Up to date on September twenty ninth, 2023 by Bob Ciura

We consider long-term traders ought to give attention to the highest-quality dividend progress shares. These are firms with lengthy histories of elevating their dividends, and sturdy aggressive benefits to gas continued dividend progress.

Due to this fact, we are likely to steer traders towards the Dividend Kings, a gaggle of simply 50 shares with a minimum of 50 years of dividend will increase.

You can even obtain an Excel spreadsheet with the total checklist of all 50 Dividend Kings (plus necessary metrics similar to price-to-earnings ratios and dividend yields) by clicking on the hyperlink beneath:

We overview every of the Dividend Kings yearly. The subsequent inventory to be reviewed on this 12 months’s version is AbbVie (ABBV).

There are questions concerning AbbVie’s future progress, as a result of its flagship drug Humira dealing with patent expiration. Nevertheless, the corporate has a plan to proceed rising within the years forward.

Enterprise Overview

AbbVie is a worldwide pharmaceutical large. It started buying and selling as an unbiased firm in 2013, after it was spun off from Abbott Laboratories (ABT). AbbVie generated robust progress for the reason that spin-off. Based on AbbVie, it grew income and adjusted EPS progress by 14.7% and 19% respectively, annually from 2013-2021.

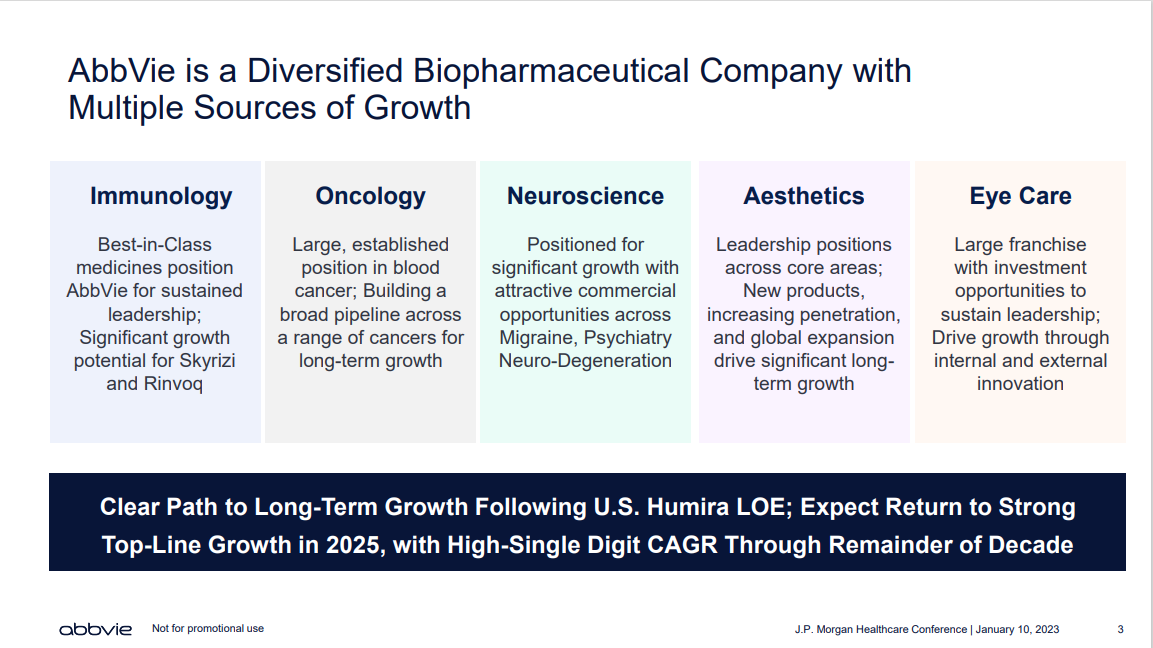

At present, AbbVie focuses on one primary enterprise phase—prescribed drugs. It focuses on just a few key remedy areas, together with immunology, hematologic oncology, neuroscience, and extra.

Supply: Investor Presentation

For the reason that spin-off from Abbott, AbbVie has produced wonderful progress, due largely to Humira, a multi-purpose drug. The problem for AbbVie is that Humira is now dealing with biosimilar competitors after it has misplaced patent exclusivity.

Even so, AbbVie stays a large within the healthcare sector, with a big and diversified product portfolio.

Within the 2023 second quarter, revenues of $13.9 billion declined 5% from the identical quarter final 12 months. Revenues had been positively impacted by progress from a few of its newer medicine, together with Skyrizi and Rinvoq. Nonetheless, declining income for Humira took its toll final quarter.

Earnings-per-share of $2.91 declined 14% from the identical quarter final 12 months, however EPS did beat analyst estimates by $0.10.

Progress Prospects

The main threat for international pharmaceutical producers is patent loss. When a specific drug loses patent, the market is often flooded with competitors, particularly for the world’s top-selling merchandise.

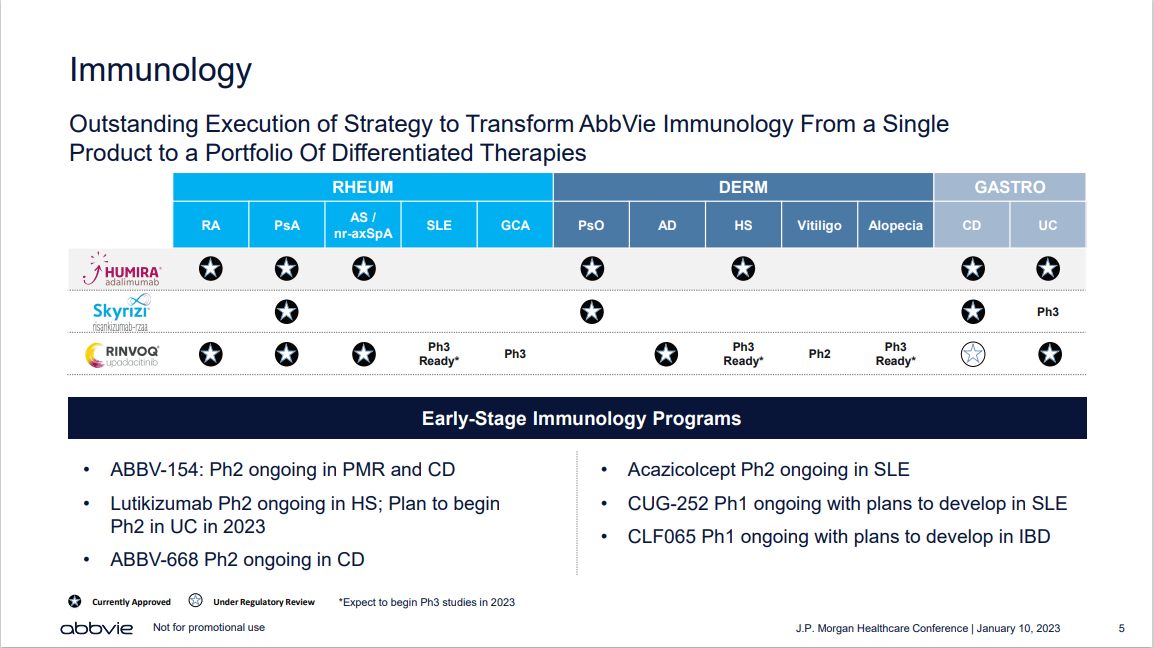

For AbbVie, its largest threat is the competitors about to hit its flagship drug Humira, a multi-purpose drug that’s used to deal with a wide range of situations. A few of these embody rheumatoid arthritis, plaque psoriasis, Crohn’s illness, ulcerative colitis, and extra.

Humira at one level generated over half of AbbVie’s annual gross sales. Lack of patent exclusivity is a big overhang–AbbVie expects its complete gross sales will decline in 2023 in consequence. On the identical time, AbbVie additionally expects to return to gross sales progress in 2025, with excessive single-digit annual progress by means of the tip of the last decade.

Luckily, the corporate ready for the lack of patent exclusivity on Humira by investing closely in new merchandise, in addition to acquisitions to spice up its progress. For instance, Rinvoq and Skyrizi are two key merchandise that signify long-term progress catalysts.

Supply: Investor Presentation

AbbVie additionally accomplished the $63 billion acquisition of Allergan. Allergan’s flagship product is Botox, which diversifies AbbVie’s portfolio with publicity to international aesthetics.

The corporate sees its aesthetics income rising at a excessive charge over the following a number of years, exceeding $9 billion in 2029.

Supply: Investor Presentation

In all, we anticipate 3% EPS progress for AbbVie over the following 5 years, reflecting the steep patent cliff dealing with Humira. We consider the expansion outlook will enhance when the Humira overhang is gone, however there may be uncertainty surrounding AbbVie’s capacity to beat that with new merchandise.

Aggressive Benefits & Recession Efficiency

Crucial aggressive benefit for AbbVie, and any pharmaceutical firm, is its patent portfolio. Pharmaceutical giants have to spend closely to develop new medicine and therapies, when one in every of their blockbusters loses patent safety.

AbbVie has over 80 scientific applications. It has a number of progress alternatives to interchange Humira, significantly within the therapeutic areas of immunology, hematology, and neuroscience. The results of its important funding in R&D is a well-stocked pipeline.

AbbVie was not a standalone firm over the past monetary disaster, so there is no such thing as a recession monitor document. Nevertheless, the very fact stays that since sick individuals require remedy whether or not the economic system is robust or not, it’s extremely probably that AbbVie would proceed to carry out nicely throughout a recession.

AbbVie’s earnings are prone to decline considerably in a recession, however the dividend ought to stay safe. AbbVie has a projected dividend payout ratio of ~54% for 2023.

Valuation & Anticipated Returns

AbbVie is anticipated to generate adjusted EPS of $11.00 for 2023, on the midpoint of steerage. At this EPS degree, the inventory is at present buying and selling for a price-to-earnings ratio of 13.7.

Our honest worth estimate for AbbVie is a price-to-earnings ratio of 11, which means the inventory is barely over-valued in the present day. A declining P/E a number of may scale back shareholder returns by roughly 4.3% per 12 months over the following 5 years.

As well as, we anticipate annual earnings progress of three% by means of 2028.

Lastly, the inventory has a present dividend yield of three.9%. Given these inputs, we anticipate annual returns of two.6% per 12 months over the following 5 years, making AbbVie inventory a maintain.

Last Ideas

AbbVie is a really high-quality enterprise, with a robust pharmaceutical pipeline and progress potential. It’s also a shareholder-friendly firm that returns extra money circulate to traders by means of inventory buybacks and dividends.

AbbVie faces a big problem in changing misplaced Humira gross sales because it faces competitors within the U.S. and Europe. For this reason we’ve got pretty low assumptions for the corporate’s future EPS progress and honest worth P/E a number of.

Nonetheless, the corporate has constructed a big portfolio of latest merchandise that ought to hold its progress intact. And, AbbVie will be capable of generate extra progress from the acquisition of Allergan.

Nevertheless, the low anticipated returns make the inventory a maintain.

Moreover, the next Positive Dividend databases include essentially the most dependable dividend growers in our funding universe:

- The Dividend Champions: Dividend shares with 25+ years of dividend will increase, together with these that won’t qualify as Dividend Aristocrats.

- The Dividend Kings: thought-about to be the last word dividend progress shares, the Dividend Kings checklist is comprised of shares with 50+ years of consecutive dividend will increase

For those who’re on the lookout for shares with distinctive dividend traits, contemplate the next Positive Dividend databases:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

{kind=link}