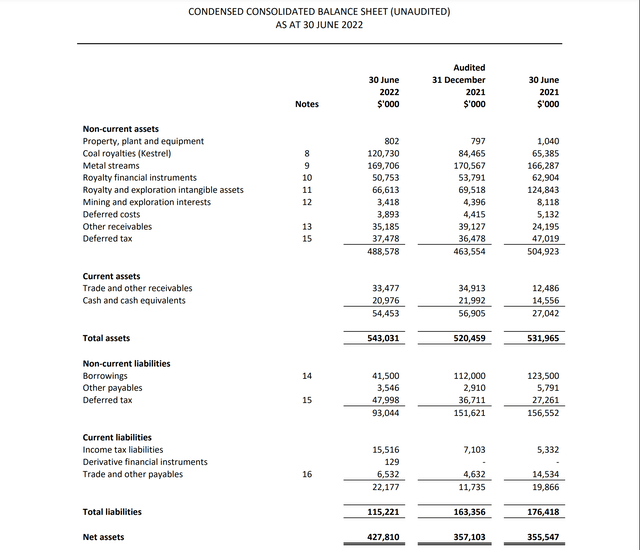

The newest revenue and steadiness sheet statements present perception into how the royalty revenues movement all the way down to the underside line (pages 15 and 17 of 2022 Half Yr Outcomes). Usually, expenditures are comparatively small in comparison with revenues. I estimate that price of gross sales, amortization and depletion, and working bills account for round $28 million in expenditures yearly. Many of the different loss and revenue gadgets (besides finance prices) are one-offs that are inclined to common to zero within the medium to long run, as for instance, royalty valuations might improve or lower yr to yr, however must be pretty secure over time.

Finance prices rely on the quantity of debt and the rate of interest charged on that debt. Finance prices decreased between June thirtieth, 2021 and June thirtieth, 2022 as borrowings decreased from $123.5 million to $41.5 million. The mortgage services that Ecora has entry to cost LIBOR plus 2.75% to 4.50% relying on leverage ratios. Present LIBOR charges are round 5%. Assuming conservatively that Ecora’s long-term borrowings are $100 million and that it pays 10% on these borrowings yearly, I estimate that Ecora’s medium-term annual finance prices may very well be round $10 million.

When subtracting expenditure and finance prices from $100 million in anticipated revenues, this flows all the way down to Ecora earnings earlier than taxes of round $62 million. The proportion tax, Ecora pays appears to range over time, however seems to be near round 20%. Subsequently, I estimate potential internet after tax earnings of round $50 million. Subsequently, about half of revenues are anticipated to movement down as internet revenue, and this proportion ought to improve as revenues improve, which may occur by new royalty purchases or increased commodity costs.

The share construction of Ecora is tight with comparatively few excellent choices and warrants, which could be seen be evaluating fundamental earnings per share with diluted earnings per share. There was some general share dilution, however this was undertaken to accumulate base steel royalties on Voisey’s Bay, West Musgrave and Santo Domingo, and will subsequently be thought-about to be accretive. One potential concern is the excessive dividend per share that Ecora gives. The present dividend is 1.75 pence per share per quarter, which works out to round $0.085 per share yearly (or round 5% at a $1.75 share worth). Multiplying the dividend per share by Ecora’s present share rely of round 257 million shares, provides annual dividend bills of $22 million. This must be nicely coated by the anticipated future internet revenue of $50 million. The dividend yield is round 5%, when in comparison with an Ecora market cap of $450 million utilizing a worth per share of $1.75.

Supply: Ecora 2022 Half Yr Outcomes Supply: Ecora 2022 Half Yr Outcomes

Firm Valuation

Utilizing the data mentioned within the part above we are able to calculate medium time period valuation ratios for Ecora:

- Value/Gross sales: 4.5 ($450 million market capitalization / $100 million in revenues)

- P/E: 9.0 ($450 million market capitalization / $50 million in internet revenue)

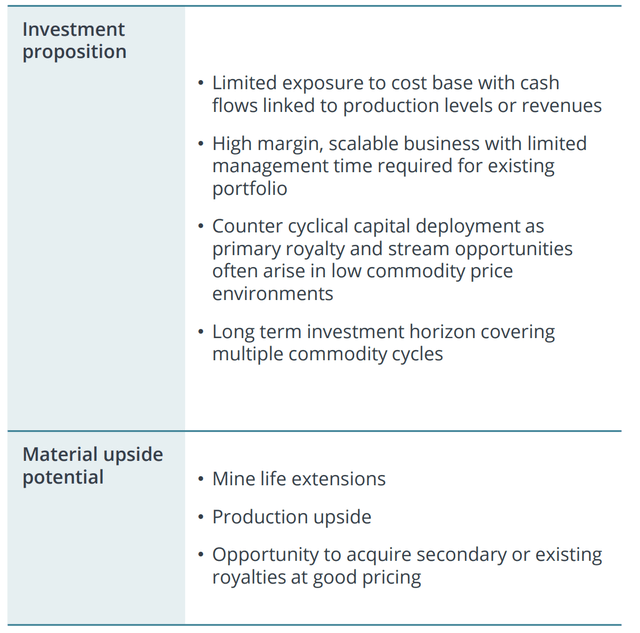

A P/E ratio of 9 could be a horny valuation for a daily base metals mining firm. Nonetheless, Ecora is a base steel royalty firm, which has a number of benefits in comparison with a daily mining firm (see chart under). The restricted publicity that royalty firms must the price of manufacturing makes them ideally suited inflation performs, as their revenues improve with the worth of inflation, however they’re largely shielded from elevated mining prices. That is notably true for revenue-based royalties akin to internet smelter royalties ((NSRs)), gross royalties and gross overriding royalties, which account for almost all of Ecora Useful resource’s revenues.

Supply: Ecora Assets February 2023 Investor Presentation

Wanting on the present valuations of different royalty firms utilizing knowledge from In search of Alpha and royalty firm investor displays, a Value/Gross sales ratio of 4.5 and a P/E ratio of 9 is affordable (observe that each one firms under have a Value/Gross sales ratio in extra of 10):

- Franco Nevada (FNV) trades at a at a Value/Gross sales ratio of 19 and a P/E ratio of round 32, with its gold equal ounces anticipated to extend by 9% between 2021 and 2026.

- Wheaton Valuable Metals (WPM) trades at a Value/Gross sales ratio of 17 and a P/E ratio of round 23, with its gold equal ounces anticipated to extend by 7% between 2021 and 2026.

- Royal Gold (RGLD) trades at a Value/Gross sales ratio of 13 and a P/E ratio of round 33, and trades at an identical worth to internet asset worth as Wheaton Valuable Metals.

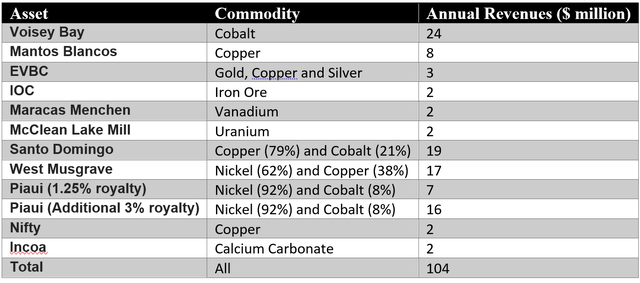

Nonetheless, this thesis of low cost valuation relaxation on its Ecora’s non-coal income forecasts. Subsequently, I generated my very own forecast of medium-term revenues, as a sanity examine, for every royalty anticipated to generate over $1 million in annual revenues (see desk under). To generate these estimates, I used manufacturing estimates obtained from the Ecora web site and commodity costs near their historic averages, and for simplicity handled all revenue-based royalties as being gross income royalties. The revenues generated by the extra vital royalties had been calculated as follows (which given excessive volatility in costs must be roughly appropriate):

- Voisey’s Bay: $24 million (2,600 tons of cobalt * $40,000 per ton of cobalt * 23% share).

- Mantos Blancos: $8 million (52,000 tons of copper * $10,000 per ton of copper *1.5% share).

- Santo Domingo: $19 million ((77,000 tons of copper * $10,000 per ton of copper + 5,000 tons of cobalt * $40,000 per ton of cobalt) * 2% share).

- West Musgrave: $17 million ((33,000 tons of copper * $10,000 per ton of copper + 27,000 tons of nickel * $20,000 per ton of nickel) * 2% share).

- Piaui (1.25% royalty): $7 million ((24,000 tons of nickel * $20,000 per ton of nickel + 1,000 tons of cobalt * $40,000 per ton of cobalt)*1.25% share)

- Piaui (Further 3% royalty). $16 million ((24,000 tons of nickel * $20,000 per ton of nickel + 1,000 tons of cobalt * $40,000 per ton of cobalt)*3% share). Notice that with a view to receive the additional 3% royalty on Piaui, Ecora must pay $70 million in money.

The annual non-coal revenues that I estimated of $104 million carefully match Ecora’s estimate of round $100 million. Based mostly on the annual income values within the desk under, I estimate that copper, cobalt and nickel are anticipated to account for round 35%, 29% and 26% of non-coal revenues respectively, with the remaining commodities accounting for round 11% of revenues. It is a extremely diversified publicity to base metals, notably to cobalt and nickel, which is exclusive amongst royalty firms. Evaluating with the opposite industrial steel centered royalty firms when it comes to base steel revenues, utilizing info from their investor displays, it’s clear that Ecora’s commodity publicity is considerably totally different:

- Labrador Iron Ore Royalty Company (OTCPK:LIFZF) has no base steel revenues, as all its revenues come from iron ore.

- Altius Mineral (OTCPK:ATUSF) generates round 36% of its revenues from copper and round 8% of its revenues from nickel, zinc and cobalt. The remaining revenues come from potash, iron ore and energy era.

- Nova Royalty (OTCQB:NOVRF) is primarily uncovered to copper royalties, with round a ten% publicity to nickel.

Supply: Creator’s calculation primarily based on knowledge obtained from the Ecora web site and assuming commodity costs primarily based on historic averages

Funding Dangers

Probably the most vital funding danger I foresee is that the principle growth tasks don’t attain full manufacturing, resulting in a shortfall in revenues to Ecora. It is a danger inherent to all growth tasks. Nonetheless, I believe that Ecora’s three predominant growth tasks are all more likely to be developed for the next causes:

- The West Musgrave mine is at the moment underneath building, making it nearly sure that it’s going to produce nickel and copper for many years to come back, explicit because it is likely one of the predominant the explanation why BHP is shopping for OZ Minerals.

- Piaui is already producing small portions of nickel and cobalt and is on observe to ramp as much as full manufacturing.

- No mine building choice has been made on Santo Domingo but, nevertheless, the mine is absolutely permitted, and can or not it’s Capstone Copper’s main growth venture put up 2023.

One other potential danger to Ecora is its vital publicity to cobalt, which may potential get replaced by different metals in electrical automobile batteries. Nonetheless, even when this had been to happen, I’m not satisfied that this is able to considerably affect cobalt costs. At the moment, cobalt is buying and selling at across the identical worth that it was buying and selling at in 2010, which was lengthy earlier than electrical automobiles grew to become widespread. Moreover, all of Ecora’s cobalt is sourced outdoors of the DRC, which can end in it will definitely buying and selling at a premium.

A 3rd funding danger is the present excessive rate of interest surroundings, which will increase the curiosity Ecora would pay on debt. If increased debt funds had been probably mixed with vital delays in a few of its growth tasks, it may end in them not having the ability to make further royalty purchases within the close to future, or extra problematically, not be capable to preserve the present dividend. Nonetheless, my funding thesis isn’t predicated on a excessive dividend or additional acquisitions. Moreover, excessive rates of interest depress all asset values, that means that Ecora may probably buy royalty portfolios at a extra engaging worth.

A remaining funding danger is that the financial system goes right into a recession. This might possible set off a fall in Ecora’s inventory worth and a fall in commodity costs, which would scale back Ecora’s revenues. Nonetheless, I might view this as a shopping for alternative, as Ecora’s inventory worth would possible improve once more because the financial system improves. Moreover, a recession may show to be a long-term blessing for Ecora, as it will allow it to buy royalty portfolios at discount costs, and if the recession is accompanied by decrease rates of interest, Ecora would pay decrease curiosity expenditures on loans used for acquisitions.

Ultimate Ideas

Ecora’s share worth has been remarkably secure over the past 5 years (see chart under). My thesis for that is that the market has but to understand the transformation of Ecora’s portfolio from coal to base metals property, and consequentially assign it the next valuation a number of. I think this can change as soon as Piaui absolutely ramps up and West Musgrave goes into manufacturing. I’m bullish ECRAF.

Supply: In search of Alpha

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

{kind=link}