Updated on October 4th, 2022 by Quinn Mohammed

The Dividend Kings are widely known as a group of dividend growth stocks to buy and hold for the long-term.

These companies have generated strong profits year after year, even during recessions, and have proved their ability to grow earnings steadily over many years.

The Dividend Kings are a group of companies with 50+ consecutive years of dividend increases.

You can see all 45 Dividend Kings here.

You can also download an Excel spreadsheet with the full list of Dividend Kings (plus metrics that matter, such as price-to-earnings ratios and dividend yields) by clicking the link below:

Up next in our annual Dividend Kings In Focus series is consumer products behemoth Procter & Gamble (PG), which has paid dividends for 131 years. The company has also increased its dividend for 66 consecutive years.

Procter & Gamble is one of the most well-known dividend stocks, largely due to its extremely long dividend history and widely recognizable brands.

Years ago, P&G completed a major overhaul of its product portfolio, including a significant divestment of brands no longer deemed necessary.

This article will discuss P&G’s portfolio transformation, future growth prospects, and stock valuation.

Business Overview

Procter & Gamble is a consumer products giant that sells its products in more than 180 countries and generates roughly $80 billion annual sales.

Its core brands include Gillette, Tide, Charmin, Crest, Pampers, Febreze, Head & Shoulders, Bounty, Oral-B, and many more.

During P&G’s massive portfolio restructuring over the past few years, the company sold off dozens of its consumer brands.

Asset sales in recent years include battery brand Duracell to Berkshire Hathaway (BRK-A) (BRK-B) for $4.7 billion and a collection of 43 beauty brands to Coty (COTY) for $12.5 billion.

Today, P&G has slimmed down to just 65 brands, from 170 previously. And those brands are acquiring global market share at a healthy rate over the past few years.

Source: Investor Presentation

The company operates in five reporting segments based on the following product categories:

- Fabric & Home Care

- Baby, Feminine, & Family Care

- Beauty

- Health Care

- Grooming

Growth Prospects

Following P&G’s restructuring, the company is now a more agile and flexible organization with improved growth prospects. While P&G divested low-margin businesses with limited growth potential, it held on to its core consumer brands such as Tide, Charmin, Pampers, Gillette, and Crest.

In addition, P&G received billions of dollars from its numerous asset sales, and a portion of that went to stock buybacks. These buybacks have also boosted P&G’s earnings-per-share over time.

Margin expansion is a major component of P&G’s earnings growth strategy. P&G’s cost-cutting efforts have elevated its operating margins and after-tax profit margins. However, high-cost inflations are negatively affecting gross margins in recent results.

As part of the restructuring, P&G launched a massive cost-cutting effort. It cut costs by $10 billion over the course of its restructuring through headcount reduction and lower SG&A expenses.

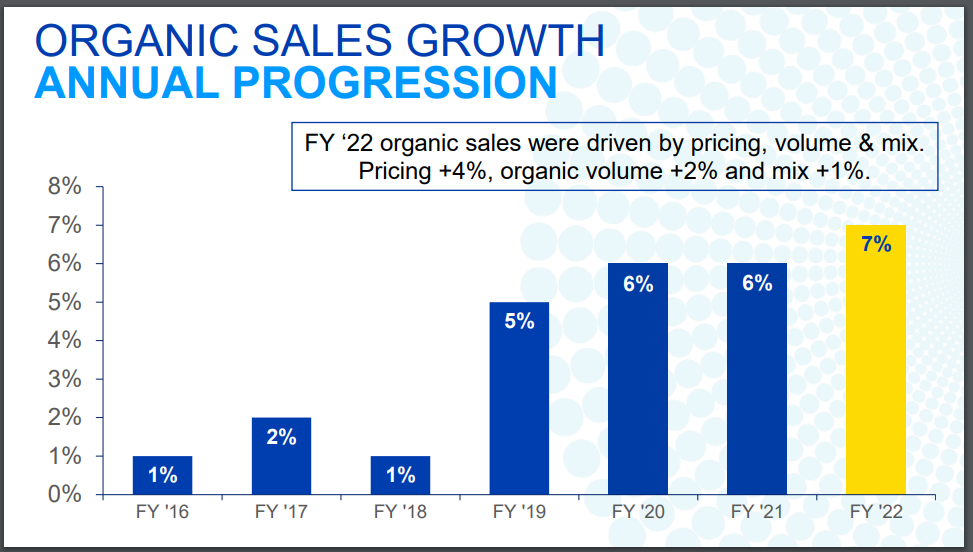

At the same time, the focus on premier brands with pricing power has resulted in consistent sales growth:

Source: Investor Presentation

In the 2022 fiscal year, the company generated $80.2 billion in sales, a 5% increase compared to FY 2021, as organic sales increased 7%.

This result featured sales increases of 2%, 2%, 9%, 6%, and 5% in the company’s Beauty, Grooming, Health Care, Fabric & Home Care, and Baby, Feminine & Family Care segments, respectively.

Adjusted earnings-per-share equaled $5.81, a 3% increase compared to $5.66 in 2021.

Procter & Gamble also provided fiscal 2023 guidance, anticipating up to 4% adjusted earnings-per-share growth for roughly $5.93 per share at the midpoint.

We are forecasting 4% annual earnings-per-share growth over the next five years.

Competitive Advantages & Recession Performance

P&G has several competitive advantages. The first is its strong brand portfolio. P&G has several brands that generate annual sales $1 billion or more.

These and other core brands hold leadership positions in their respective categories as well. These products are associated with high quality, and consumers will pay a premium for them.

The company invests heavily in advertising to retain its competitive position, which it can do thanks to its financial strength. It also invests heavily in research and development. This investment is a competitive advantage for P&G; R&D fuels product innovation, while advertising helps market new products and gain share.

P&G’s competitive advantages allow the company to remain profitable, even during periods of recession. Earnings held up very well during the Great Recession:

- 2007 earnings-per-share of $3.04

- 2008 earnings-per-share of $3.64 (19.7% increase)

- 2009 earnings-per-share of $3.58 (-1.6% decline)

- 2010 earnings-per-share of $3.53 (-1.4% decline)

As you can see, P&G had a very strong year in 2008, with nearly 20% earnings growth. Earnings dipped only mildly in the following two years.

This was a very strong performance in one of the worst economic downturns in the past several decades.

P&G also performed relatively well in 2020, as consumers still needed personal care and household products during the coronavirus pandemic.

P&G has a recession-resistant business model. Everyone needs paper towels, toothpaste, razors, and other P&G products, regardless of the economic climate.

Valuation & Expected Returns

Based on our expectation for earnings-per-share of $6.00 for fiscal 2023, P&G is presently trading at a price-to-earnings ratio of 21.4.

Our fair value estimate for P&G is a P/E of 20. As such, shares appear to be overvalued.

If P&G’s valuation were to revert back to 20.0 times earnings, future shareholder returns could face a -1.4% annual reduction over the next 5 years.

Earnings growth and dividends will help offset the impact of a contracting price-to-earnings multiple. For example, we expect P&G to generate 4.0% annual earnings growth each year, and the stock has a current dividend yield of 2.8%.

However, adding it all up leaves a total return potential of just 5.4% each year.

That said, P&G continues to have appeal as a dividend growth stock.

The current dividend payout is well-covered by earnings, with room to grow. Based on expected fiscal 2022 earnings, P&G has a payout ratio of just above 60%. This leaves enough cushion for future dividend increases each year.

Investors should expect P&G to continue increasing its dividend each year for many years to come. It has the brand strength, competitive advantages, and profitability to maintain its steady annual dividend increases over the long term.

Final Thoughts

P&G has many strong qualities that make it a time-tested dividend growth company. Thanks to a significant reshuffling of its brand portfolio years ago, P&G positioned itself to capitalize on global growth opportunities.

P&G has a long history of rewarding shareholders with dividends. For its long history of annual dividend hikes, P&G earns a place on our list of “blue chip” stocks.

You can see the full list of blue chip stocks here.

However, the current valuation leaves something to be desired from a value perspective.

While we remain enthused about the ongoing growth of the business, we do not find shares to be attractive enough to buy at this time.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].