Revealed on February twenty second, 2024 by Bob Ciura

The Dividend Kings encompass firms which have raised their dividends for at the very least 50 years in a row. Due to their unparalleled streak of annual dividend will increase, it is not uncommon to view the Dividend Kings as among the many greatest dividend development shares within the inventory market.

You’ll be able to see the complete checklist of all 56 Dividend Kings right here.

We additionally created a full checklist of all Dividend Kings, together with related monetary statistics like dividend yields and price-to-earnings ratios. You’ll be able to obtain the complete checklist of Dividend Kings by clicking on the hyperlink under:

Phone & Information Programs (TDS) just lately elevated its dividend for the fiftieth consecutive yr. Consequently, the corporate now joins the unique checklist of Dividend Kings.

This text will analyze the corporate’s enterprise overview, future development prospects, aggressive benefits, and extra.

Enterprise Overview

Phone & Information Programs is a telecommunications firm that gives clients with mobile and landline companies, wi-fi merchandise, cable, broadband, and voice companies throughout the US. The corporate’s Mobile Division accounts for greater than 75% of whole working income. TDS began in 1969 as a set of 10 rural phone firms. In the present day the corporate has a market cap of $1.7 billion and greater than $5.4 billion in annual revenues.

TDS posted fourth-quarter earnings on February sixteenth. Quarterly income of $1.32 billion beat estimates by $40 million, whereas adjusted earnings-per-share got here to a lack of $0.11 per share. Income declined 3.2% from the 2022 fourth quarter. The online lack of $0.38 per share for the fourth quarter was due primarily to a $547 million non-cash impairment cost at TDS Telecom.

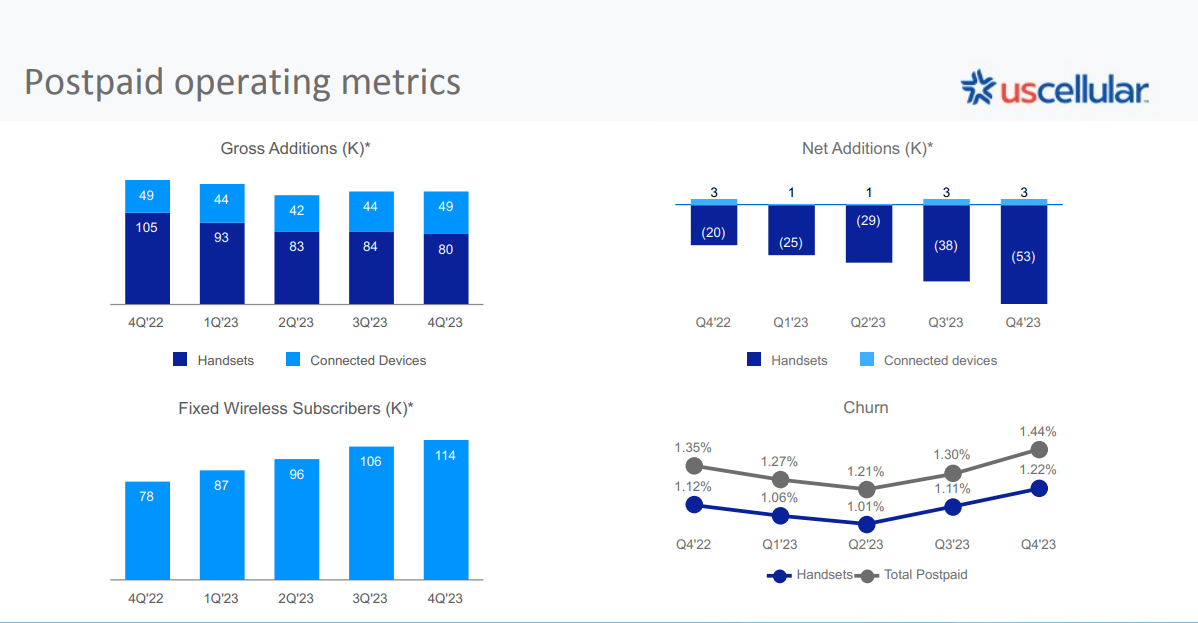

At US Mobile, postpaid common income per person grew 2% for the complete yr 2023. Fastened wi-fi clients grew 46% to 114,000 whereas tower rental revenues grew 8% to $100 million.

Together with quarterly outcomes, the corporate raised its dividend by 2.7% to $0.19 per share.

Progress Prospects

TDS operates a really low-growth enterprise, as it’s a very small participant in a extremely aggressive trade that’s dominated by Verizon and AT&T. That has led to repeated years of detrimental earnings development. TDS has an 82% stake in U.S. Mobile and primarily depends on this stake to realize development.

In recent times, U.S. Mobile centered on connecting clients in under-served areas with their high-quality community, in addition to market share enlargement, growing enterprise with authorities clients in 5G and IoT, and bettering community modernization and 5G applications.

TDS Telecom grew broadband income with a rise in buyer connections and expanded the attain of their fiber and 1Gig companies. TDS has made investments in the direction of rising its shopper base, increasing into new territories, in addition to bettering their community applied sciences, in an effort to spice up the corporate’s competitiveness.

Nevertheless, rising working bills and impairments are taking a few of that benefit away over time, as we noticed with 2023 outcomes. Along with that, the corporate is making an attempt to construct out its choices in broadband service by way of its fiber infrastructure, which helps ship quicker and extra dependable web to residences in its service space.

Working income has been roughly flat for a while, and we anticipate it’s going to stay as such for the foreseeable future. Whereas TDS is making an attempt to take a position for development, we imagine the corporate is going through an uphill battle in the case of rising earnings within the years to return. We estimate 2% annual EPS development for the corporate over the following 5 years.

Aggressive Benefits & Recession Efficiency

TDS’ aggressive benefit, if it has one, is that it has a captive viewers of kinds in its service areas. Broadband operators are likely to have service areas analogous to energy utilities in that selection for shoppers is normally restricted. That may assist defend TDS’ internet-based income over time, however we see much less of a worth proposition for shoppers on wi-fi income.

Shoppers have far more selection in the case of wi-fi income, and whereas TDS hasn’t confronted a person exodus, development is low and we attribute that to the extreme competitors within the wi-fi service area. The actual fact is that Verizon and AT&T have scale benefits that TDS doesn’t, and we predict that its aggressive place is probably in danger consequently.

To its credit score, TDS has weathered a number of recessions up to now, elevating its dividend by way of all of them. Even when we get a recession in 2024, we don’t assume that alone would put the dividend in danger, as the corporate’s income and earnings are usually not essentially beholden to financial situations. Somewhat, TDS is extra vulnerable to company-specific danger elements, as mentioned above.

Valuation & Anticipated Returns

To worth TDS, we can’t use EPS as the corporate reported a internet loss for 2023. Subsequently, we’ll use guide worth per share as a proxy for EPS, and price-to-book ratio as a substitute of P/E. Utilizing the present share value of ~$14 and guide worth per share of $47.90, the inventory trades with a price-to-book ratio of 0.30.

The ten-year common P/B ratio is 0.64, however we peg truthful worth at a P/B ratio of 0.45 by 2029. Nonetheless, an enlargement of the valuation a number of might enhance annual returns by 8.4% per yr over the following 5 years.

Individually, estimated enterprise development of two% will enhance shareholder returns. Lastly, the inventory has a 5.3% present dividend yield.

Placing all of it collectively, TDS is predicted to return over 15% yearly over the following 5 years, making the inventory a purchase.

TDS has raised its dividend for 50 consecutive years. It has grown its dividend by ~3% per yr on common over the previous 5 years. In the present day, its 5.3% dividend yield is considerably increased than the yield of the S&P. Nevertheless, the dividend just isn’t backed by optimistic EPS, making it a comparatively dangerous dividend payout.

As TDS and U.S. Mobile function in a extremely aggressive enterprise, the company lacks a significant aggressive benefit. As U.S. Mobile generates the overwhelming majority of the revenues and earnings of TDS and is presently its most vital development driver, any headwind that will present up in the way in which of U.S. Mobile will have an effect on TDS.

In different phrases, there isn’t a assure that TDS will be capable of proceed its dividend improve streak indefinitely, given its detrimental EPS and cloudy development outlook.

Remaining Ideas

TDS depends on the efficiency of U.S. Mobile, and it’s now present process a strategic assessment to find out its greatest plan of action to unlock shareholder worth, which might consequence within the sale of the corporate or its belongings. TDS inventory might nonetheless provide robust annual return potential over the following 5 years.

We presently charge TDS inventory a purchase resulting from its excessive projected returns, though we acknowledge the excessive degree of danger to the dividend and the volatility of the corporate’s outcomes.

Different Certain Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}